When it comes to investments, we all want solid returns – and that brings many investors to dividend stocks, and REITs in particular. These companies put capital to work in the real estate sector, either owning, managing, and leasing real properties; funding and investing in mortgages and mortgage-backed securities; or following a combination of these tracks – and they are known for paying out high percentages of their profits back to shareholders in the form of dividends.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Among the REITs, the hospitality sector – hotels, resorts, and other leisure properties – is known for its high volatility consequent to its exposure to leisure industry cycles. Hospitality REITs bring a unique twist to the REIT model – instead of directly working with the ownership or management of their properties, they derive their income from the short-term room rental rates.

For investors, this brings up two vital points – first, that hospitality REIT investors are somewhat insulated from the real estate aspects of the leisure properties, and second, that room count is a vital statistic in judging a hotel or hospitality REIT stock.

It all makes an interesting background to some recent stock picks from Jefferies analyst David Katz, who believes that it’s time to load up on two 2 hospitality REIT stocks in particular. A look into the details on them with help from the TipRanks database should offer some insight.

Park Hotels & Resorts (PK)

First up is Park Hotels & Resorts, a leisure REIT with a strong portfolio of major hotels and convention centers, mainly located in important urban cores and other vacation destinations around the US. Park Hotels can boast that its portfolio includes 12 resort locations, 13 prime city centers, 5 convention centers, and 13 strategic airport and ‘other’ locations. These properties have a total of 26,000+ premium rooms, conveniently located and well-maintained; some 86% of these rooms are classed in the luxury and upscale hotel segments.

All of that makes a solid foundation for a leisure REIT, and Park Hotel & Resorts complements the scale of its portfolio with the quality of the names. This REIT owns properties under such top-end hotel brands as Hilton, Hyatt, and Marriot.

This company’s stock has strongly outperformed the broader markets in the past year, as the company has benefited from some important tailwinds. PK shares are up 41% in the last 12 months, compared to a gain of 25% on the S&P 500, and the company’s year-to-date gain, of 13%, has easily outpaced the S&P’s 6.5% ytd increase. Tailwinds that have supported the shares include solid performance in the New York market – and strong results from the company’s Honolulu properties, which have gained due to lack of competition from resorts on the island of Maui.

Turning to the results, we find that Park Hotel reported total revenue of $657 million for the fourth quarter of 2023, a figure that was down a modest 1.2% from the prior year quarter, but beat the Street’s forecast of $652 million. Additionally, the bottom-line figure, the FFO – funds from operations, a key metric in the REIT industry – came to 52 cents per share, a penny better than the forecast.

Not only did the FFO beat expectations, it also fully covered the company’s dividend payment. Park’s most recent dividend was declared on February 27 for 25 cents per share. This dividend represents an increase of 67% in the recurring quarterly payment, and the annualized rate of $1 gives a forward yield of almost 5.8%.

For Katz, covering the stock from Jefferies, the key points here are Park’s sound exposure to the quality Hilton name, the company’s ability to maintain and renovate its properties, and the fundamentally sound industry. He writes, “The solid performance in the fourth quarter coupled with Mgt. commentary on its positive outlook suggests meaningful growth trajectory. PK’s unique position in HI which is still recovering post-COVID and the value-enhancing renovation projects support upside and the prospective divestiture of on-core assets and capital recycling, all suggest further upside. Finally, we believe valuations are supported by the stable fundamental environment.”

Laying out the case to move forward, Katz adds, “We view the prospects of a long-term group and business travel recovery to be balanced by a relative dispersion of asset values and market exposures within the portfolio vs. the group. The divestiture of non-core assets, capital returns, and debt pay-downs should drive incremental value upside as the magnitude expands. We also note that the fundamental context for Lodging and REITs in particular is increasingly positive, which supports our view on PK and specific peers.”

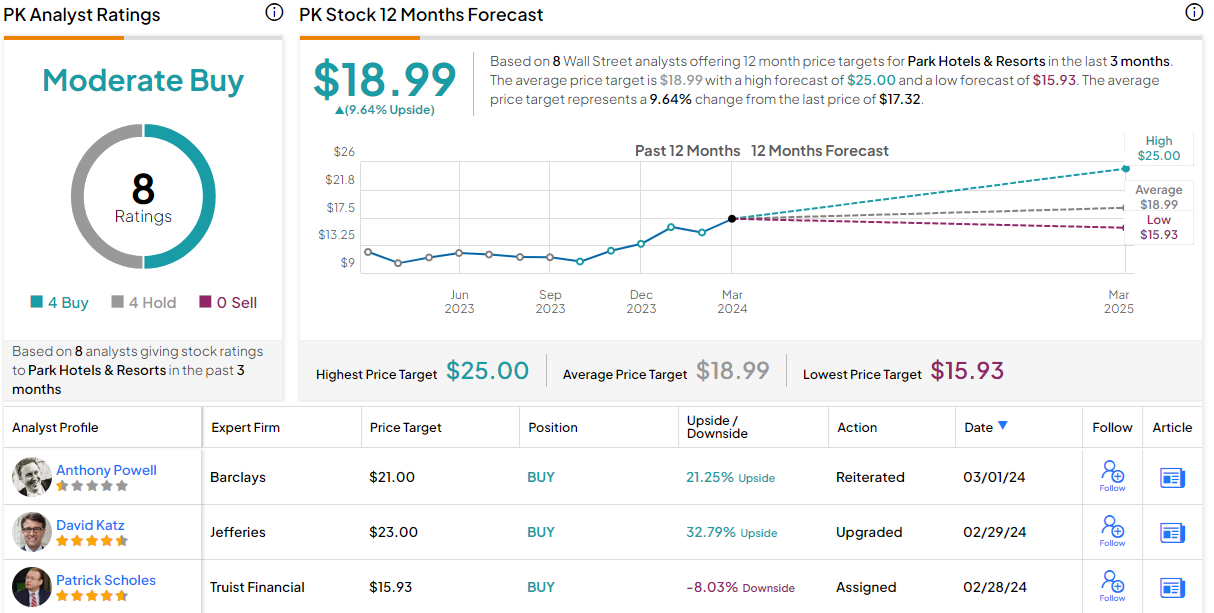

What this means, for the analyst, is a Buy rating with a price target of $23 to show potential for a 33% upside in the coming months. (To watch Katz’s track record, click here)

Overall, Park has earned a Moderate Buy consensus rating from the Wall Street analysts, based on 4 Buy and Hold recommendations, each, set in recent months. The shares are trading for $17.32 and their $18.99 average target price suggests a one-year upside potential of 9.5%. (See PK stock forecast)

Xenia Hotels & Resorts (XHR)

Next on our list is Orlando-based Xenia Hotels & Resorts, another REIT in the luxury and upscale hotel niche. This leisure REIT is a self-advised, self-administered entity, operating in the US, with properties in 25 of the nation’s top lodging markets and key leisure destination areas. Xenia’s holding portfolio contains 32 hotels in 14 states, and claims a total of 9,514 rooms. Like Park above, Xenia benefits from the well-known names on its hotel properties; these include Davidson, Fairmont, Hilton, and Loews.

During the fourth quarter of last year, Xenia spent a total of $51.4 million on portfolio improvements and property renovations. This represented almost half of the 2023 total spend on these activities, which came to $120.9 million. The renovation activity included completion of projects on 5 hotels, and substantial progress toward completion on a sixth, the Waldorf Astoria Atlanta Buckhead. In addition, last year the company began a $110 million project to renovate the Hyatt Regency Scottsdale Resort & Spa at Gainey Ranch. This property has 491 rooms and is in the process of being upgraded to a Grand Hyatt.

In 4Q23, the company was in-line on revenue – reporting $253.38 million at the top line, down 3.7% year-over-year – but beat the forecast on the bottom line. The adjusted FFO came to 41 cents per share, above consensus at $0.37 and fully covered the 12-cent common share dividend. This dividend was declared on February 27 for an April 15 payout, and marked a 20% increase from the previous quarter. The 48-cent annualized dividend gives a forward yield of 3.13%.

When we turn to Katz’s comments, we find that the analyst’s upbeat stance is based in large part on the renovations. He writes, “We believe recent renovations bear outsized EBITDAre upside upon stabilization, which is not fully reflected in consensus or valuation which begins in 2024-2025. The recently renovated hotels should add an incremental $24M of Adj. EBITDAre and another $25M from Hyatt Scottsdale, ultimately leading to an estimated notional stabilized pro-forma Adj. EBITDAre of ~$343M over the next few years. This warrants valuation multiple increases to at least 11X AFFO from 10X, which compares to historical peak levels of 16X.”

In addition, Katz goes on to explain why this stock is likely to continue generating returns for shareholders, saying of it, “XHR maintains a strong balance sheet that has peaked at 4.7X as of end 2023 to 4.1X at least by 2025, mostly driven by better operating results. Given the healthy outlook, Mgt. set a long-term target to return to a prepandemic payout ratio in the mid-60% range of FFO as its portfolio ultimately stabilizes, vs. current ~40%, which implies the dividend could approximately double over time, according to Mgt.”

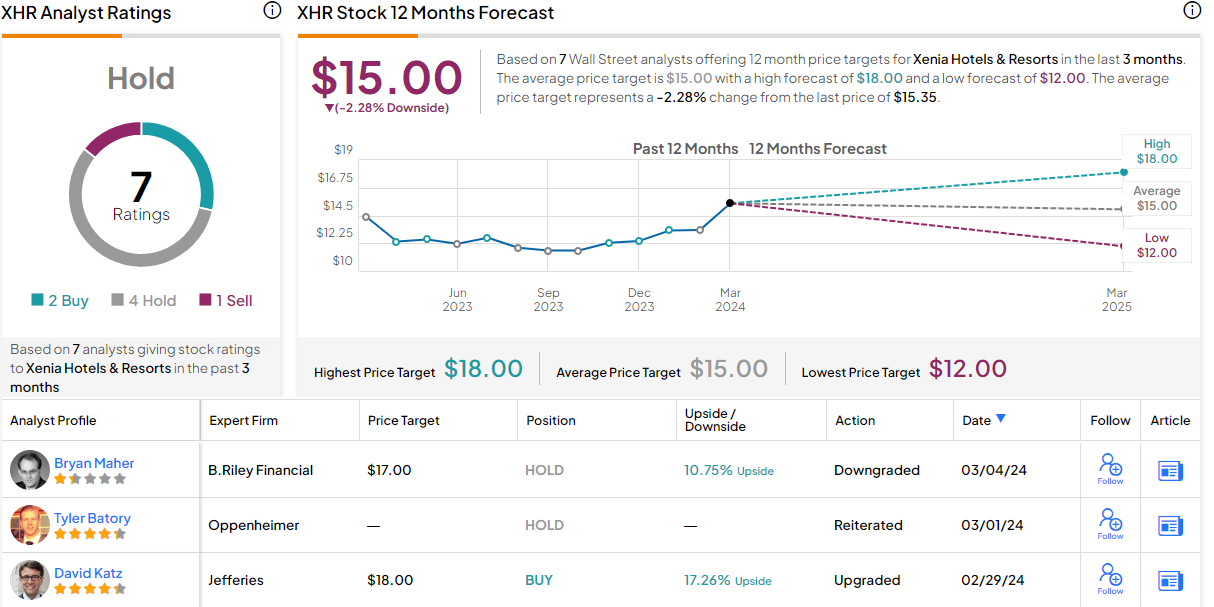

These comments support Katz’s Buy rating on the stock, while his $18 price target implies a 12-month gain of 17%.

Katz is more bullish than the Street’s consensus here. The stock has 7 recent reviews, and the 2-4-1 split – Buy-Hold-Sell – gives the shares a Hold consensus rating. The average target price of $15 suggests the shares will remain rangebound for the time being. (See Xenia stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.