A full quarter of 2024 is behind us now, and it’s clear that we’re in the midst of another bullish run, similar to last year. The gains are substantial; markets reached a trough in October 2023, and the S&P 500 is up ~24.5% from that point while the NASDAQ has rebounded 29%. Year-to-date, the indexes are up 9% and 10%, respectively.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

And, while last year’s gains rested on the narrow base of mega-cap tech firms, the gains this year are built on a broader foundation, providing investors with more options for investment. The professional stock analysts are taking note, as well, and are not shy about tagging stocks as ‘Buys’ for the rest of this year.

With that as backdrop, we’ve dug up the details on two names the analysts at financial giant Wells Fargo have turned bullish on. They’ve recently upgraded their ratings on them – so, it’s ‘time to hit buy,’ in other words. Using the TipRanks database, we can see that these stocks already have ‘Buy’ ratings and double-digit upsides, while the Wells Fargo view sees gains of up to ~60%. Here are the details.

GoodRx Holdings (GDRX)

The first Wells Fargo pick on our list is GoodRx, a company that takes pharmacy services and joins it to both online tech and the growing telehealth industry to create a package deal designed to streamline the distribution of prescription medications. The company is based in Santa Monica, California, has been in business since 2011, and its operations are based on a key insight about healthcare consumers: that giving them access to better information will result in better consumer decisions – and better healthcare results.

Expanding upon that insight, GoodRx today gives its users the information they need – including price transparency and affordability solutions, based on convenient telehealth consultations. The result is an online pharmacy that is patient-oriented, designed to promote greater medication compliance and faster treatment regimens, all for a better patient outcome.

GoodRx’s chief service is access to prescription medications, with discount pricing. Patients can consult with physicians and pharmacists, can use electronic coupons, and can select from generic drug equivalents. The system is optimized to make sure that each patient gets the correct prescription, with the correct instructions, filled conveniently. The service is available directly through the company’s website, where users can also find informative articles from medical professionals, to add context to the prescription services.

By the numbers, GoodRx has built up a substantial business. The company provides more than 200 billion pricing points daily, and estimates that 80% of transactions are repeat business – a strong indication of satisfied customers. Overall, GoodRx estimates it has saved its customers approximately $60 billion over the years.

Turning to the results, we find that GoodRx showed a top-line of $196.6 million in 4Q23, a figure that beat the forecast by a modest $730,000 and was up nearly 7% year-over-year. On the bottom-line, EPS of ($0.06) missed the estimates by a penny.

Assessing the company’s prospects, Wells Fargo analyst Stan Berenshteyn thinks GoodRx is well set-up to outperform. He writes, “Analysis of strategic pivots over the last two years points to possible growth headwinds, but revenue visibility (and downside risk) appear to be materially improved. We think this sets up GoodRx to deliver on a beat & raise narrative in 2024 with upside to consensus expectations in 2025. We expect this dynamic to help GDRX close the valuation gap to its peers, in turn setting up the stock to see meaningful outperformance over the next 12 months.”

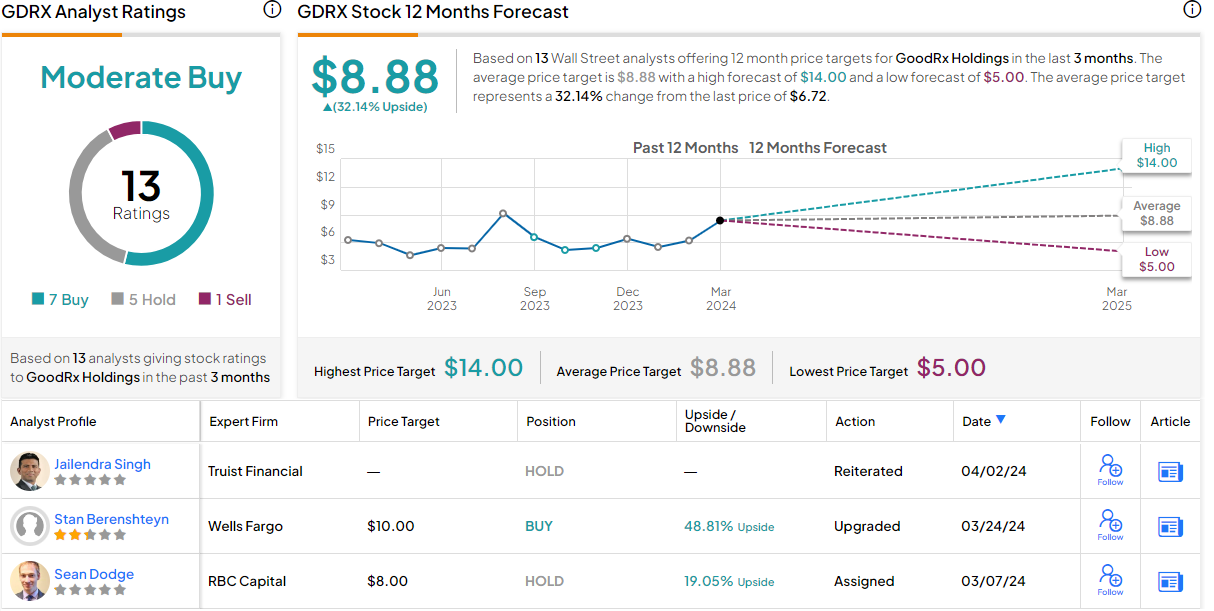

As such, the analyst recently upgraded his GDRX rating from Equal Weight (Neutral) to Overweight (Buy), while his $10 price target (up from $7.5) indicates a one-year upside of 49%. (To watch Berenshteyn’s track record, click here.)

This stock has 13 recent analyst reviews, breaking down to 7 Buys, 5 Holds, and 1 Sell, for a Moderate Buy consensus rating. The shares are trading for $6.72 and their $8.88 average target price suggests a 32% upside potential for the year ahead. (See GoodRx’s stock forecast.)

NeuroPace (NPCE)

Next up is NeuroPace, another California company in the medical field. NeuroPace focuses on the treatment of epilepsy. The company has developed the RNS system, a medical device designed to detect and prevent seizures without the use of medication. This is an important advance, as some types of epilepsy are known to be medication-resistant.

NeuroPace’s system acts directly in the brain, where it can monitor and record electrical activity, and apply nervous stimulation when seizures are indicated. Because the device also records EEG data, patients and physicians are able to fine-tune the stimulation and better monitor the pace and frequency of seizure activity. Patients using the device report a significant reduction in seizure activity, and 1 in 5 patients were reported as ‘seizure-free’ at their last medical check.

The company’s revenues have shown an almost consistent upward trend since the second half of 2022. In the last quarter reported, for 4Q23, revenue came to $18 million, up 41% from the $12.8 million reported in 4Q22. The firm’s EPS, reported as a loss of 23 cents per share, was 8 cents better than had been anticipated. For the full-year 2024, the company has guided for revenues between $73-$77 million, compared to 2023’s $65.4 million.

However, Wells Fargo’s Vik Chopra thinks the company might be playing it safe here. “Our analysis demonstrates potential upside to 2024 numbers and beyond as NPCE expands access to RNS outside of Level 4 CECs,” Chopra said. “We do not believe that mgmt has contemplated meaningful revs in 2024 guide from Project CARE and as such, we see potential for upside revisions… we like the setup as NPCE expands into the community setting and do not believe the Project CARE opportunity is priced in.”

Conveying his confidence, Chopra rates the shares as Overweight (Buy – upgraded last month) and his price target of $20 implies an upside of 62% on the one-year horizon. (To watch Chopra’s track record, click here.)

There’s general agreement on the Street that this is a stock to buy; the Strong Buy consensus rating is based on 7 recent reviews that include 6 Buys to 1 Hold. The shares have an average price target of $17.71, suggesting a 43% one-year increase from the current share price of $12.37. (See NeuroPace’s stock forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.