Post-COVID, the domestic leisure industry saw robust demand even in the face of 2023’s growing economic headwinds. The sector had a surge in spending in the first two years after the pandemic, and while that is likely to slow down heading into 2024, industry experts still predict 2% inflation-adjusted annualized growth for domestic leisure over the next few years.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

One leisure segment with a solid outlook is the timeshare sector, and for good reason. As the Federal Reserve prepares to reduce interest rates this year, timeshares – in which vacationers purchase ownership and usage rights in shared properties – will become more affordable through less costly financing. More affordable destinations should boost vacation travel, even if the macroeconomy slows.

That’s the theory behind a New Year’s report from Jefferies analyst David Katz. He focuses on stocks in timeshare companies and comes to the conclusion that now is the time to buy them.

“The importance of interest rates in timeshare stock performance is at the heart of our thesis change. Given the active receivable creation that accompanies sales coupled with the securitization of receivables which drives a meaningful earnings stream for the companies that benefits from a widening spread, the pivot to a bullish stance is straightforward,” Katz opined.

Summing up, Katz adds, “Notwithstanding the interest rates, timeshares should be incrementally more productive given the expectation for a soft landing of the macroeconomy. Further, the businesses have proven to be more stable earnings generators than the Street expects.”

Katz doesn’t leave us with a macro view of the industry. The analyst goes on to give a drill-down to the micro level and picks out two timeshare stocks that he sees as potential winners for the long haul. We used the TipRanks database to identify what makes them stand out from the pack.

Travel + Leisure Company (TNL)

We’ll start with Travel + Leisure Company, or TNL, an established name in the timeshare industry. The company is based in Orlando, Florida – a natural place to headquarters a vacation-related firm – and operates through the development, sale, and management of timeshare properties. These are offered on the vacation and travel market through multiple brands, including well-known names such as Wyndham, Worldmark, and Margaritaville. TNL bills itself as the world leader in the membership travel destination segment.

There is a reason for that boast. TNL claims over 245 vacation club and resort locations worldwide, offering customers and members top combinations of travel content and travel services. The company counts more than 3.5 million RCI exchange members and brought in $174 million in travel and membership revenue during the third quarter of 2023, the last quarter reported.

At heart, timeshares are simply a way of making vacation resort lodgings more affordable for consumers. Owners buy a share of the property or usage rights thereon, with set allotments of time periods for use. TNL facilitates this service and has over 816,000 vacation club owners on its books. Possession of property rights – or usage rights – reduces one strain in leisure travel; timeshare owners can vacation with accommodations arranged long in advance and are less susceptible to cancellations.

In bottom-line terms, TNL leveraged this to achieve both earnings and revenue beats in 3Q23. The company’s top line came to $986 million in total revenues, up more than 5% year-over-year and some $14.3 million ahead of the forecast. The bottom line, the non-GAAP EPS of $1.54, was up 20% from the prior-year period and came in 8 cents per share better than had been expected.

For stockholders, TNL offers the incentive of a strong capital return program. The company had $210 million remaining on its share buyback authorization as of the end of 3Q23, and during that quarter repurchased $65 million worth of common stock. The company pays out a common share dividend as well, with the last payment sent out on December 29, 2023, for 45 cents per share. This annualizes to $1.80 per common share and yields 4.6%, well above the current pace of inflation.

Turning to Jefferies analyst David Katz, we find him upbeat on TNL, describing the company as ‘durable’ and noting the resilient business model. Specifically, Katz writes, “With improving interest rate spreads, TNL continues to demonstrate earnings durability of the core VOI business and Mgt. expects the recent softness in T&M to pivot positive going forward. The focus of the company is the execution of new-buyer growth, as well as normalizing loan loss provision to 18%-19% this year, as the company raised its average FICO score of its target owners. We note that TNL’s business model is inherently more resilient through cycles; we believe near-term upside is achievable in a more favorable interest rate environment.”

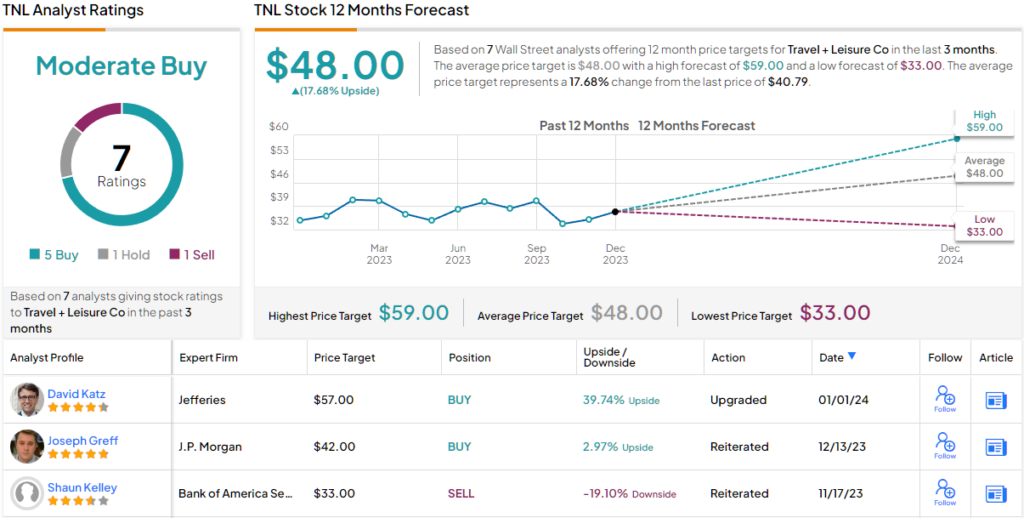

To put it in numbers, Katz gives TNL shares a Buy rating and a $57 price target. If he’s right, that could mean your TNL shares could be worth ~40% more by the end of this year. (To watch Katz’s track record, click here)

If we step back and look at the bigger picture, we can see that overall the stock has a ‘Moderate Buy’ analyst consensus rating. In the last three months, the stock has received 5 Buy ratings and 1 each Hold and Sell. The stock is selling for $40.79 after the last session, and has a $48 average target price suggesting ~18% gain in the next 12 months. (See TNL stock forecast)

Hilton Grand Vacations (HGV)

Next on the list, we’ll turn to Hilton Grand Vacations, the independent timeshare operator that originated as a spin-off from the hotel giant, Hilton, Inc. HGV is now an operator of quality, name-branded vacation timeshares in 15 states across the US. These include vacation hotspots such as California, Florida, and Hawaii, as well as resorts in major urban destinations like Las Vegas and DC. Internationally, the company owns and manages properties in Canada, the Caribbean, Mexico, Japan, the UK, and mainland Europe.

In all, HGV has 167 resorts in its portfolio of destinations and counted 526,000 members as of September 30, 2023. While the company is no longer part of the Hilton hotel chain, it retains the name and the parent company’s reputation for quality; HGV offers a high standard of customer service in its resorts and other properties. Timeshare owners can find properties in urban scenes, golf resorts, beachfronts, casinos, ski slopes, and more. Amenities at the resorts include programming for kids and adults, sports, shopping, restaurants, movies, spas – pretty much anything people look for on vacations.

While the vacation industry generally has seen gains in recent years, HGV had a tough time in 2023. The stock rose a mere 4% for the year, far underperforming the S&P 500’s 24%+ gain for the same period. The company faced several idiosyncratic headwinds that bear a closer look.

First was the wildfire in Maui. HGV has multiple properties in Hawaii, including two on the island of Maui. While neither of them was damaged by the Lahaina fire, the company took a serious hit from cancellations and reduced travel to the island.

The second hit to the stock came in November when HGV disclosed its intention to acquire Bluegreen Vacations, a resort company featuring 49 Club Resorts and 24 Associate Resorts, in an all-cash transaction valued at $1.5 billion, inclusive of debt. The deal is set to conclude in the first quarter of 2024. The noteworthy aspect here is that, as of the end of the third quarter in 2023, HGV held $227 million in cash and liquid assets, in addition to $866 million available through a revolving credit facility. After the announcement, shares in HGV fell some 6%.

Finally, in the 3Q23 earnings release, HGV showed mixed results. Quarterly revenue came to $1.02 billion, down almost 9% y/y and missing the forecast by $20 million. Earnings did better, with the 98-cent non-GAAP earnings per diluted share beating expectations by a penny.

All of this forms the background to Katz’s outlook on HGV. The Jefferies analyst believes that the Bluegreen acquisition will be a net long-term positive and that the company will recover from the Maui disruptions. He writes, “The acquisition of BVH is positive for the growth outlook by driving new owner growth, expanding geographic distribution and therefore should be accretive if the expected synergies are achieved upon successful integration. While we note the near-term business deceleration in the quarter and lingering impact from Maui, VPG maintains above 2019-levels and the company continues to execute growth initiatives, which are constructive for long-term earnings growth.”

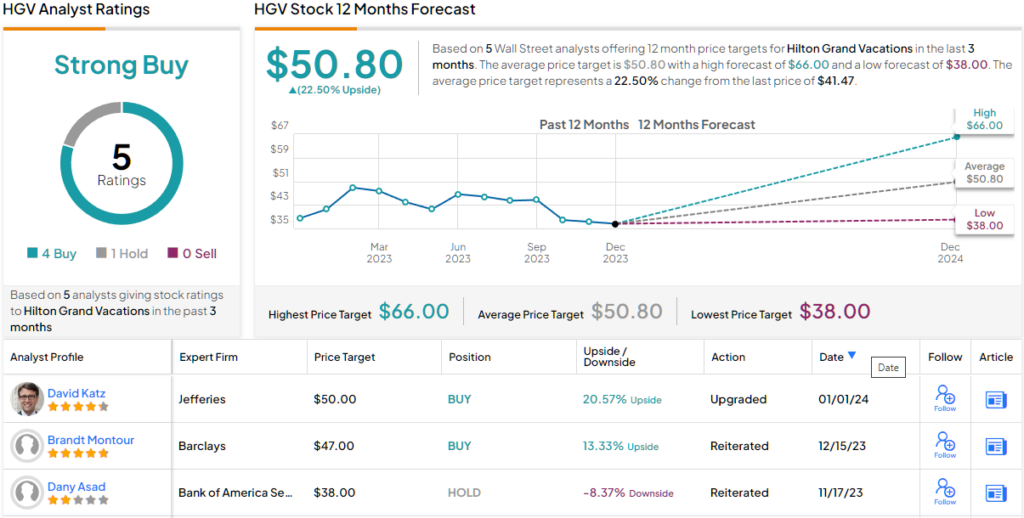

Looking ahead, Katz upgrades HGV from Hold to Buy and gives the stock a $50 one-year price target, implying an upside potential of ~21%.

Overall, there are 5 recent analyst reviews here, breaking 4 to 1 in favor of Buy over Hold – giving the stock a Strong Buy consensus rating and showing that Wall Street agrees with the bullish outlook. The average price target of $50.80 and current trading price of $41.47 together suggest an upside of 22.50% in the next 12 months. (See HGV stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.