Market volatility in recent weeks brings with it a few lessons for investors. Start with the obvious: sash-flush consumers drove the economy in the immediate post-COVID period. Move on to the macro-conditions that prevailed in the period 2021 to 2022: rising inflation that hurt consumers – but also encouraged short-term spending. Adding to last year’s twist were heightened interest rates, a slowing pace of inflation, and reduced consumer savings, all pushing in conflicting directions.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

So maybe we shouldn’t be surprised that last year’s bullish run saw some fits and starts. Even so, the year ended with solid gains. For the nation’s retail firms, the situation shows reasons for hope. As inflation slows and the Fed looks like it will ease back on interest rates, consumers are more willing to spend on goods.

A recent note from the investment banking giant Morgan Stanley puts matters in perspective for investors: “Focus on stocks with reasonable ’24 estimates and stronger ’25 EPS growth. Lower interest rates, bottoming durables and a late ’24 housing inflection make for an improving setup.”

Putting this into practical terms, Morgan Stanley’s analyst Simeon Gutman has picked out several retail stocks, pointing out that current conditions make it ‘time to buy.’ We’ve used the TipRanks platform to look up the Wall Street views of Gutman’s picks and found that they are Buy-rated with double-digit upside potential for the year ahead. Here are their details, and Gutman’s comments thereon.

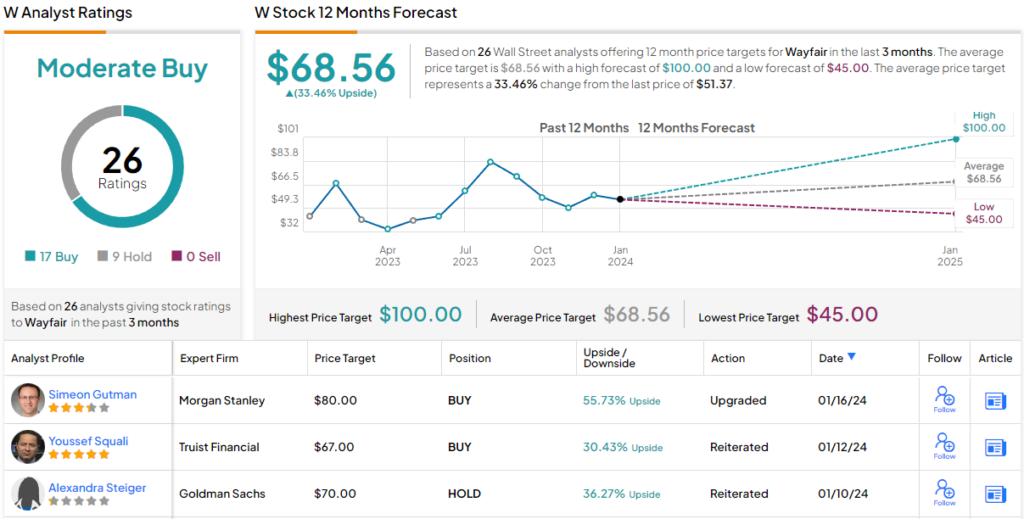

Wayfair, Inc. (W)

We’ll start with Wayfair, a Boston-based online seller of furniture and other home goods. The company is an e-commerce leader in its sector and bills itself as the ‘destination for all things home.’ Wayfair has active operations – business offices and warehouses – in the US and Canada, as well as the UK, Ireland, Germany, and China.

On the customer-facing side, Wayfair conducts its business through a family of six websites: Wayfair and Wayfair Professional, Joss & Main, AllModern, Birch Lane, and Perigold. The company sells a wide range of products, including seasonal furnishings, custom cabinets and home improvements, lighting systems, rugs, decorative items, large and small appliances, and even pet accessories. Together, these products and the company’s online outlets generated $12 billion in net revenue for the 12-month period ending on September 30, 2023.

Turning to the company’s most recent results, we find that Wayfair reported $2.9 billion at the top line for 3Q23. This was up $104 million year-over-year, or 3.7%, although it missed the forecast by $80 million. At the bottom line, the company’s non-GAAP earnings came to an EPS loss of 13 cents. We should note, however, that this beat expectations by a wide margin, at 33 cents per share. The company showed strong results in the US market, which was up 5.4% from the previous year, reaching $2.6 billion in net revenue, while international revenues fell by 7% year-over-year. The non-GAAP free cash flow, at $42 million, was positive for the second consecutive quarter.

Wayfair’s sales statistics showed that the company saw a year-over-year decrease in active customers for Q3 – the metric fell by 1.3%. The average order value also fell, from $325 to $297. On more positive notes, Wayfair reported a 13.8% year-over-year increase in orders delivered during the quarter and an increase of 16.2% in repeat customers.

Checking in with Morgan Stanley analyst Gutman, we find him upbeat, explaining why by pointing to Wayfair’s potential for strong fundamentals in the coming year.

“W fits our theme of favoring early-cycle, quality retailers with a track record of share gains and cost discipline. With growth in Home Furnishings approaching a bottom and assuming W’s share gains continue against our ‘24 category forecast, we see ~mid- to ~high-single-digit upside to Street ’24 sales estimates. Together with continued discipline in advertising spend/SOTG&A, ~mid-single-digit adj. EBITDA margins are possible in ‘24/’25. If W can deliver these sustainably stronger fundamentals – or even an outcome in-line with consensus in ‘24 (~mid-single-digit sales growth/adj. EBITDA margin) – this may trigger a structural re-rating,” Gutman opined.

Gutman comes down with an Overweight (i.e. Buy) rating on this stock, an upgrade from Neutral. His price target, of $80, points toward a one-year upside of ~56%. (To watch Gutman’s track record, click here)

This stock has earned a Moderate Buy rating from the Wall Street consensus, based on 26 recent analyst reviews that include 17 Buys to 9 Holds. The shares are priced at $51.37 and the $68.56 average price target suggests a gain of 33% in the next 12 months. (See Wayfair stock forecast)

Valvoline, Inc. (VVV)

Next up is Valvoline, a long-time leader in the market for automotive fuels, lubricating oils, and other liquid chemical products. The company markets these globally, and its product line ranges from various gasoline blends to a full gamut of engine oils, brake fluids, transmission fluids, and anti-freeze engine coolants. Additionally, Valvoline produces fuel treatments, additives, and specialized, purpose-formulated oil, coolant, and transmission fluid products needed in hybrid cars.

Valvoline’s products are available to the public through a combination of retail sellers and company-branded outlets. The company has agreements with multiple chain stores and big-box outlets, as well as independent gas stations, to sell its products. Valvoline also operates a total of 1,852 service center locations, franchised under the Valvoline Instant Oil Change and Valvoline Great Canadian Oil Change names.

While the automotive industry has faced various challenges in recent years, from labor disputes to supply chain blockages to increased costs from raw materials, Valvoline has been able to weather the storm. The company benefits from a ‘captive audience’ since every car owner requires both fuel and maintenance. While there is significant competition in these fields, the products and services are necessities. As a result, despite VVV stock’s high volatility in the past year, it has largely remained break-even for the last 12 months, and it boasts a 3-year gain of over 46%.

In November of the past year, the company reported its financial results for Q4 of fiscal year 2023. Total revenue reached $390 million, marking a more than 16% year-over-year increase and surpassing the forecast by a modest $1.19 million. In terms of non-GAAP measures, Valvoline achieved earnings of 39 cents per share, reflecting an 86% year-over-year increase; however, this fell 2 cents below expectations.

For the full fiscal year 2023, Valvoline reported $1.44 billion in revenue, up 17% year-over-year, and $1.18 per share in non-GAAP adjusted EPS, marking a 62% year-over-year increase. The company’s system-wide store total of 1,852 represents a net year-over-year gain of 48 in the quarter.

Analyst Simeon Gutman likes this stock, and in his write-up for Morgan Stanley he outlines Valvoline’s healthy growth outlook.

“We expect VVV to compound behind one of the healthiest growth outlooks in our coverage (mid teens top-line and EBITDA growth). Earnings visibility and achievability of estimates is high in our view with strong top-line trends and a more stable margin outlook than in past years, and a cleaner story post the Global Products sale. We also like VVV’s positioning as a defensive grower, which should enable the stock to perform well in various ‘24 market backdrops. Valuation at ~12.5x C’24 EV/EBITDA is fair in our view… We think the stock can grind higher on EBITDA/earnings growth, with outperformance driven by upside to estimates in our model,” Gutman opined.

This is another stock that got an upgrade from Gutman, also from Neutral to Overweight (i.e. Buy). His price target on VVV is $44, implying an upside potential of 22% on the one-year horizon. (To watch Gutman’s track record, click here.)

While there are only 5 recent analyst reviews on VVV shares, their 4 to 1 breakdown favoring Buy over Hold gives the stock a Strong Buy consensus rating. The shares are currently priced at $36.06, and the $40.60 average target price suggests a 12-month gain of ~13% from that level. (See Valvoline stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.