Despite the strong jobs numbers for April, the overall economic outlook heading toward the second half of the year remains grim. Against a backdrop of elevated interest rates and recent bank failures, the odds of a recession hitting later this year are up to 64%. It’s an environment almost tailor-made to keep investors nervous – and looking for ‘recession proof’ sectors.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

In a recent report from JPMorgan, analyst Bill Peterson sees just such an opening in the aluminum sector. Peterson has taken a deep dive into the complexities of aluminum production and products, and found that the sector presents a number of advantages that should provide long-term support, even in a downturn.

“Aluminum’s light weight and recyclability mean it will play a key role in the transition to a greener economy… J.P. Morgan’s Commodities Research team sees demand for aluminum in EVs, wind, and solar growing from around 2.4Mt in 2020 to 3.8Mt by 2025, reflecting a ~10% CAGR, which we think has significant potential for upside on the accelerated adoption of EVs based on IHS’s forecast of 23% and 45% penetration by 2025 and 2030, respectively,” Peterson explained.

Peterson isn’t just analyzing the aluminum industry as a whole, he’s also putting his finger on two stocks that he sees as winners. In fact, he’s projecting more than 40% growth potential for both of them. According to TipRanks, the premier source of analyst insights and research, these stocks also boast significant double-digit upside prospects, as evaluated by other analysts in the field. Here are the details.

Constellium SE (CSTM)

We’ll start with Constellium, a Paris-based global industrial leader, with a strong position in the manufacture of aluminum products. The company also works at the development of new uses for aluminum, and is a leader working with recycled aluminum metal. Constellium is known for its advanced alloys and engineering, and its aluminum products are found in a range of applications, from the simple soda can to aircraft, cars, and packaging.

Constellium does all of this with a truly global footprint. The company employs more than 12,000 people worldwide, and it operates 3 R&D centers and 28 production facilities in Europe, North America, and China. The company serves a wide range of industries, including Aerospace and Transportation (A&T), Packaging and Automotive Rolled Products (P&ARP), and Automotive Structures and Industry (AS&I). Major players in these fields, such as Ford, Audi, Airbus, and Boeing, are among Constellium’s esteemed clients.

One number will give the scale of Constellium’s operations, and its presence in the global metals market: 8.1 billion. In Euros, that was the firm’s total revenue in 2022. That number came to more than $8.5 billion in US currency, and marked a 17% increase year-over-year.

The company’s first quarter revenues came to 1.96 billion Euros, or US$2.1 billion; while slightly down 1% yeaer-over-year, this figure beat the forecast by 140 million Euros. At the bottom line, the GAAP EPS was reported as 14 Euro cents, missing the forecast by 22 cents.

Of interest to investors, Constellium generated 34 million Euros in cash from operations in the quarter. The firm’s free cash flow came to a loss of 34 million, due to a 68 million Euro spend on property, plant, and equipment – just the sort of capex expected to bring rewards later on. Management is guiding toward 2023 free cash flow in excess 125 million Euros.

In Peterson’s view, this company’s position in a necessary industrial niche, combined with its potential for cash generation, are the key points. He writes, “Constellium has the most upside potential among our downstream coverage, in our view, as we like its combination of end-market exposure, which can both help weather a recession in aerospace, while also providing strong, long-term growth fundamentals in packaging and auto. Strong FCF generation and pricing power, which have proved resilient through the cycle, are another plus. The slight premium to its ~6x historical average is warranted in our view given its solid FCF generation and improved balance sheet, likely enabling the company to initiate shareholder returns in 1H24.”

The JPMorgan analyst uses these comments to support his Overweight (i.e. Buy) rating on the stock, while his US$24 price target implies the stock will gain 55% in the year ahead. (To watch Peterson’s track record, click here)

Overall, this European industrial firm has picked up 5 recent analyst reviews from Wall Street, and those are unanimously positive and give CSTM its Strong Buy consensus rating. The shares are selling for $15.46 and have an average price target of $20.40, for a 32% upside potential in the next 12 months. (See CSTM stock forecast)

Alcoa Corporation (AA)

The next stock JPMorgan’s Bill Peterson is betting on is Alcoa, a Pittsburgh-based company that has long been a major player on the world’s aluminum scene. Alcoa produces high-end primary aluminum, fabricated aluminum, and alumina products, and markets and distributes them worldwide. The company works with global customers in a wide range of industries, including such commonplaces as home appliances and cookware to cars and bicycles, but also in aerospace and automobiles.

A number of rising economic headwinds have hurt Alcoa in recent months, including a wicked combination of stubborn inflation, elevated interest rates, and disrupted supply chains that work together to push up the cost of production. The company has pushed back, however, by showing that it can ‘turn green,’ tacking with the social and political winds, while still delivering quality products.

Alcoa is doing that by lowering its carbon footprint compared to traditional aluminum producers. The company’s Sustana product lines – in low-carbon aluminum, low-carbon alumina, and recycled aluminum – feature significant improvements in carbon use. The EcoDura line features a minimum of 50% recycled content, while the EcoLum low-carbon aluminum line’s carbon footprint is 3x better than the industry’s average.

Alcoa has achieved this by starting at the base, in the foundries. The company’s proprietary Elysis smelting technology is the first carbon-free smelting tech in the global aluminum industry. Using this tech, Alcoa can smelt aluminum alloys while emitting only oxygen as a gaseous byproduct.

None of this comes cheap. Alcoa’s 1Q23 results showed a top line of $2.67 billion, skating under the forecast by $90 million and declining 19% year-over-year. The bottom line non-GAAP EPS figure was a net loss, at 23 cents per share, instead of breaking even as Wall Street had expected. At the same time, the company did report an important asset – more than $1.1 billion in liquid assets on hand. With those deep pockets, Alcoa is confident that it can meet an economic storm.

What this means for JPM’s Peterson is clear from his comments on the stock: he is bullish here, and isn’t shy about saying so.

“Our view rests on a positive aluminum price outlook , given supply constraints and the commodity’s strong secular growth trends, which can help fund shareholder returns and future growth initiatives. The company has systematically improved its cash funding related to its pension and has no near-term debt obligations, which positions it well for a recessionary slowdown,” Peterson opined.

“Finally,” the analyst added, “we believe Alcoa is also well positioned for aluminum’s growing demand in the energy transition in addition to the ‘greening’ of the commodity itself with the launch of its low-carbon Sustana product line. The outlook also looks promising for its proprietary, zero-carbon Elysis smelting technology, which eliminates all scope 1 emissions associated with aluminum smelting, instead emitting pure oxygen as a byproduct.”

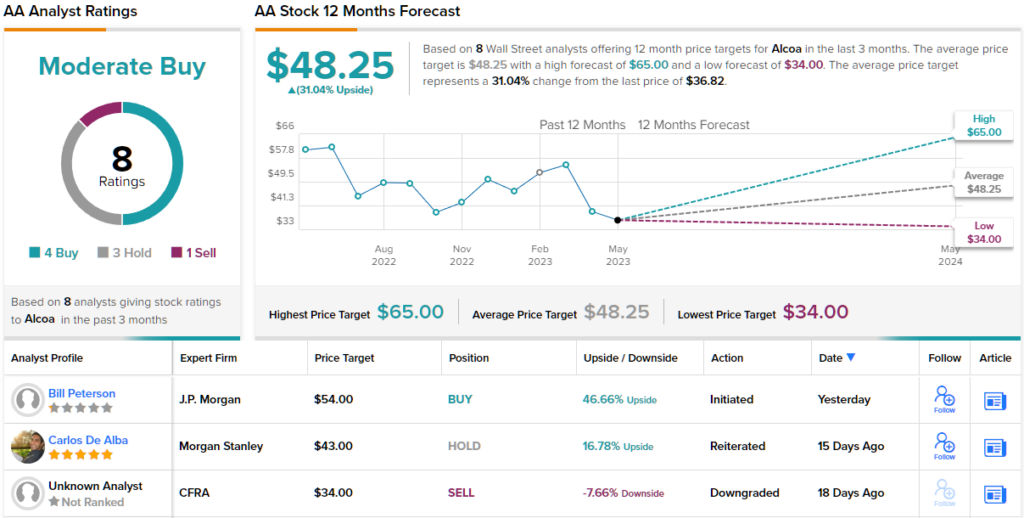

To this end, Peterson sets an Overweight (i.e. Buy) rating on Alcoa shares, along with a $54 price target that suggests ~47% share gain by year’s end.

What does the rest of the Street think? Looking at the consensus breakdown, opinions from other analysts are more spread out. 4 Buys, 3 Holds and 1 Sell add up to a Moderate Buy consensus. In addition, the $48.25 average price target indicates a solid 31% upside potential. (See Alcoa stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.