It’s easy to respect technology stalwart Intel (NASDAQ:INTC) but difficult to truly get on board with the stock. After all, its rivals like Nvidia (NASDAQ:NVDA) and Advanced Micro Devices (NASDAQ:AMD) have pressured or dominated Intel in key markets. However, those thinking about shorting its shares should think again, mainly due to bullish options activity. Tactically, I am bullish on INTC stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Positive Q3 Underlines the Fundamental Case for INTC Stock

To be clear, while the main bullish catalyst for INTC stock centers on technical dynamics to be discussed later, it’s not devoid of a fundamental argument. Indeed, a surprisingly robust third-quarter earnings print – along with better-than-expected Q4 guidance – invigorated sentiment.

As TipRanks contributor Abdulrasaq Ariwoola stated, Intel posted earnings per share of 41 cents, easily beating Wall Street’s consensus target of 22 cents per share. In addition, the tech firm rang up sales of $14.2 billion. In fairness, this tally represented an 8% decline on a year-over-year basis. However, it beat the consensus estimate by $600 million.

In addition, Intel’s EPS enjoyed a boost due to reduced expenses, per a statement by company CFO David Zinsner. As Ariwoola mentioned, “The company reported that it now employs 120,300 people, a decrease from 131,500 the previous year.”

Justifying optimism for INTC stock, management guided revenue to land between $14.6 billion and $15.6 billion. That’s considerably above the consensus estimate, which called for an average sales target of $14.31 billion. Further, Intel anticipates EPS to hit 44 cents. On the other hand, the Street projected EPS of 32 cents for the current quarter.

INTC stock gained 9% the day after reporting its earnings. However, the real story is that since the disclosure, the security failed to look back, leaving pessimists perplexed. That’s because not all of the print presented a rosy narrative. In particular, Data Center and Artificial Intelligence-related sales – including server chips – fell by 10% to $3.8 billion.

Still, it’s the options market that may keep the fire burning. Let’s dive in.

Intel Bears Remain Vulnerable to Possible Short-Covering Frenzy

As previously mentioned, while Intel delivered the goods in its latest earnings report, it still faces incredible competitive pressures. This situation seems evident in the activity of options traders, particularly institutional ones, as reflected in options flow data. The data show significant activity regarding written (i.e. sold) call options. Primarily, the concern for the bears is the open vulnerability to possible short-covering activity.

To best explain the panic effect of a sold call gone bad, it’s akin to agreeing to sell a car at a specific price and at a certain time but without actually possessing the vehicle in question. Should the car start to rise in value for whatever reason, the seller faces a choice: buy the car now to avoid further damage or wait it out and hope for the best.

Another wrinkle when it comes to the sold INTC calls is the nature of the contractual agreement. As you probably know, an option holder enjoys the right but not the obligation to exercise the contract. On the flip side, an option writer (seller) has the obligation but not the right to fulfill the contract under exercise. In other words, the writer has zero say what the countervailing party does.

So, for example, the entity or entities that sold 8,692 contracts of the Dec 15 ’23 42.00 call may be feeling hot under the collar. At the time of the transaction, INTC stock traded hands at $43.11. Now, it’s near $44.50.

More importantly, the open interest for this call stands at 9,972 contracts. Consequently, there could still be many bears exposed to this trade, perhaps requiring short covering. If short covering occurs, that would put even more upside pressure on INTC stock.

The Bears Have a Point

To be fair to the pessimists, they do have a point from a fundamental perspective. Mainly, INTC stock just isn’t that attractive when looking at its key financial metrics. For instance, the market prices INTC at a trailing-year revenue multiple of 3.5x. That’s a bit lower than the underlying semiconductor sales multiple of 3.9x.

Nevertheless, this multiple is a bit deceptive because investors don’t have much confidence in Intel’s market position. Last year, the company posted revenue of $63.05 billion, well below the prior year’s tally of $79.02 billion. So, the bullish narrative largely centers on the tactical implications of options trading, specifically the potential for short covering.

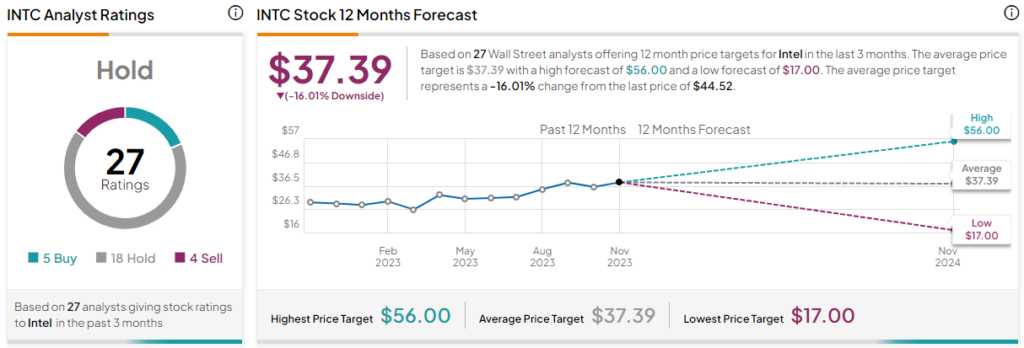

Is INTC Stock a Buy, According to Analysts?

Turning to Wall Street, INTC stock has a Hold consensus rating based on five Buys, 18 Holds, and four Sell ratings. The average INTC stock price target is $37.39, implying 16% downside risk.

Takeaway: INTC Stock Pessimists are Right, Except for One Detail

In many ways, bearish traders who don’t see much upside for INTC stock have almost every component of the narrative called correctly. In a competitive ecosystem, Intel appears to have lost its touch. However, the pessimists have so far been wrong about the contrarian bullish tactic. So long as INTC keeps marching higher, a dangerous game of chicken is in play.