Such has been the unpredictable nature of the markets and the economy in 2023, that’s it’s hard to guess what’s coming next.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

For example, it should be remembered that at the start of the year and coming off the back of 2022’s merciless bear market, few had predicted the ensuing rally that has taken place since.

Likewise, for the broader economy. Against a backdrop of soaring inflation and high interest rates, there were plenty of financial prognosticators warning of an impending vicious recession. But given the rate at which inflation has cooled lately, those calls have now been replaced by forecasts of a soft landing and a mild recession, at worst.

On the other hand, Tuesday saw big news as Fitch, one of the world’s foremost credit rating agencies, downgraded the United States’ long-term foreign-currency issuer default rating from “AAA” to “AA+.” Fitch’s decision was grounded in their anticipation of a substantial deterioration in the Federal government’s fiscal position over the next three years. Of particular concern was the agency’s observation that the repetitive debt-limit political standoffs and last-minute resolutions have severely undermined confidence in fiscal management.

So, how is an investor meant to make sense of it all? Here some expert advice could come in handy, and this is where the Wall Street analysts, such as those working at banking giant Goldman Sachs, enter the frame. It is their job after all to seek out the names that are primed to do well whatever the macro/market backdrop.

With this in mind, using the TipRanks database, we’ve tracked down two recent Goldman picks, ones which they think have strong gains in them for the coming year – on the order of 60%, or more. Let’s find out why they could surge from here.

Stagwell, Inc. (STGW)

The first stock on our Goldman-backed list is Stagwell, a marketing firm created by Mark Penn and focusing on scaled creative performance for major global brands. The company’s strategy includes the combination of human creativity with the latest data analytics, to bring the best of both to its clients. Stagwell boasts a workforce of more than 13,000, active in 34 countries around the world, driving effectiveness and improving business results.

The current incarnation of Stagwell took shape in 2021, when the company completed a merger with MDC Partners, but Penn’s firm has been in business since 2015. Stagwell has a network of over 70 agencies in its operations, and its enterprise client list includes more than 4,000 names. The firm brought in more than $2.68 billion in fiscal year 2022, for an 83% increase year-over-year.

The company appeared to hit a stumbling block as 2023 got started, however; its 1Q23 results, the last quarter reported, showed a top line of $622 million, down 3% year-over-year and missing the forecast by over $17 million. The firm’s non-GAAP earnings were reported at 13 cents per share, 7 cents per share below expectations.

On the positive side, the company reported $53 million in quarterly ‘net new business wins,’ part of a $212 million total for the trailing twelve month period.

That last metric points to Stagwell’s underlying strength; the company’s ‘digital first’ approach is well adapted to today’s marketing environment. This theme is elaborated on by Goldman analyst Brett Feldman, who uses it to bolster his upbeat take on the stock.

Feldman writes of Stagwell, “STGW is well positioned to benefit from long-term secular growth in global digital advertising and marketing spend. Specifically, we expect STGW will continue to benefit from secular tailwinds to digital advertising spend, which we expect to outpace total advertising spend by LSD through 2026E (ex-US political), as companies continue to shift mix of advertising budgets towards digital mediums.

“We believe that STGW’s valuation looks attractive based on our outlook for organic growth as well as potential upside from further M&A or other potentially accretive allocation of capital,” the analyst added.

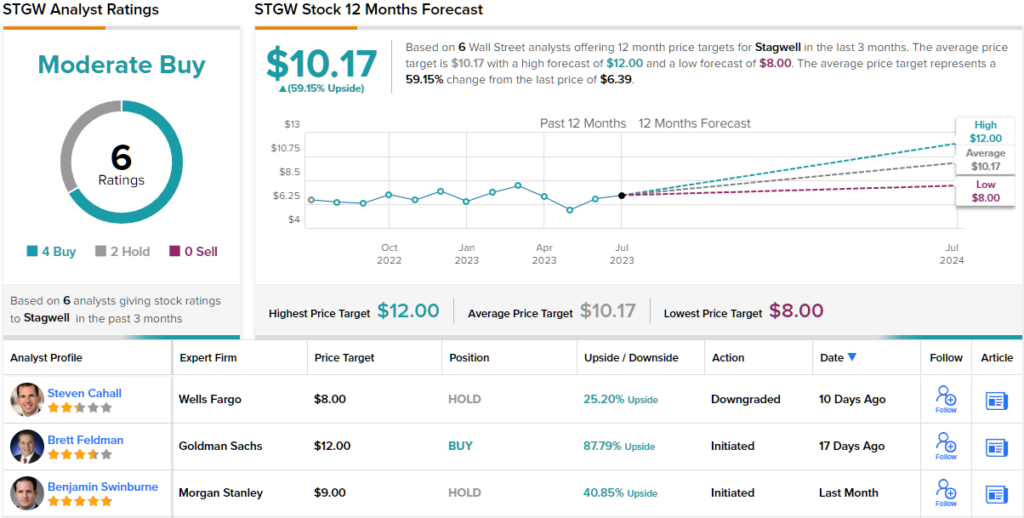

Looking forward, Feldman rates Stagwell’s shares as a Buy, and he gives the stock a price target of $12, implying a one-year gain of ~88%. (To watch Feldman’s track record, click here)

Overall, Stagwell boasts a Moderate Buy rating from the Street’s consensus based on 6 recent share reviews that break down 4 to 2 in favor of Buys over Holds. The stock’s current trading price is $6.39 and the $10.17 average price target suggests that a 59% increase lies ahead for STGW. (See STGW stock forecast)

Impinj, Inc. (PI)

From online marketing we’ll jump to the tech sector – specifically, to radio frequency identification technology, or RFID. This is a core component of the internet of things, IoT, and Impinj is a pioneer company in the field. The Seattle-based firm is a designer, maker, and distributor of RAIN RFID technology. This technology, particularly common in retail where it is a vital part of price scanning and loss prevention, is rapidly expanding into the IoT world, where it facilitates the connections that make so much of modern tech work.

Impinj’s product line includes all aspects of the RFID ecosystem. The company produces both tag and reader chips, as well as reader devices – and the software that connects them all together. Looking at some numbers reveals the scale of Impinj’s market. The company has deployed more than 4 million RFID readers in over 95 countries, and connected more than 75 billion items.

This is clearly a growth sector, and Impinj reported solid revenue gains in its recent quarterly results, for 2Q23. Nevertheless, the shares fell after the report, losing 12%. A dive into the results explains what happened.

The company’s y/y revenue growth was powerful – the total of $86 million was up almost 44% from 2Q22 and beat the estimates by $1 million. The bottom-line adj. EPS of $0.33 also trumped expectations – by 2 cents.

So far, so good. However, the company’s guidance for Q3 came in well below expectations. Revenue is expected in the range between $63 to $66 million vs. consensus at $88.11 million. Likewise, adj. EPS is anticipated to be between ($0.12) to ($0.06), way off the $0.38 the analysts were looking for.

Goldman’s Toshiya Hari acknowledges the lackluster outlook but maintains faith in Impinj’s long-term prospects.

The 5-star analyst writes, “While we are certainly disappointed by the updated outlook and reduce our forward estimates, we maintain our Buy rating on the stock with the belief that a) 2H23 will mark a cyclical bottom for the Endpoint IC business, b) the through-cycle growth prospects in RAIN RFID – based on growing adoption in and outside the traditional Retail/Apparel market – remain unchanged, and c) Impinj’s competitive advantage supported by its complete product offering (i.e. systems, endpoint ICs, software) is intact.”

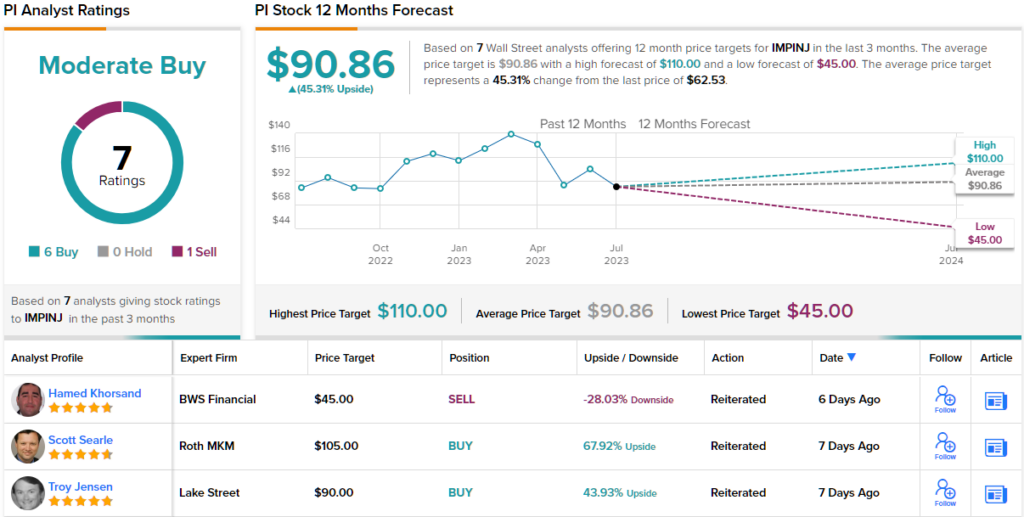

Alongside the Buy rating, Hari’s $101 price target makes room for one-year returns of 61%. (To watch Hari’s track record, click here)

There are 7 recent analyst reviews on this stock, with a breakdown of 6 Buys and 1 Sell indicating a Moderate Buy consensus rating. The shares are priced at $62.53 and their $90.86 average price target implies they will show ~45% upside in the coming 12 months. (See PI stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.