Electric vehicles, EVs, are getting plenty of headlines, and for good reason. There is a concerted push, both from governments and societal entities, to promote EVs over combustion-engine cars, and that has resulted in a global EV market that is expected to reach $561.30 billion in 2023. Almost all of the major auto manufacturers are producing EV models, and small, independent companies have been springing up in the larger markets for several years now. By 2028, the EV market is expected to reach unit sales of 17.07 million vehicles, generating a market volume of more than $900 billion.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

For the retail investor, this means that EV stocks are an area of opportunity. Projected growth on that magnitude doesn’t come often – but when it does, it means that whole industries are changing. Current EV production won’t come close to meeting the projected demand for 2028, and companies that can expand to meet that demand are going to flourish. The trick is finding them.

Wall Street’s professional stock analysts are up to the challenge. They’ve been scouring the automotive industry, looking for the EV stocks that should surge with the increased demand – and from investment firm Stifel, analyst Stephen Gengaro has picked out two stocks that investors should give a second look. These are both Buy-rated equities, and Gengaro sees 90% upside or better for each of them.

According to TipRanks’ database, Gengaro is not alone in thinking these stocks have plenty to offer investors; both are rated as Strong Buys by the analyst consensus. Let’s take a closer look.

ChargePoint Holdings (CHPT)

We’ll start our look at EV stocks with ChargePoint, a leader in the charging station niche. While ChargePoint doesn’t build actual cars, it does produce, market, and install the vital charging infrastructure that will turn EVs from a novelty into a practical transport option. The company offers a variety of charging station options for businesses, for fleet use, and for individual drivers.

The company has been operating since 2007, and its network of charging stations has expanded to the point that ChargePoint can boast of someone plugging in every 1 second or so. That has added up to more than 172 million charges delivered over the years, and ChargePoint claims 76% of the Fortune 500 companies among its customers. It’s an impressive record.

ChargePoint produced decent financial results in the recently reported first quarter of fiscal year 2024. The company showed a revenue total of $130 million, up a robust 59% from the prior year – and beating the analyst expectations by $1.67 million. At the bottom line, like many cutting-edge tech-oriented firms, ChargePoint is running at a current loss. The company’s GAAP EPS of a 23 cent loss was in-line with the forecast, while the non-GAAP figure, a 15-cent per share loss, came in better than the forecast by 2 cents.

Looking ahead, ChargePoint is guiding toward fiscal Q2 revenue in the range of $148 million to $158 million; this would represent a 41% y/y gain at the midpoint. ChargePoint has plenty of resources to continue its expansion, with $313.7 million in cash on the balance sheet as of the end of fiscal Q1 (this past April 30).

For Stifel’s Stephen Gengaro, this all adds up to a stock that investors should seriously consider, describing it as his ‘favorite EV charging name.’ He is impressed by ChargePoint’s solid position in the charging market, and its ability to expand that position.

“We reiterate our belief that CHPT is well positioned to capitalize on the expected robust growth in EV sales and charger demand over the next several years. We expect the company to deliver solid revenue growth in 2023-25+, and appears on target to deliver positive FCF by the end of calendar 2024,” Gengaro opined.

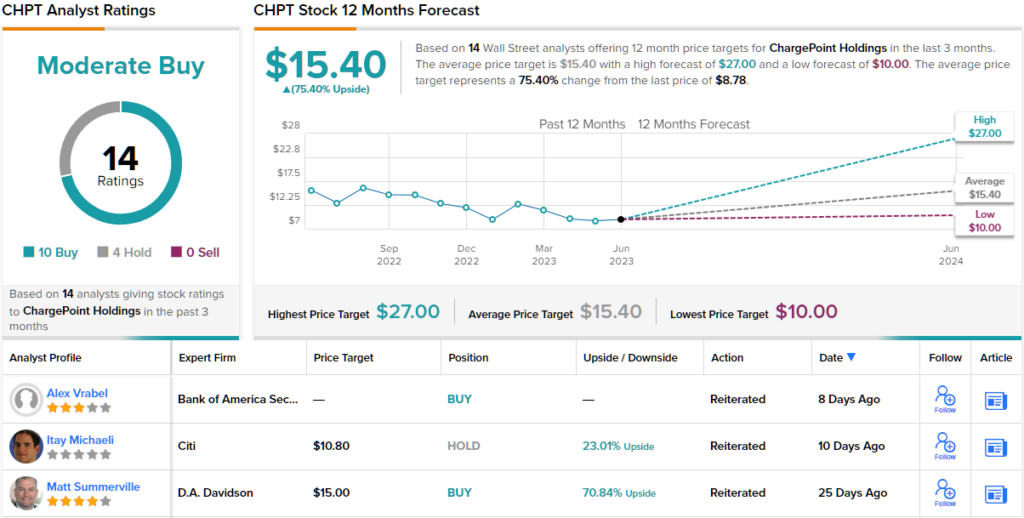

Gengaro goes on to rate CHPT shares a Buy, and his $17 price target implies a one-year gain of ~94% for the stock. (To watch Gengaro’s track record, click here)

The Street, generally, is giving CHPT shares a Moderate Buy consensus rating, based on 14 recent analyst reviews that include 10 Buys and 4 Holds. The stock’s $15.40 average price target suggests an upside of ~75% over the next 12 months, from the current trading price of $8.79. (See CHPT stock forecast)

Canoo, Inc. (GOEV)

Next up is Canoo, a California-based maker of a multi-purpose EV platform, a vehicle chassis that is adaptable to a variety of EV types and models. Canoo is working on several types of EV vehicle designs, based on this common platform. End designs include a ‘lifestyle’ vehicle, a light- to mid-duty type pickup truck, and a delivery vehicle targeting the ‘last mile’ niche. That last is an operational mode in which EVs have proven successful, as their combination of short to moderate range and zero emissions are a good fit for urban stop-and-go delivery driving.

Canoo’s EV chassis features several innovative elements. The company’s vehicle design includes independent electric motors on all four wheels, which reduces the weight and complexity of the drivetrain. Additionally, it incorporates electrically powered steering capable of ‘drive-by-wire.’ The dashboard is streamlined, offering the driver and front passenger a wide field of view. Moreover, the steering column can be shifted between the driver and front passenger seats. The vehicle comes with wireless connectivity, and users can download a mobile app that allows them to monitor the vehicle from any location.

With all of this, it’s important to note that Canoo has not yet put its vehicle into regular production. The company has recently entered agreements with Walmart and Zeeba for the purchase of 4,500 and 3,000 vehicles, and these add to an already substantial order backlog. But – the company burns cash and it’s having trouble raising capital. In 1Q23, Canoo reported no revenue and a GAAP net loss of 22 cents per share, 4 cents per share worse than was expected.

Stifel’s Gengaro acknowledges that this is a highly speculative stock, not for the risk-averse, but believes that, if Canoo can survive its financial difficulties then the rewards will be worth it.

“We view Canoo as a high-risk, high-reward stock due to its ongoing financing needs and risks associated with ramping production volumes to profitable levels. We are confident that demand for Canoo’s vehicles is strong, supported by a committed backlog of 18,000 units, another $2.8 billion of orders (~60,000 units), and our belief in both the consumer and commercial versions of its EVs,” Gengaro explained.

“We believe there are three key drivers to the stock over the next 12-24 months, including 1) reaching production targets; 2) funding operations; and 3) delivering positive gross margins. In our view, all three of these are closely linked, and start with funding,” the analyst added.

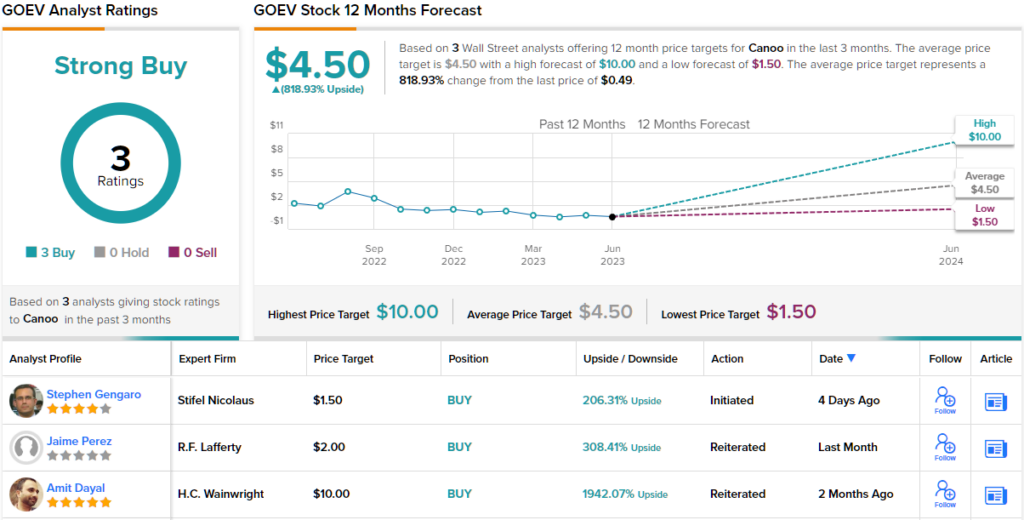

To this end, Gengaro rates GOEV shares a Buy, and his $1.50 price target indicates room for a 207% gain in the year ahead.

Gengaro is not alone in his willingness to take a risk on GOEV; the stock has 3 recent analyst reviews, all positive, for a unanimous Strong Buy consensus. The shares are trading for just $0.49, and the $4.50 average price target implies a sky-high potential appreciation of ~819% on the one-year horizon. (See Canoo stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.