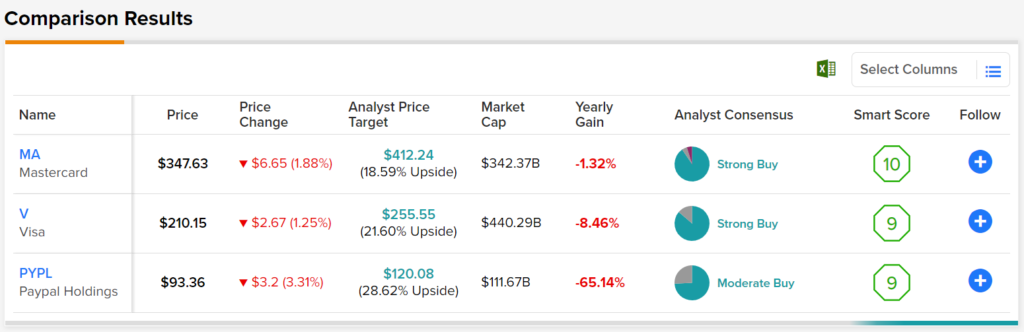

In this piece, we used TipRanks’ Comparison Tool to look at three different payment plays that Wall Street hasn’t yet turned its back on. With Buy ratings and positive year-ahead upside, shares of Visa, Mastercard, and PayPal seem like compelling pick-ups for investors who believe in the resilience of the consumer.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Payments stocks have taken a massive hit to the chin in recent quarters. With a recession likely to happen in early 2023, there’s fear that consumers may continue to tighten their purse strings. Indeed, those built-up cash cushions from pandemic lockdowns will eventually be exhausted. Though it’s difficult to tell when consumers will begin to really cut discretionary spending, many payment stock investors seem unwilling to stick it out through the vicious volatility.

From fintech-flavored payment plays to traditional credit card companies, it’s been tough to make any money in the space of late. As more recession is baked into share prices, I’d be more inclined to take a contrarian position, even before a recession becomes official. The next recession is unlikely to be like those in the past. Consumer spending may not fade as quickly as markets expect, and that’s where the real upside from payments plays comes from.

Visa (V)

Visa and the credit card giants have held their own far better than the many fallen fintech startups amid rising interest rates. Though Visa stock hasn’t gone anywhere since the market peaked in early 2020, the firm has been steadily beating analyst expectations.

Following yet another earnings beat in its third quarter, it’s clear that Visa was more resilient in the face of macro storm clouds than most thought. Visa’s revenue surged 19% year-over-year, while margins crept higher by 60 basis points.

As a market leader, the bears would argue Visa’s dominant share is for it to lose. However, given how much pressure fintech startups have been under in recent months, I think the heavyweights like Visa will gain the upper hand.

Profits matter when rates rise, and though unprofitable fintech startups posed some risk to the payment darlings like Visa, I think it’s becoming clear that the disruptive impact of said startups was vastly overblown.

At the end of the day, Visa is an innovative company, too. The only difference is it has powerful network effects on its side and actual profits to show.

The only knock against Visa is the valuation. The stock trades at 16.3 times sales, which is pricier than some of its higher-growth, unprofitable counterparts in fintech. Though Visa deserves a premium for its moat, I’m not so sure the current multiple leaves much in the way of a margin of safety.

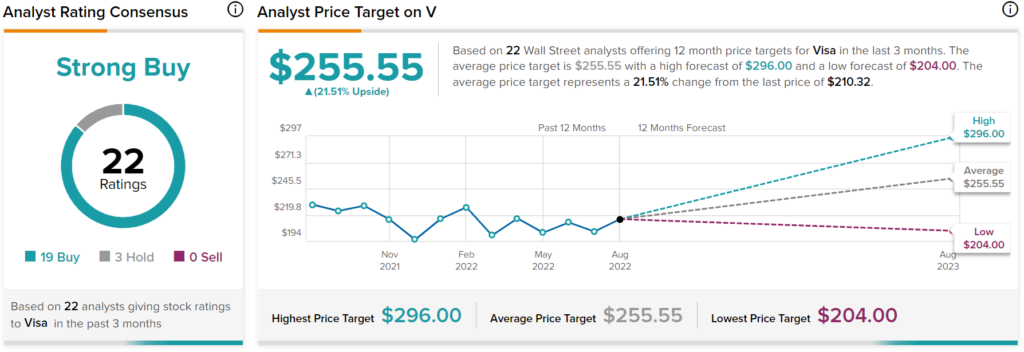

In any case, Wall Street loves Visa stock. They think Visa deserves its multiple and assigned 19 Buys and three Holds to it. Visa Stock’s price target is $255.55, which equates to more than 20% gains.

Mastercard (MA)

Speaking of credit card companies with tech prowess, Mastercard is a beast in its own right. At 16.9 times sales, Mastercard is more expensive than Visa, but only slightly. For the slight premium, investors gain a lot more in the way of innovation.

The firm sees itself making big moves in cybersecurity and even cryptocurrencies. Sure, the crypto and blockchain boom may be coming to an end, but Mastercard is still exploring the technology. With so much profit to show, the risks of having nothing to show for crypto projects are far lower than they are for some of the crypto pure-plays out there.

Like Visa, Mastercard is on an earnings-winning streak. The latest second quarter came in far better than expected, with Mastercard posting $2.56 in per-share earnings, much higher than the $2.36 estimate. Revenue grew 21% year-over-year, or 27% when neglecting the effect of the strong dollar. That’s still remarkable growth in the face of subtle economic pressures.

I think the winning streak will continue, even in the face of macro headwinds. While a recession is bad news for digital payments, I see Mastercard scraping some market share away from fallen fintechs that may need to curb their growth pace.

Wall Street is still a big fan of Mastercard stock, with 19 Buys, one Hold, and one Sell assigned in the past three months. The average MA stock price target is $412.25, which has slightly lower upside potential than Visa, calling for an 18.4% gain over the next year.

PayPal (PYPL)

Finally, we have PayPal, the hardest-hit of the payments plays on this list. The stock peaked back in July 2021 and was a canary in the coal mine for the tech sector. It came as a shock to many to see the blue-chip fintech play shedding 75% of its value. Though shares have found their footing again, it’s doubtful that PayPal will surge past $300 per share anytime over the near future.

The stock was way overvalued, and it took higher interest rates for the market to drag the name back down. Despite intriguing innovations, PayPal looks no more innovative than a credit card company. The firm may have a toe in the BNPL (Buy Now Pay Later) and crypto waters, like Visa and Mastercard. However, it’s becoming clear that BNPL and crypto aren’t nearly as exciting as they once were.

After a vicious pummelling, PYPL stock trades at 55.3 times trailing earnings. At 4.4 times sales, the fintech may actually be a tad cheaper than the credit card firms.

Though PayPal’s ecosystem, which includes Venmo, is worth a premium, I think the network effects of the credit card firms warrant a greater multiple.

Looking ahead, PayPal is doubling down on digital payments, with a focus on e-commerce. The prior acquisition of Honey could help improve upon its ecosystem and help differentiate itself from other payment pure-plays. With plenty of dry powder on the balance sheet, I think PayPal needs to make a big acquisition if it’s to regain its former double-digit price-to-sales (P/S) multiple again.

Despite greater uncertainties, Wall Street still thinks PayPal is a great value, with 23 Buys, eight Holds, and zero Sells. The consensus PYPL price target also calls for 28.5% upside. That’s not a great return if you rode the stock all the way down from over $300 per share. Still, the risk/reward seems decent for new investors.

Conclusion – Analysts Expect PYPL Stock to Deliver the Highest Returns

Payments plays have been weighed down of late. Credit card firms have held their own better but can’t seem to pick up traction as investors fret over a looming consumer slowdown. Of the three stocks in this piece, analysts expect the most from PayPal on the returns front. Personally, I like Mastercard for its resilience and tech capabilities, which rival that of disruptive fintechs.