Risk and reward are the watchwords of all investing, and that’s especially true in the stock markets. Business cycles turn up and down, economies rise and fall, companies succeed or fail on idiosyncratic grounds – it takes a special kind of risk tolerance to try and read the tea leaves scattered on Wall Street.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

But the savvy investor knows that tolerating risk is the key to success – and that few stock segments offer a better reward potential, for the risk involved, than the penny stocks. These shares, priced under $5 each, can offer an attractive combination of low cost of entry and solid potential for high-percentage returns, and triple-digit share appreciation is not uncommon. The risk – if these shares turn south, the losses can be just as heavy.

Still, for the risk-friendly investors, the ‘pennies’ are a popular choice, and that brings these low-cost shares onto the analysts’ radar screens. In fact, two in particular have caught the experts’ eyes – for their potential to surge over 200%. Furthermore, according to the TipRanks database, each has earned a “Strong Buy” consensus rating from the analyst community.

Clearside Biomedical (CLSD)

We’ll start with Clearside Biomedical, a medical research firm focused on ocular health. Specifically, Clearside is working on the development of new treatments for serious diseases that affect the back of the eye. The company describes its goal as restoring and preserving vision, and has developed a patented suprachoroidal space (SCS) microinjector, a novel delivery mechanism that can direct the therapeutic agent directly to the back of the eye.

Clearside currently has one product, Xipere, approved for use in the US. This is the firm’s first commercial product, and the first approved therapeutic agent designed specifically for SCS delivery. The drug is a treatment for macular edema associated with uveitis, the first such therapy on the market, and has been licensed to Bausch + Lomb for commercialization in the US and Canada.

In addition, the company is working on a pipeline of small-molecule drug candidate compounds suitable for the SCS microinjector system, designed to take maximum advantage of that novel pathway in the treatment of eye diseases. The most notable of these, CLS-AX, is a treatment for neovascular age-related macular degeneration, or wet AMD. CLS-AX, or axitinib, has the high-potency and pan-VEGF attributes of TKI axitinib, combined with the specialized use of the targeted SCS microinjector delivery. The drug candidate’s small molecule suspension allows for enhanced durability.

CLS-AX is undergoing a Phase 2b ODYSSEY trial, a test of the drug as delivered by the SCS microinjector in the treatment of wet AMD. The company is progressing with the trial, and recently reported that randomization has been completed. Topline data is expected from this clinical trial in 3Q24.

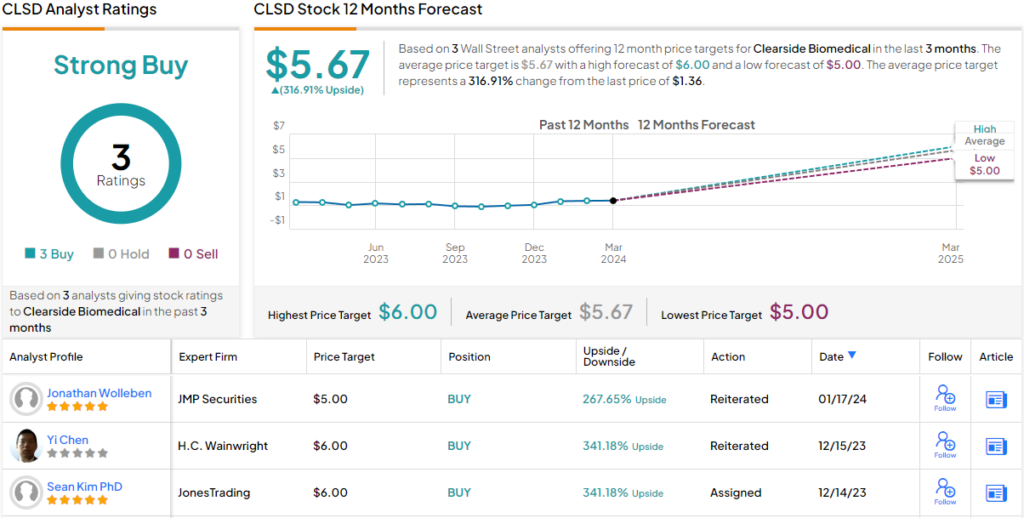

The ODYSSEY trial, and the potential inherent in the CLS-AX drug candidate, caught the attention of JMP’s Jonathan Wolleben, a 5-star analyst rated in the top 3% of the Street’s stock pros.

“We continue to recommend CLSD shares ahead of its ODYSSEY data, which we think have a high likelihood of showing improved durability vs. Eylea. While ODYSSEY is not powered for noninferiority on its primary BCVA endpoint, management expects CLS-AX will have similar results to Eylea, with all CLS-AX treated patients going >/=4 months before requiring rescue, and the majority lasting six months. ODYSSEY enrolled quickly and exceeded the 60-patient target, reflecting wet AMD patients’ enthusiasm for CLS-AX… We believe CLSD has the most room for upside in the group and is worth investors taking a look before the company reports [the] Phase 2 data in 3Q24,” Wolleben opined.

To this end, Wolleben rates CLSD an Outperform (i.e. Buy) along with a $5 price target. This implies shares could soar ~268% in the next year. (To watch Wolleben’s track record, click here)

Wolleben is not the only analyst to see a solid upside here; all three of this stock’s recent reviews are positive, resulting in a Strong Buy consensus rating. The stock is trading at $1.39, and with an average price target of $5.67, the upside potential amounts to approximately 317%. (See CLSD stock forecast)

Accuray Inc. (ARAY)

Next up is Accuray, a radio-oncology company that develops and manufactures medical devices for the delivery of accurate radiotherapy doses for cancer treatments. Targeted radiation doses have long been used in cancer treatments, to kill tumor cells and other malignancies; the key to success is as much in the precision of the targeting as in the type of radiation used, to avoid or minimize damage to and effects on healthy cells and tissue. Accuray has developed a line of products to deliver radiation treatments for a wide range of patient needs and has built up a global base of customers in the medical field.

Some numbers will tell the story. Accuray has installed more than 1,000 systems overall and has activities ongoing in more than 60 countries. The company’s total revenues in fiscal year 2023 came to $447.6 million – and the firm was able to reinvest 12% of that revenue back into research and development projects, to maintain its radiotherapy systems at the cutting edge of both technology and current medical practice.

The company’s two leading products are the CyberKnife and Radixact. The first is a treatment unit designed to deliver stereotactic radiosurgery and stereotactic body radiation therapy with ‘robotic precision’ to any part of the patient’s body. The unit is AI-driven and offers real-time motion synchronization. Radixact is an integrated 3D kVCT and megavoltage CT imaging system, designed to provide the advanced imaging needed for image-guided intensity-modulated radiation therapy and for 3D conformal radiation therapy. In short, improving precision is in Accuray’s DNA.

Also of note for investors, Accuray announced last October that its Tomo C system, a radiation therapy system for the Type B market, has been approved by the Chinese National Medical Products Administration for use in that country. The new system is made in China and represents an advance in the use of radiotherapy for cancer treatments. Tomo C is based on a platform that features helical imaging and radiation delivery.

The Tomo C system is targeted at emerging markets, particularly in China where it is manufactured. Accuray is also working on the launch of Helix, a similar system scheduled to launch in FY25 in India. Helix will also use a helical delivery system and will be manufactured by Accuray in Madison, Wisconsin.

In Accuray’s last earnings report, released on January 31 for fiscal 2Q24, the company reported revenues of $107.2 million. This was down 6.6% from the prior year, but slightly beat the forecast by about half a million dollars. The company’s earnings, at a 10-cent per share loss by GAAP measures, missed expectations by 5 cents per share.

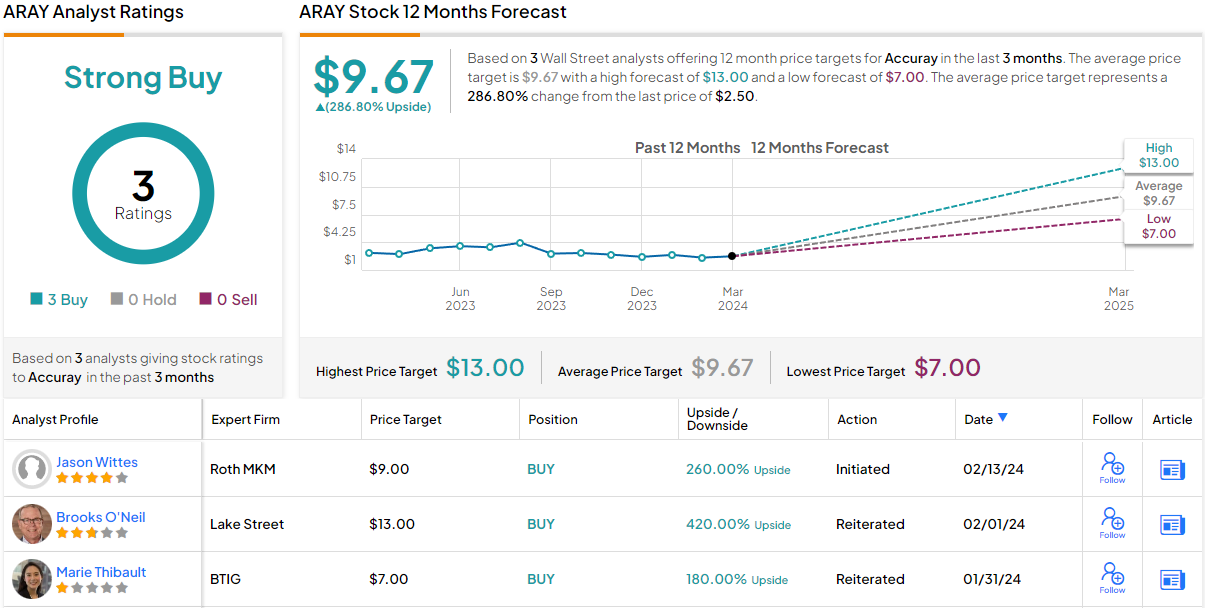

Despite the earnings miss, Roth Capital analyst Jason Wittes likes this stock. He notes especially the company’s moves into emerging markets, citing both China and India, and predicts sound growth in the long term. Wittes says of Accuray, “ARAY has about 10% market share in the radiation oncology space and is now reliably generating cash. Expansion into the value priced segment with Tomo C (first installs in June FY4Q24) in China and Helix in India in FY25 positions ARAY to compete more effectively in faster growing emerging markets. This expansion should boost revenue growth from low-mid-single digits to at least mid-high-single digits, warranting investor attention and a higher valuation.”

Looking ahead, Wittes rates ARAY shares a Buy and his $9 price target indicates confidence in a robust 260% upside for the next 12 months. (To watch Wittes’ track record, click here)

Overall, the analyst consensus here is a Strong Buy, based on 3 positive ratings set in recent weeks. The shares are currently trading for $2.52 and their $9.67 average price target implies a one-year upside potential of ~287%, somewhat higher than analyst Witte allows. (See Accuray’s stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.