Whether you love them or hate them, penny stocks are contentious. These tickers, which trade for less than $5 per share, have earned a reputation on Wall Street for their divisive nature, leaving investors struggling to find common ground on the matter.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

The appeal is clear. For the same price as one share of a more well-known company, investors can snap up hundreds of shares of a penny stock. What’s more, the fact that even minor share price appreciation can translate to irresistible percentage gains entices some investors.

It’s also understandable why some investors are wary. Opponents are quick to point out that there could be a very real reason these stocks are changing hands for pocket change, with the low share prices often masking obstacles like weak fundamentals or troubling headwinds.

No matter which side you take, one thing is certain: due diligence is necessary before making any investment decisions. That’s where the Wall Street experts come in. These pros bring experience and in-depth knowledge to the table.

With this in mind, we turned to investment firm Piper Sandler for some inspiration. The firm’s analyst, Yasmeen Rahimi, has pinpointed two compelling penny stocks, noting that each offers massive upside potential and could climb to $25 or even higher. In fact, it’s not only Rahimi who is getting behind these names. According to the TipRanks database, both stocks are rated as Strong Buys by the analyst consensus.

Immunic, Inc. (IMUX)

We’ll start with Immunic, a clinical-stage biopharmaceutical firm at the forefront of developing orally administered small-molecule immunotherapies for chronic inflammatory and autoimmune diseases. Immunic’s work focuses on orally dosed medications, which is an important consideration. Many new drug treatments for autoimmune diseases require intravenous administration, with all the discomfort and inconvenience that entails for the patient. An orally dosed treatment avoids these difficulties.

The company’s current pipeline includes several drug candidates, two in the clinic and one in pre-clinical testing, targeting multiple sclerosis, ulcerative colitis, and celiac disease. The company’s leading program targets multiple sclerosis, and is at Phase 3 in clinical trials.

On the clinical side, Immunic’s leading program is IMU-838, vidofludimus calcium, which is being tested as a treatment for both relapsing and progressive multiple sclerosis, and moderate-to-severe ulcerative colitis. The first of these tracks, on relapsing MS, is the most advanced, in a Phase 3 clinical trial. Earlier Phase 2 trials of this drug candidate showed clinically significant therapeutic activity in the treatment of MS. In April of this year, the company also announced positive Phase 2b data on the use of IMU-838 in the treatment of ulcerative colitis.

The company’s second leading pipeline program is IMU-856, under investigation as a treatment for celiac disease. This drug candidate has been exceeding the company’s expectations, showing success in proof-of-concept trials and in early-stage clinical testing. The company is preparing a Phase 2b trial of IMU-856 in patients with ongoing active celiac disease.

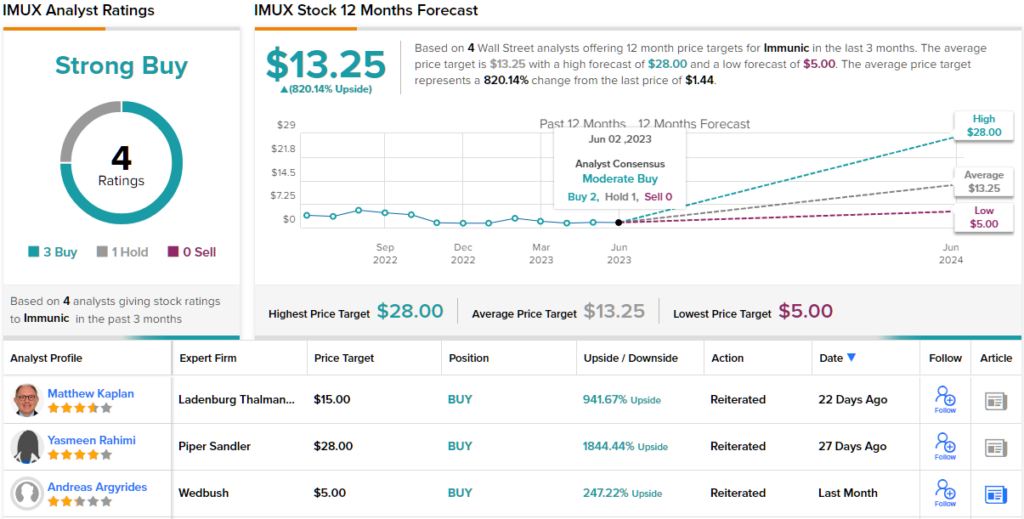

Based on the potential of the company’s drug candidates, and its $1.44 share price, Piper Sandler analyst Yasmeen Rahimi thinks that now is the time to get in on the action.

“We continue to believe that IMUX is an undervalued stock as we head into two key events on the horizon across two strong assets: 1) IMU-838 in ~225 PMS patients on track to read out key biomarker MFL and GFAP data in 2H23, and 2) initiation of a Ph2b celiac disease study with IMU-856 following the positive topline results from the Ph1b part C, where mgmt’s next steps will involve working diligently on the protocol and design to as quickly as possible submit an IND filing in the US to start regulatory discussions. Altogether, we continue to have high conviction for the success across the IMUX pipeline,” the analyst opined.

To this end, Rahimi rates IMUX an Overweight (i.e. Buy) and her price target, set at $28, implies an impressive upside of 1,844% over the next 12 months. (To watch Rahimi’s track record, click here)

So, that’s Piper Sandler’s view, how does the rest of the Street see the next 12 months panning out for IMUX? Based on 3 Buy ratings and 1 Hold, the analyst consensus rates the stock a Strong Buy. The $13.25 average price target indicates shares could skyrocket 820% in the next year. (See IMUX stock forecast)

Altimmune, Inc. (ALT)

The next penny we’ll look at is Altimmune, a clinical-stage biopharma firm with a focus on peptide therapeutics, a class of drugs with applications for liver disease and obesity-related conditions. Altimmune’s peptide research track is creating novel therapeutic agents, with plenty of potential in the treatment of several serious health conditions.

The company’s pipeline currently features three tracks, all in the clinic. Two of these tracks are studying the leading drug candidate pemvidutide. This is a GLP-1/glucagon dual receptor agonist which has shown clinical trial successes in the treatment of both obesity and nonalcoholic steatohepatitis, a type of fatty liver disease. The company’s third research track features HepTcell, an immunotherapeutic agent under development by Altimmune for the treatment of the life-threatening chronic viral disease, hepatitis B.

These three tracks form a compelling picture for investors to consider. In March, the company announced positive data from the 24-week segment of the MOMENTUM Phase 2 trial of pemvidutide in the treatment of obesity, and is currently running a 48-week section of the same trial. Topline results from the 48-week MOMENTUM trial are expected in 4Q23.

Altimmune is also running the Phase 2 trial of HepTcell, which it hopes can become a functional cure for chronic hep-B. Results from this trial are expected for release in 1Q24.

Finally, the company is the process of initiating the Phase 2b trial of pemvidutide in the treatment of NASH. This trial will run for 24 weeks, after which patients should experience reduction in NASH and fibrosis, followed by an additional 24 weeks of treatment. If patients experience GI intolerance, a dose reduction will be permitted. The company expects to have topline results by 1Q25.

Despite the rich pipeline of therapeutic candidates, Altimmune shares are down 71% over the past 12 months. According to Piper Sandler’s Yasmeen Rahimi, this presents an opportunity for the stock to undergo substantial growth.

“We believe this stock has been overly punished by Street despite strong pemvidutide MOMENTUM interim data that showed competitive weight loss and some of the strongest liver defatting as we have seen from the NAFLD data. That said, we believe Ph2b IMPACT in NASH with initiation expected in mid-2023 is significantly de-risked. Furthermore, we think that full 48-week MOMENTUM (n=320) will rejuvenate investor interest in the name. Furthermore, we believe there is a compelling story for pemvidutide as ALT engages in potential partnership discussions for both obesity and NASH,” the analyst opined.

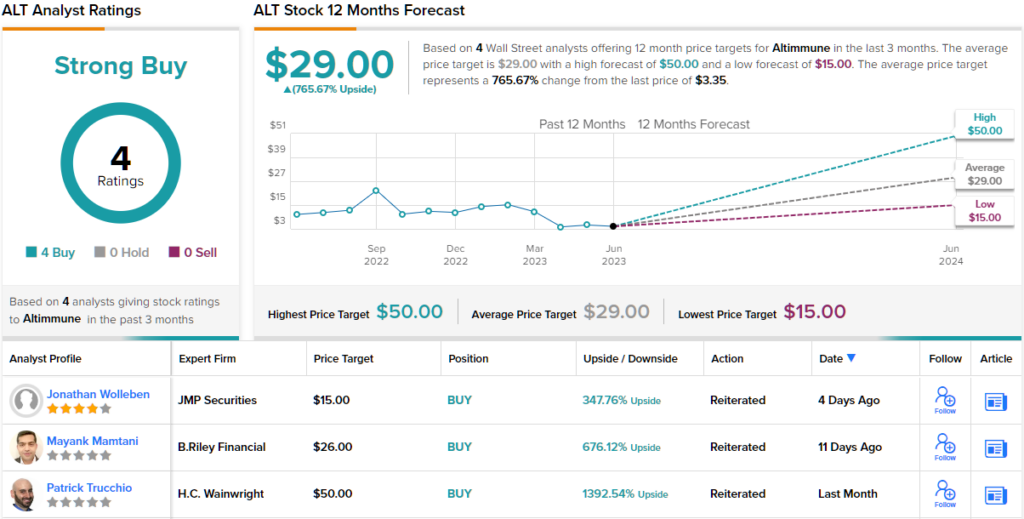

Looking forward, Rahimi rates ALT an Overweight (i.e. Buy) rating, along with a $25 price target that indicates potential for a strong 646% upside by the middle of next year.

Overall, this stock has earned a unanimous Strong Buy consensus rating from Wall Street, based on 4 recent positive analyst reviews. The average price target, at $29, points toward a robust 765% 12-month upside from the current trading price of $3.35. (See ALT stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.