‘Audentes Fortuna iuvat,’ wrote Virgil in his classic epic, the Aeneid. The saying, translated as ‘Fortune favors the bold,’ means that Fortuna, the Goddess of luck, is more likely to help those who take risks or action.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The stock market gives us one of the clearest examples of this principle with penny stocks. These low-cost shares, listed at $5 or less, present a rock-bottom entry point, making them true gold for the risk-tolerant investor.

The appeal is clear. For the same price as one share of a more well-known company, investors can snap up hundreds of shares of a penny stock. What’s more, the fact that even minor share price appreciation can translate to hefty percentage gains is too enticing for some investors to ignore.

Although penny stocks can deliver massive returns, there could be a reason they are changing hands at such low levels. Finding themselves in challenging times, these names could be bogged down by overwhelming headwinds or poor fundamentals.

So, how should investors approach a potential penny stock investment? By taking a cue from the analyst community. These experts bring in-depth knowledge of the industries they cover and substantial experience to the table.

Bearing this in mind, we used TipRanks’ database to pinpoint two penny stocks getting rave reviews from Piper Sandler, with the firm’s analysts forecasting a potential rally of over 300%, setting a target price of $9 for each. Adding to the good news, both tickers boast a ‘Strong Buy’ consensus rating from the rest of the Street. Let’s take a closer look.

Unicycive Therapeutics (UNCY)

We’ll start with Unicycive Therapeutics, a biotech company focused on the treatment of hyperphosphatemia. This condition is a common side effect of chronic kidney disease (CKD) and is a leading cause of excess death in dialysis patients. Hyperphosphatemia is particularly dangerous because it is symptomless and can only be tracked by frequent blood tests. Even when controlled, it still imposes a burden on patients; CKD is the chronic illness with the highest ‘pill burden’ – a median of 19 prescription pills taken daily by patients, even higher than for AIDS or congestive heart failure.

Unicycive aims to both treat hyperphosphatemia and reduce the pill burden on patients, with the goal of improving medication compliance and thus also improving medical outcomes. The company’s leading drug candidate, oxylanthanum carbonate (OLC), is tailored for just this purpose. The drug candidate is a phosphate binder that uses the already-known phosphate binding capabilities of elemental lanthanum to create a hyperphosphatemia treatment that is more effective, at a lower dose, and with smaller pills than current treatments.

The company has completed enrollment in a pivotal late-stage clinical trial, conducted in an open-label, single-arm, multicenter, multidose format. Anticipated in late 2Q24, the release of topline data from this trial marks a crucial step forward in Unicycive’s journey towards transforming hyperphosphatemia treatment.

In addition to OLC, Unicycive is also developing UNI-494, a new drug candidate for the treatment of acute kidney injury. This drug candidate has been granted the FDA’s Orphan Drug designation in delayed graft function of the acute kidney injury indication. Orphan Drug designation is an important regulatory step in the development of therapeutic agents for conditions with small patient bases.

With UNCY shares trading at $1.02, this attractive valuation has caught the eye of Piper Sandler analyst Yasmeen Rahimi, who is upbeat on the potential sales for OLC should it receive approval.

“This micro-cap name is trading at ~cash and significantly below its value, in our view, but we think this hidden gem has major upside ahead of OLC approval. Specifically, lead asset, OLC, is a wholly-owned phosphate binding agent currently in late-stage development for hyperphosphatemia, which universally affects CKD patients. CKD is a blockbuster market with >500K undergoing kidney dialysis (~80% on phosphate binders), driving ~$1.125B in US sales in 2021 ($2.5B globally). As ARDX (hyperphosphatemia comp) trades at a market cap of ~$1.71B, we think this highlights that UNCY is undervalued, flying under investors’ radar,” Rahimi opined.

“Accordingly,” Rahimi sums up, “we are bullish on UNCY ahead of its key, near-term stock moving catalysts with topline OLC 16-week Ph2 CKD dialysis tolerability data late 2Q24, NDA filing mid-2024, and potential approval mid-2025.”

To this end, Rahimi rates UNCY an Overweight (i.e. Buy), while her $9 price target indicates room for a potential one-year upside of a whooping 791%. (To watch Rahimi’s track record, click here)

Overall, UNCY shares hold a Strong Buy rating from the analyst consensus, based on 4 unanimously positive reviews. With the average price target clocking in at $5.88, shares could soar 482% from current levels. (See UNCY stock forecast)

Taysha Gene Therapies (TSHA)

Next up is Taysha Gene Therapies, a biotech company with a focus on the development of adeno-associated virus (AAV)-based gene therapies for severe monogenic diseases of the central nervous system. The company is looking to create an adeno-associated virus delivery system, capable of inserting a spliced gene into a damaged genome. It’s designed for one-time dosing, to deliver a corrected copy of the MECP2 gene to central nervous system cells, thereby addressing the genetic root cause of the disease condition.

Specifically, the company is working on a gene therapy to target Rett syndrome, a serious developmental disorder of the brain. Rett patients typically develop the disease in their first year, and progressively lose motor function abilities – such as crawling or standing – which they previously had. Over time, the disease continues to impact motor function, as well as communication. Rett syndrome is more frequent in females than males, and has no effective therapies.

Taysha’s lead asset is TSHA-102, a self-complementary intrathecally delivered AAV9 gene transfer therapy specific to Rett. The drug therapy is designed for one-time dosing, to deliver a corrected copy of the MECP2 gene to central nervous system cells, thereby addressing the genetic root cause of the disease condition. The drug candidate is currently undergoing two Phase 1/2 clinical trials, the REVEAL adolescent and adult study, in the US and Canada, and the REVEAL pediatric study in the US and the UK. Early data from both studies, based on two patients, showed a well-tolerated safety profile for the drug candidate, and an absence of adverse effects linked to the therapy. Based on these results, the company plans to advance the trials to a second cohort at a higher dose.

For analyst Christopher Raymond, covering this stock for Piper Sandler, this leading drug candidate offers plenty of reason for optimism.

“We believe this company’s lead asset – TSHA-102 – is poised to transform the treatment paradigm for Rett syndrome – a rare, genetic neurodevelopmental disorder with a high unmet need, despite the existence of an approved therapy. With what we see as meaningfully derisking clinical data in hand, and further derisking data anticipated near-term, we think the stock is set to inflect meaningfully higher as soon as mid-2024, with additional drivers toward year-end,” Raymond opined.

“Bottom line, TSHA-102 represents what we see as a $900M+ revenue opportunity. With TSHA’s current $500M market cap, we believe the stock has only just started to reflect this potential. We would be buyers in front of this year’s value inflection events,” Raymond summed up.

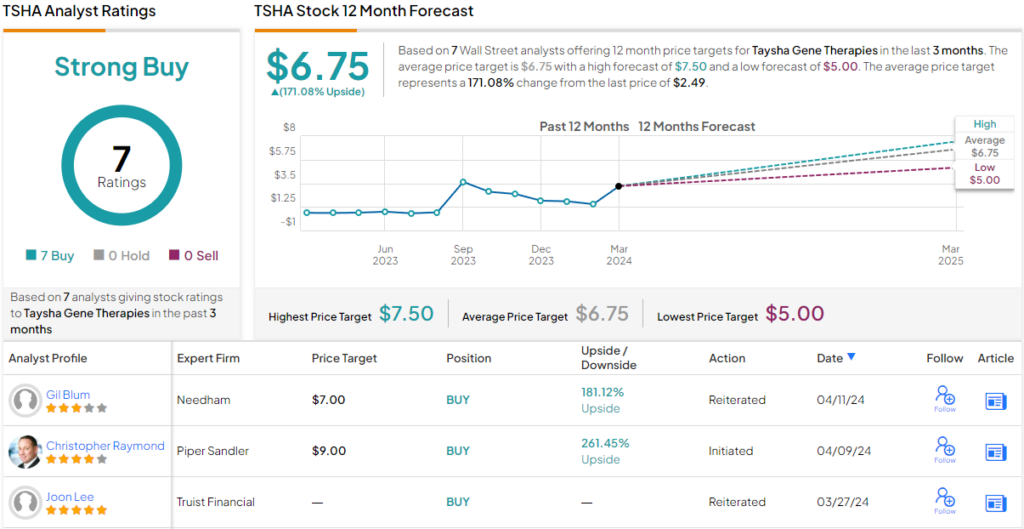

All of this adds up to an Overweight (i.e. Buy) rating from the analyst, and a $9 price target that implies a gain of ~261% in the one-year horizon. (To watch Raymond’s track record, click here)

What does the rest of the Street have to say? 7 Buys and no Holds or Sells add up to a Strong Buy consensus rating. The shares are trading for $2.49, and their $6.75 average price target indicates the stock may gain 171% by this time next year. (See TSHA stock forecast)

To find good ideas for penny stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.