In the classic tune by Kenny Rogers, ‘The Gambler,’ he sang, ‘Every hand’s a winner and every hand’s a loser…’ These words hold valuable wisdom that should resonate with every investor. Regardless of your chosen investment strategy, achieving success in the stock market ultimately hinges on mastering the art of balancing risk and reward.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Few segments of the stock market offer a higher potential return for the risk involved than the penny stocks, those equities priced at $5 or less. These are stocks with a truly rock-bottom cost of entry.

This low entry cost carries the potential for substantial gains, as even a modest increase in share price can translate into a significant percentage return. When it comes to penny stocks, it is not unheard of to find upside potentials of 300%, 400%, or even better. Of course, the flip-side is also true; with the high reward comes increased risk.

Given the nature of these investments, Wall Street analysts recommend doing some due diligence before pulling the trigger, noting that not all penny stocks are bound for greatness.

With this in mind, our focus turned to two penny stocks that have received a thumbs-up from Baird analysts. After running the tickers through TipRanks’ database, we found that both have been cheered by the rest of the Street as well, as they boast a ‘Strong Buy’ analyst consensus. Not to mention, there is substantial upside potential on the table – we’re talking about over 500% here.

Leap Therapeutics (LPTX)

We’ll start with Leap Therapeutics, a clinical-stage biopharma company focused on developing new treatments for a variety of cancers. The company is working in the field of immune-oncology to create drug candidates based on monoclonal antibodies.

Leap’s leading candidate, DKN-01, is a humanized monoclonal antibody designed to fight esophagogastric, gynecologic, and colorectal cancers by targeting the DKK1 protein. FL-301, Leap’s second candidate, is an anti-CLDN18.2 antibody and is under research as a treatment for gastric and pancreatic cancers. The company has two additional drug candidates in preclinical stages of development.

In the research clinic, Leap’s leading candidate is currently undergoing three separate trials. The most advanced of these, the DisTinGuish study, is a Phase 2 trial of DKN-01 against gastric cancers. In recently released data on Part A of the study, covering the long-term follow-up for first-line patients, Leap showed that the overall response rate was 73% in the modified intent-to-treat population. The company has also announced positive initial results from Part A of the Phase 2 DeFianCe study, focusing on DKN-01 in the treatment of colorectal cancer. Based on the Part A results, the DeFianCe study will be expanded into a 130-patient randomized control trial for Part B, expected to start enrolling participants in the coming year.

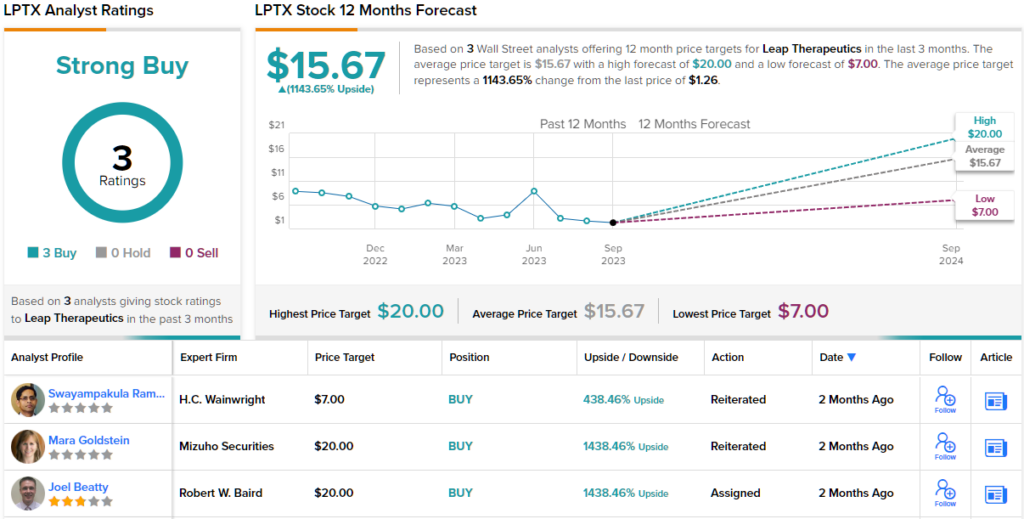

Based on the potential of DKN-01, and the company’s $1.26 share price, Baird analyst Joel Beatty thinks that now is the time to get in on the action.

“We view LPTX as a promising small-cap targeted oncology biotech company… Enrollment continues to be strong in the 160-patient randomized-controlled Part C of the DisTinGuish study in gastric cancer, which Leap expects to complete enrollment in 4Q23. This sets up initial ORR data from this study coming around YE23/1Q24. We view this as the most important catalyst for the stock. We anticipate the stock would trade several times higher if this trial is a clear success…”

Looking ahead to potential expansions of Leap’s program, Beatty points out that DKN-01 may have broader applications beyond its current clinical trial targets. He writes, “We believe credit for DKN-01 in additional cancers beyond gastric/GEJ is missing from the stock price. The strong and consistent ph2a data in gastric/GEJ cancer suggests to us that there’s a good probability that DKN-01 could provide a benefit in other cancers beyond gastric with high DKK1. Potential settings with some early supportive data include endometrial, colorectal, lung, and prostate.”

To this end, Beatty rates LPTX a Buy along with a $20 price target. This puts the upside potential at a massive 1,438%. (To watch Beatty’s track record, click here)

Turning now to the rest of the Street, 3 Buys and no Holds or Sells have been published in the last three months. Therefore, LPTX has a Strong Buy consensus rating. With the average price target clocking in at $15.67, the upside potential lands at 1,143%. (See LPTX stock forecast)

Cellectis SA (CLLS)

The next penny stock we’ll look at is Cellectis, an immunotherapy biopharmaceutical company working on new cancer treatments; specifically, Cellectis’ work is focused on chimeric antigen receptor (CAR) T cell technology, a biotech approach that fights cancers through enlisting the patient’s own immune system to inhibit growing tumors.

Cellectis is using a proprietary gene editing platform, TALEN, to develop a line of anti-cancer therapies that can be used ‘off the shelf,’ reducing the time needed to start effective therapies for patients. The company has created a line of in-house CAR T cell drugs, the UCART line, as allogenic products, designed to target multiple indications. This is an important advantage for Cellectis’ product line, as existing CAR T drugs are typically customized for each patient.

The line of in-house UCART products includes three drug candidates in the clinical trial stages – UCART22, a potential treatment for acute lymphoblastic leukemia; UCART123, a potential treatment for acute myeloid leukemia; and UCART20x22, targeting non-Hodgkin lymphoma.

Cellectis has recently released positive data derived from the BALLI-01 trial, a Phase 1/2a clinical study of UCART22. The next data set is scheduled for release later this year. Turning to the AMELI-01 trial, the Phase 1 dose escalation study of UCART123, Cellectis has released positive primary data and is currently enrolling patients for further studies.

From an investor’s perspective, perhaps the most exciting of Cellectis’ clinical studies is the NATHALI-01 trial, the Phase 1/2a clinical trial of UCART20x22 in the treatment of non-Hodgkin lymphoma. This is a target condition with a large addressable market and high profit potential for any company that can develop a new, effective treatment. Cellectis’ candidate, UCART20x22, is the first dual allogenic CAR T product designed to target both CD20 and CD22 in the treatment for NHL. The study is ongoing and offers a near-term catalyst as first-in-human data is expected to be released before the end of this year.

The potential success of UCART20x22 is a main feature that caught the attention of Baird analyst Jack Allen, who writes, “We anticipate the data surrounding UCART20x22 will gain the majority of investor attention, as investors are well aware of the commercial opportunity for CAR-T in NHL, which is currently ~$2B annually based on the sales of the approved autologous products.”

“Given the success of other CAR-Ts in this space, we believe Cellectis is taking a thoughtful approach to the development of UCART20x22, focusing on CD19 experienced patients (inclusive of antibody, bispecific, and CAR-T) and note recent data from Adicet’s CD20-targeted gamma delta, ADI-001, in a similar patient population lead us to be optimistic that Cellectis will see a meaningful rate of response to their therapy (while Cellectis’ utilization of T cells also leads us to be optimistic about the potential durability as well), which lead us to be positive on shares ahead of this dataset,” the analyst added.

In line with his optimistic approach, Allen gives CLLS shares an Outperform (i.e. Buy) rating and his $10 price target suggests a robust 566% potential upside for the coming year. (To watch Allen’s track record, click here)

Overall, the Strong Buy consensus rating on Cellectis is based on 5 analyst reviews set in recent months, including 4 Buys and 1 Hold. The shares are priced at $1.50, with an average target price of $8.5 suggesting ~466% upside potential heading out to the one year horizon. (See CLLS stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.