Our modern world has a voracious appetite for metals, and smart investors can leverage that for profits. The list of metals is extensive, and ranges from lesser-known rare elements such as scandium, yttrium, and gadolinium to the vital component of every battery in every digital device, lithium. Lithium has been growing in value as laptops, ipads, and smartphones, with lithium-ion batteries, have proliferated, but in recent years the expansion of electric vehicles – and their far larger battery packs – has pushed the price of lithium sky-high.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

From an investors perspective, this opens up several avenues for opportunity, particularly in lithium mining and lithium processing.

In a report from B. Riley Securities, analyst Matthew Key lays out the current status and path forward for the lithium industry: “Lithium has arguably been the best-performing commodity since the start of 2021, with current pricing for carbonate and hydroxide at $74,000/Mt and $80,500/Mt, respectively, primarily from battery demand for electric vehicles. Overall, we believe the strong outlook for EV sales will support robust pricing over the near term…”

Key’s description shows why now is the right time for investors to consider lithium, as a portfolio option. So let’s take a look at two lithium stocks that the analyst has given Buy ratings along with double-digit upside potential – on the order of 40% or more. In fact, Key’s view is no outlier. Running the tickers through TipRanks’ database, we found out that each boasts a “Strong Buy” consensus rating from the broader analyst community.

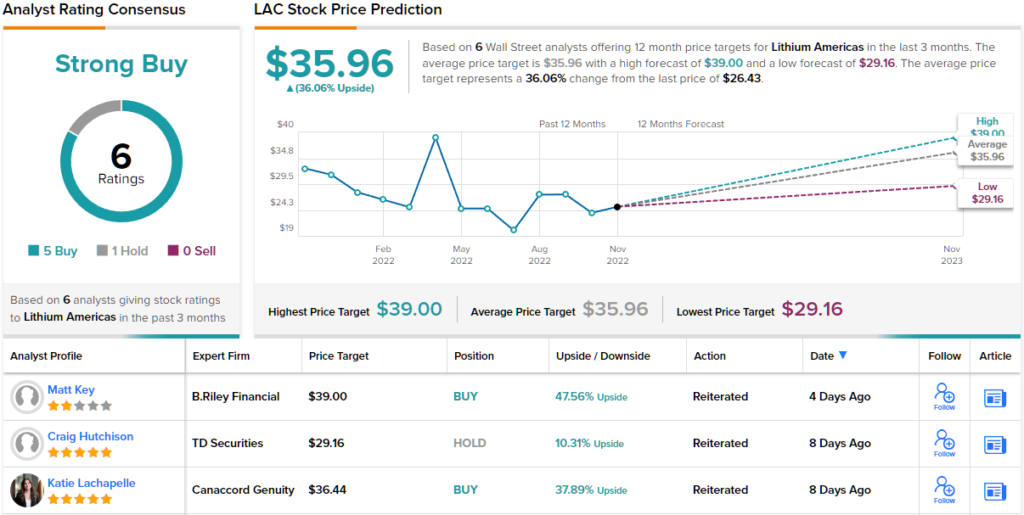

Lithium Americas (LAC)

First up, Lithium Americas, is developing two major lithium mining and processing projects, the Cauchari-Olaroz mine in northern Argentina and the Thacker Pass mine in Nevada. Thacker Pass is potentially North America’s best lithium mine, with the largest known lithium reserves in the US. Between the two projects, Lithium Americas expects to generate approximately 100,000 tons of usable lithium annually.

For now, the company is still in development stages, moving both projects toward completion and the commencement of production. In its 3Q22 report, released on October 27, the company reported continued progress on the Cauchari-Olaroz, with an update on the production ramp-up schedule expected before the end of this year.

Turning to Thacker Pass, Lithium Americas reported that, by September of this year, it had sent 100 tons of ore from the mine for the production of product samples that can be shown to potential customers and partners. The feasibility study, required before the mine can open, is scheduled for completion in 1Q23.

While Lithium Americas is still pre-revenue, it is in a sound financial position. As of September 30, the company had on hand $392 million in cash and other liquid assets, along with $75 million in available credit.

Checking in with B. Riley’s Key, we find that he is bullish on Lithium Americas, saying of the stock: “LAC continues to be one of our favorite names in our coverage group, and we believe the completion of Cauchari in early 2023 will serve as a major catalyst for the stock. Importantly, the increase in near-term carbonate pricing benefited the earnings potential of Cauchari considerably, and we are now estimating $332M in EBITDA for 2023E and $385M for 2024E.”

It should be unsurprising, then, that Key rates LAC a Buy. Not to mention his $41 price target puts the upside potential at ~48%. (To watch Key’s track record, click here)

It’s clear from the consensus rating, a Strong Buy supported by 5 Buy ratings out of 6 analyst reviews, that Wall Street is bullish on this lithium company. As for upside, the shares are trading at $26.43 and their $35.96 average price target suggests a gain of 36% in the coming year. (See LAC stock forecast at TipRanks)

Piedmont Lithium (PLL)

The next stock we’ll look at is Piedmont Lithium, a lithium mining and processing firm which, like LAC above, is still in the development process. The company’s goal is to turn the US into a major player in the global lithium supply chain. It’s a realistic goal; the US has approximately 17% of the world’s proven lithium reserves, and with current US production averaging only 2% of current supply, there is plenty of room for expansion here.

Piedmont is working to bring mining assets in North Carolina online, and its main activities are at the Carolina Tin Spodumene belt, not far from Charlotte. The company holds 1,100 acres in that region, and is on track to begin construction activities in 2024. Spodumene concentrate production is scheduled to begin in 2026, with a goal of 30,000 tons annually at full production capacity.

The company’s other major project is located in Tennessee, where the company has selected a site for a 30,000 ton capacity lithium hydroxide plant, with production targeted for 2025. The company’s Tennessee lithium project has recently been selected by the US government to receive a $141.7 million grant from the US Department of Energy, as part of the Biden Administration’s recent infrastructure law.

Outside of the US, Piedmont has partnerships with lithium mining projects in Quebec, at the North American Lithium (NAL) project in Val d’Or, and in Ghana, in the Ewoyaa project. Piedmont invested in these projects in 2021, and expects to benefit from 168,000 tons annual production of spodumene concentrate in Quebec, starting in 2023, and from 30.1 million tons of known Li2O reserves at the Ewoyaa mine. While the Quebec and Ghana projects are based on smaller reserves than Piedmont has in the Carolina, they are expected to go online at an earlier date.

Analyst Matthew Key recently bumped up his price target on Piedmont Lithium’s stock, and wrote of his decision: “Our PT for Piedmont increased for two primary reasons. First, the increase in long-term hydroxide prices from $16,000/Mt to $18,000/Mt was highly accretive to Piedmont’s hydroxide projects in Carolina and Tennessee. In total, the adjustment added roughly $338M in NAV value for both assets. In addition, the increase in long-term spodumene prices from $900/Mt to $1,200/Mt also benefited the NAV of the company’s two spodumene assets.”

To this end, Key rates the shares a Buy, and his new price target, set at $108, indicates room for ~75% upside potential in the shares.

Overall, there are 4 analyst reviews on this pre-production lithium company, and all are positive, making the Strong Buy consensus rating unanimous. The shares are priced at $61.56 and their $108.75 average price target suggests a gain of ~77% in the next 12 months. (See PLL stock forecast at TipRanks)

To find good ideas for lithium stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.