The energy sector has been riding high this year, with the S&P 500 Energy index up a whopping 65%. So the question for investors is, does the sector have more room to run? According to Wall Street pros, the answer to that is ‘yes.’

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Selling an absolutely necessary product, energy companies are widely seen as hedges against inflation, frequently offering a combination of corporate profits and shareholder dividends. In the US, the price of crude oil has risen 15% so far this year, and the government estimates that it will continue going up, from its current $86 per barrel to $95 per barrel in the first half of next year.

Bearing this in mind, we used TipRanks’ database to pinpoint two energy stocks that are showing clear opportunities for investors. These are Strong Buy tickers, according to the analyst community, and while both have already achieved serious growth this year, they are primed to keep climbing higher. Let’s take a closer look.

Cheniere Energy, Inc. (LNG)

The first energy stock on our list is Cheniere Energy, a Houston-based firm specializing in the liquefication of natural gas prior to export. The company controls a $38 billion network of pipelines and natural gas liquification facilities, including major export terminals at Corpus Christi, Texas and Sabine Pass, Louisiana. The export terminals include 9 liquefaction units between them, and are capable of passing through a total of 45 million tons annually of liquified natural gas for export. Cheniere is the largest natural gas liquification company operating in the US, and one of the largest in the world.

Along with a leading position in the US gas export market, Cheniere has also been showing steady gains in revenues since the third quarter of 2020. The company’s most recent report, from 3Q22, showed $8.85 billion at the top line, up an impressive 177% year-over-year. Cheniere has found support for its revenues from the rising price of natural gas on the world markets, along with increased exports to Europe in recent weeks. Overall volume of gas exported in 3Q22 was 559 trillion Btu, compared to 500 trillion one year earlier, a gain of 12%.

The company’s net income, however, came in at a loss, of $2.38 billion. This was a sharp turnaround from recent profits, and was attributed to derivative losses of approximately $2.2 billion, and settlements of $6 billion.

Nonetheless, Cheniere shares are up 67% this year, far outperforming the overall markets.

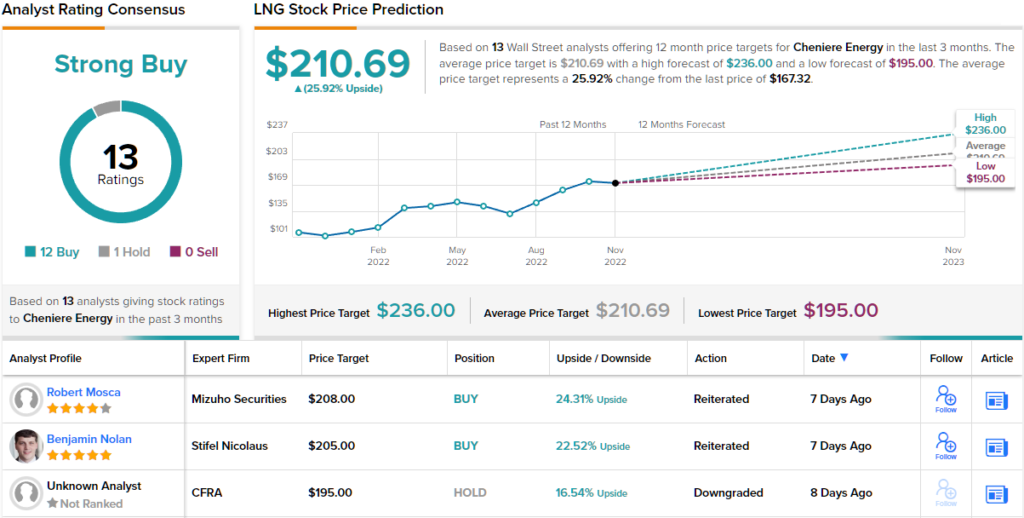

Cheniere has scored fans within the analyst community. Among them is Jefferies analyst Lloyd Byrne, who rates the stock a Buy, while his $210 price target implies a one-year upside of 25%. (To watch Byrne’s track record, click here)

Backing his stance, the analyst writes: “We like Cheniere because its first mover advantages give it a leg up in contracting and self-funding growth projects, which should help sustain its position as the largest US liquefaction player generating strong returns on capital and consistent cash flows. Helped by this virtuous cycle, we believe Cheniere will be well positioned to return cash to shareholders through spending and commodity cycles. Recent guidance raise and capital allocation update reinforces our view.”

The Street, generally, is sanguine on Cheniere stock, as shown by the unanimous Strong Buy consensus rating based on 13 positive analyst reviews. The stock is trading for $167.32 and its $210.69 average price target suggests that a gain of ~26% lies ahead. (See Cheniere stock forecast on TipRanks)

Schlumberger Limited (SLB)

From natural gas export we’ll turn to oilfield services, another essential niche. The oil exploration companies would not be able to get their product out of the ground if not for the services offered by Schlumberger and its peers. Schlumberger makes available to the drilling companies the necessary expertise in well completion, drilling, and other engineering tasks essential in oil production.

The oil industry, generally, has benefitted in recent quarters from increases in the price of crude on world markets, along with continued strong demand, and Schlumberger has had a part of that. The company’s revenues are solid, with the recent 3Q22 report showing a top line of $7.5 billion. This was up 28% from the year-ago quarter, and included a 26% y/y gain in international revenue and an even stronger 37% y/y jump in North American revenue.

The company reported a GAAP EPS of 63 cents per share, which was up 62% y/y. These earnings were accompanied by strong cash flows – cash from operations came in at $1.6 billion, and free cash flow was reported at $1.1 billion. The company also boasted current liquid assets of $3.6 billion. In short, Schlumberger is swimming in cash.

For investors, that’s important because cash funds the dividend, which was declared on October 20 at 17.5 cents per common share, for a January 12 payment. At the current declared rate, the dividend pays out 70 cents per year, and yields 1.32%. While the yield is low, Schlumberger does have a reliable history of keeping up the payments.

Schlumberger’s stock has gained an impressing 79% this year, outperforming the broader market by far.

Analyst Roger Read, in coverage of Schlumberger for Wells Fargo, sees the company is a strong position to continue its gains. He writes, “SLB posted positive EPS/EBITDA beats on impressive Well Construction and Production Systems performance supported by continued net pricing improvements. Increased activity in the offshore and international markets presents upside for strong int’l servicers in our view, which is why SLB remains our top pick in the sector.”

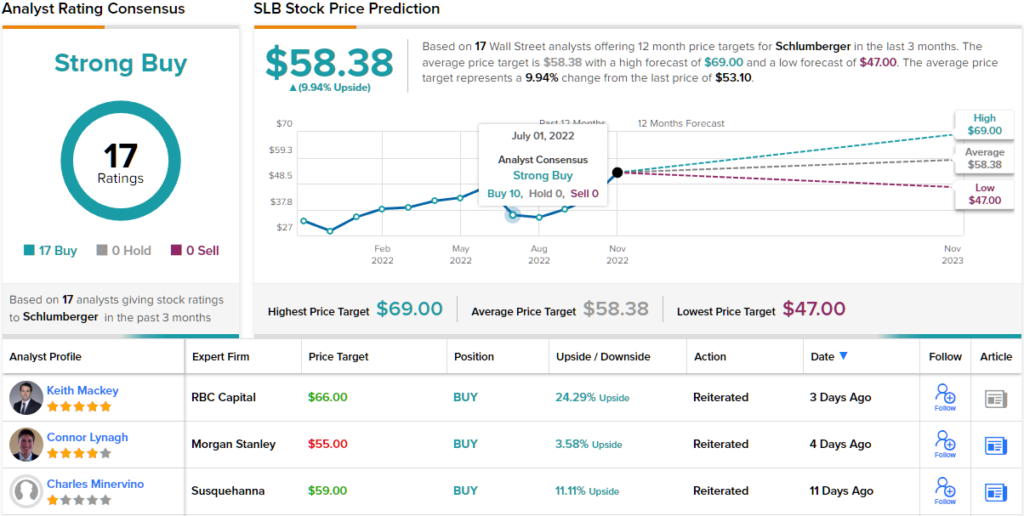

Read’s comments back up his Overweight (i.e. Buy) rating on these shares, and he sets a $69 price target that suggests a 30% upside in the next 12 months. (To watch Read’s track record, click here)

Overall, no fewer than 17 Wall Street analysts have chimed in on SLB shares, and they are unanimously positive, giving the stock its Strong Buy consensus rating. Schlumberger stock is priced at $53.10 and its $58.38 average target indicates ~10% one-year upside. (See SLB stock forecast on TipRanks)

To find good ideas for energy stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.