Market legend Warren Buffet likes to remind us, “Insurance will always be essential for both businesses and individuals.” It touches a basic truth in business: insurance exists to mitigate risk and protect financial resource, and both are vital in today’s world. The insurance industry has a reputation as stodgy and boring, but it’s also remarkably stable, meeting a true need.

It’s also an industry that presents a paradox – insurance companies don’t make their money by collecting premiums. The costs of business administration and claims payouts typically exceed the annuals premiums. But – between collecting those premiums and paying out claims, the company has a pool of money at its disposal, called the float, which can be used for profitable investments.

Between necessity and float, insurance stocks can offer investors both stability and profits, and that makes them always worth a second look. A recent study from the investment bank HSBC underscores this point, noting that the global insurance industry collected nearly $4 trillion in non-life insurance premiums during 2022.

The bank’s analyst Vikram Gandhi sums it up: “While the US non-life insurance market is not a typical growth industry, premium prices, especially for the US commercial lines, have been growing for nearly five years. We think this bodes well for the profitability of the segment over the next couple of years… Overall, we prefer commercial lines-focused names vs personal lines-heavy insurers. Our preference for commercial lines-geared stocks is supported by their much wider discount to the market versus four years ago.”

Gandhi goes on to point out two insurance stocks that have recently reached 52-week high levels, but still have room to run. We’ve delved into TipRanks’ database to see what makes them stand out.

American International Group (AIG)

The first stock on our short list today is American International Group, better known by its acronym AIG. With operations in more than 80 countries, over 26,000 people on the payrolls, and a market cap of $47 billion, the company is consistently ranked among the world’s largest insurance firms. According to recent data from Forbes, AIG has $463.77 billion in total assets, making it the 4th largest insurance company in the US, and the 11th largest on the global scene. The company generated total revenues of $55 billion in 2022.

AIG’s customers can choose from wide selections of insurance products, including policies in the property and casualty, accident and health, financial, life, and liability segments. The company also offers financial services such as retirement solutions, connected to the general line of its business – protecting assets through risk management and providing for customers’ future security.

AIG registered a 7.8% year-over-year increase in revenue in 2022, but the company started 2023 on rough footing. The stock saw sharp losses in February, after reporting lower than expected profits in the wake of severe winter weather and increased claims activity, and again in March, during the crisis in the regional banking sector. The stock bottomed out at the end of March and has had a solid run since then, posting a 43% gain.

The company has credited its recent gains to strong performance in both its underwriting and Commercial Lines businesses, particularly during 3Q23. The company reported a quarterly net income of $1.61 per diluted share, up 92% year-over-year and 13 cents per share better than had been expected. The gain in income was driven by $611 million in underwriting income, which was up an impressive 264% from the prior-year quarter.

Covering this stock for HSBC, analyst Gandhi notes that the company is emerging from the restructuring initiative that has engaged its attention over the past several years – and that its new self, leaner and more focused, shows plenty of potential going forward. Describing AIG’s situation, Gandhi writes, “With large part of restructuring complete, AIG’s liability risk profile stands much better now relative its own history as well as peers on many aspects. Separately, following the successful execution of its transformative program AIG 200, the group is focused on further expense savings. However, we think the market has yet to be fully convinced that the ‘new’ AIG is a much more conservative risk-taker and is set to become nimbler as it rapidly advances towards separating CorebridgeFinancial (CBRG) – its L&R business. Our 2023-25 estimates are marginally ahead of the Street.”

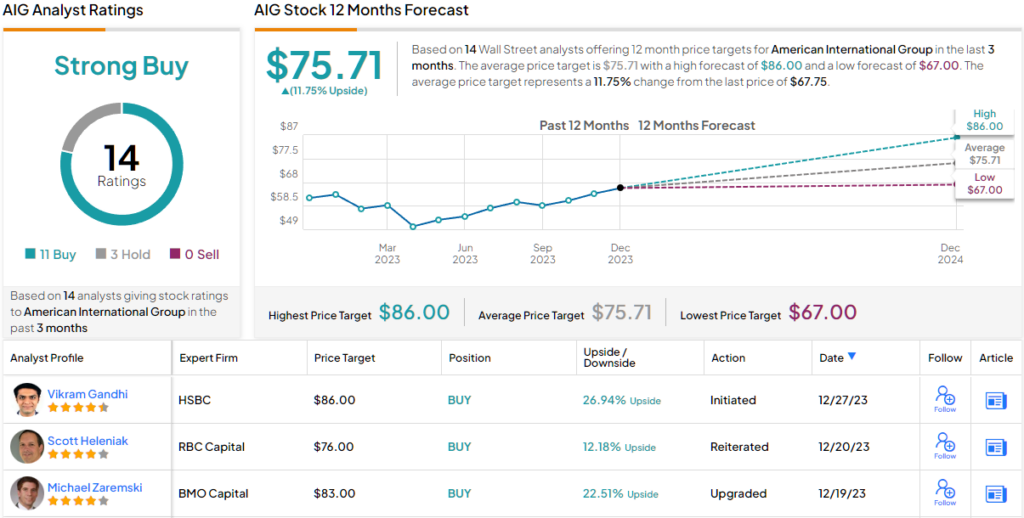

The analyst goes on to initiate his coverage of these shares as a Buy, with an $86 price target that points toward a one-year gain of 27%. (To watch Gandhi’s track record, click here)

Overall, the Street rates AIG as a Strong Buy, based on 14 recent analyst reviews that include 11 Buys to 3 Holds. But – the $75.71 average price target suggests ~12% increase from the current share price of $67.75, significantly lower than the HSBC view. (See AIG stock forecast)

Chubb (CB)

Next up on our insurance list today is Chubb, another giant of the global insurance industry. Chubb is huge by any measure – the company has a market cap of $91.5 billion, underwrote $4.6 billion in property & casualty policies in 2022, and listed $222.74 billion in total assets at the end of 3Q23. Chubb is active in 54 countries, providing services from property and casualty insurance, personal accident and supplemental health policies, life insurance, and reinsurance policies.

The core of Chubb’s business is underwriting, the assessment, assumption, and management of risk, to protect customers’ assets. The company has nearly 40 years’ experience in the field, and can build on that to offer policy coverage and services, for businesses, individuals, and families, that rate among the industry’s best.

Chubb’s share performance through 2023 has been something of a roller coaster. Like AIG, the company’s stock fell badly in March, during that month’s banking crisis, and again like AIG, Chubb’s shares have been on an upward trend since them. But CB has taken a decidedly volatile upward path this year, with plenty of ups and downs as it regained the ground lost in March.

When we get down to the brass tacks, however, we find that Chubb benefits from the same factors that have always supported the insurance industry: everyone needs to manage risk and protect assets, and that means buying insurance. In the last reported quarter, 3Q23, Chubb reported a solid non-GAAP EPS of $4.95 – a result that was 53 cents per share better than had been anticipated.

That income rested on solid year-over-year gains in the company’s property and casualty business. Chubb reported an 8.4% increase in P&C net premiums written for Q3, and a 12.3% increase in its global P&C business. The latter included a 10.3% increase in commercial insurance and a 17.6% increase in consumer insurance. Overall, the company reported consolidated net premiums written for Q3 of $13.1 billion, a total that was up 9.1% from the prior year.

Turning again to analyst Vikram Gandhi, we find him upbeat on Chubb’s solid position in the industry, and describing the stock as offering a quality option for investors. Gandhi writes of the company, “Chubb operates with best-in-class metrics on several fronts: best expense ratio (25-26% vs 28-32% for peers), highest IBNR ratio for LT lines (>75% vs 65-70% for peers), and lowest financial leverage (19-20% vs 21-28% for peers). And while we see the group as potentially more exposed to social inflation risks, we note that it also offers the highest IBNR ratio on LT lines in its peer group. Overall, given its quality, we think the stock deserves to trade at a premium vs peers. Our 2023-25 estimates are marginally behind consensus.”

Gandhi goes on to start his coverage of this stock with a Buy rating, while setting a $263 price target to suggest an upside potential of 16% on the one-year horizon. (To watch Gandhi’s track record, click here)

This stock gets a Moderate Buy consensus rating, coming from 14 recent reviews that break down to 9 Buys and 5 Holds. The stock’s $226 current trading price and $245.54 average target price together imply ~9% increase in share value by the end of 2024. (See Chubb stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.