Everyone is always on the lookout for the best possible deal – that applies to all walks of life, be it at the supermarket, the top echelons of sport, or the investing world. That said, finding the best deal in the stock market could be a complex endeavor because, while it is probably easy to find equities priced in a low range, there might be a good reason why said names are going for cheap.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Therefore, a little help in discerning which stocks are just not worth the time of day and which ones are truly at discount levels would be beneficial. In this regard, guidance from Wall Street’s equity experts, such as those employed at established financial institutions like Wells Fargo, can prove invaluable.

Recently, the firm’s analysts have homed in on a pair of stocks they believe are ripe for the picking right now, labeling them both as “too cheap” at current levels. We ran these tickers through the TipRanks database to find out what their Wall Street colleagues make of their chances.

PVH Corp. (PVH)

Let’s start in the global fashion industry and take a look at the parent company of some of the world’s most famous apparel brands.

PVH is a fashion market leader boasting a portfolio of iconic names such as Calvin Klein and Tommy Hilfiger, in addition to others on its roster. The New York City-based firm operates through various distribution channels, including retail stores, e-commerce platforms, and wholesale partnerships, with around 27,000 associates active in over 40 countries.

This global strutting business dialed in a strong first quarter report with beats both on the top-and bottom-line. Revenue climbed by 2% year-over-year to $2.16 billion, edging ahead of the forecast by $30 million. EPS of $2.14 easily trumped the $1.95 consensus estimate.

However, the shares fell consequently and that was down to a disappointing outlook. The company stuck to its FY 2023 guide, projecting revenue will rise by 3% to 4% vs. 2022, but that, at the mid-point, was below consensus, which called for a year-over-year increase of 3.76%. The outlook for Q2 was another letdown for investors, with EPS expected to hit $1.70, some distance below the Street’s expectation of $2.26.

Investors might have been disappointed with the forecast but that is no issue for Wells Fargo analyst Ike Boruchow, who calls PVH a “rare name that has managed the tough macro well.” Moreover, Boruchow thinks investors should take advantage of an enticing entry point.

“Momentum is evident, multiple remains too cheap. PVH is bucking the trend – with international growth and NA recovery driving results. Better demand trends and improving margins are an outlier today, and it’s clear PVH’s strategies around supply chain, brand elevation and distribution are gaining steam. We remain very bullish on this idiosyncratic turnaround story,” Boruchow opined.

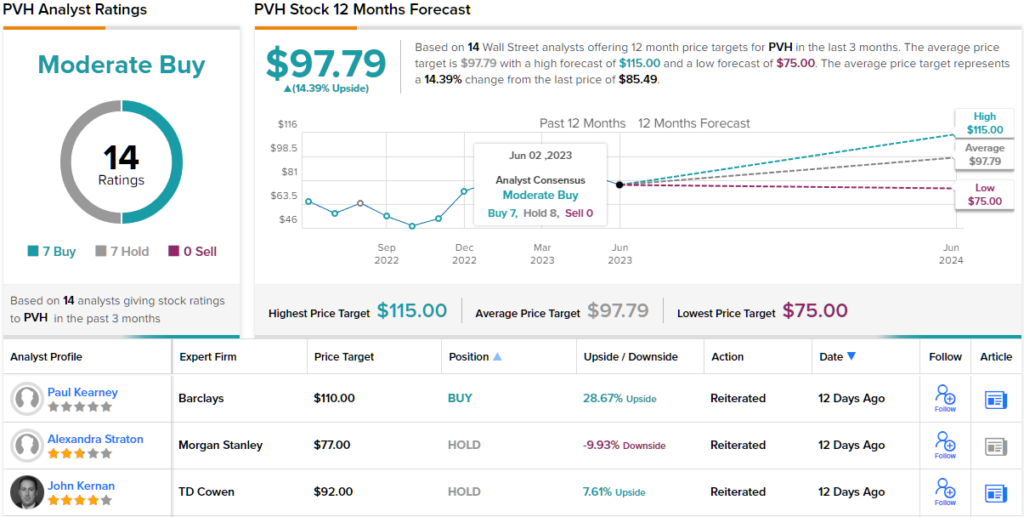

These comments form the basis for Boruchow’s Overweight (i.e., Buy) rating on PVH, while his $110 price target suggests the shares have room for 12-month growth of 29%. (To watch Boruchow’s track record, click here)

Elsewhere on Wall Street, the stock claims an additional 6 Buys and 7 Holds, all coalescing to a Moderate Buy consensus rating. The average target currently stands at $97.79, indicating the shares will be changing hands for a 14% premium a year from now. (See PVH stock forecast)

BJ’s Wholesale Club Holding (BJ)

The next stock Wells Fargo thinks is on discount is fittingly BJ’s Wholesale Club Holdings, a prominent American warehouse club retailer that operates a chain of membership-based stores. Since it was founded in 1984, BJ’s Wholesale Club has established itself as a significant player in the industry, offering consumers and businesses a wide range of products, including groceries, electronics, furniture, appliances, and more, at discounted prices. As a membership-based retailer, BJ’s offers exclusive benefits to its customers, such as access to a variety of services, discounts, and personalized offers.

The company operates 237 warehouse clubs across 18 states, primarily located on the east coast. In addition to its physical stores, BJ’s has expanded its digital presence, offering online shopping, delivery services, and the requisite mobile app.

While its business model is one suited for tough economic times, the company’s most recent quarterly readout was not an all-out success. Revenue increased by 4.9% year-over-year to reach $4.72 billion but fell $90 million shy of the analysts’ forecast. That said, gross profit rose from $790.6 million to $880 million and helped the retailer dial in adj. EPS of $0.85, thereby meeting Street expectations.

Shares have mostly been on the backfoot since the report’s release, a development Wells Fargo analsyt Edward Kelly puts down to “growing concerns about forward momentum.”

Those issues are understandable, says Kelly, although the analyst believes the stock is simply “too cheap.”

“BJ has the same issue as most peers… industry fundamentals are just slowing,” the 5-star analyst went on to say. “Consumer weakness is pressuring gen merch, while the historic pricing cycle in grocery is ending. This clearly creates momentum issues for defensive staples retail names. That said, BJ should be a share-gaining model, has a good self-help story, and trades at a compelling multiple. We remain Overweight as this big picture narrative should eventually win out.”

Along with that Overweight (i.e. Buy) rating, Kelly’s $83 price target implies shares will appreciate by 33% over the course of the year. (To watch Kelly’s track record, click here)

Most analysts agree with that stance. Of the 14 other reviews made during the past 3 months, 9 join Kelly in the bull-camp, 4 remain on the sidelines while one implores to Sell, all adding up to a Moderate Buy consensus rating. The forecast calls for one-year gains of ~28%, considering the average target stands at $78.87. (See BJ stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.