Bad is good and good is bad. No, that’s not an extract from Orwell’s 1984, but rather the stock market’s view of the jobs market at the end of 2022.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Friday’s better-than-expected jobs numbers put a spanner in the works for investors hoping the Fed will start easing its aggressive monetary stance when it convenes midway through the month to decide on its course of action. A strong jobs market is the opposite of what the Fed is looking for as it continues in its efforts to tame inflation. Therefore, the figures have sown renewed fears amongst investors worn out by 2022’s bear that another 75-basis-point rate hike – rather than a more moderate 50-basis-point increase – is in the cards.

It remains to been seen what the Fed’s decision will be, but in any case, 2022’s negative market action has resulted in many stocks already dropping to some very enticing levels. In fact, some Street analysts believe a couple of stocks are down to a level that makes them just too cheap to ignore right now. We ran these Buy-rated tickers through the TipRanks database to get a more comprehensive overview of their prospects. Let’s check the details.

Opera, Ltd. (OPRA)

We’ll start with a small-cap software firm that has built a reputation for quality. Opera got its start more than 25 years ago, bringing the best in developers, coders, researchers and marketers to the early stages of the online world. Today, the company is known for its array of top-end online products, including game making software, a wide range of mobile social apps from chat to news feeds, VPN tech, online entertainment streaming, and innovative browsers for both desktop and mobile.

All of this has brought Opera upwards of 321 million active monthly users, in a customer base that spans the globe. Opera is always looking for ways to add value to its products, and last month announced that its browser was the first to include TikTok as a built-in sidebar feature.

Opera’s recent report on Q3 financial results showed a strong year-over-year gain in revenue, from $66.6 million to $85.3 million, or an increase of 28%. Net income fell, however, from $23.5 million to $9.4 million. By EPS, the adjusted income drop was 26 cents to 10 cents per diluted share. While net income fell in the quarter, Opera felt comfortable enough to raise its full-year revenue guidance for 2022, from $316 million to $324.5 million at the midpoints; achieving this will result in a 29% y/y revenue gain.

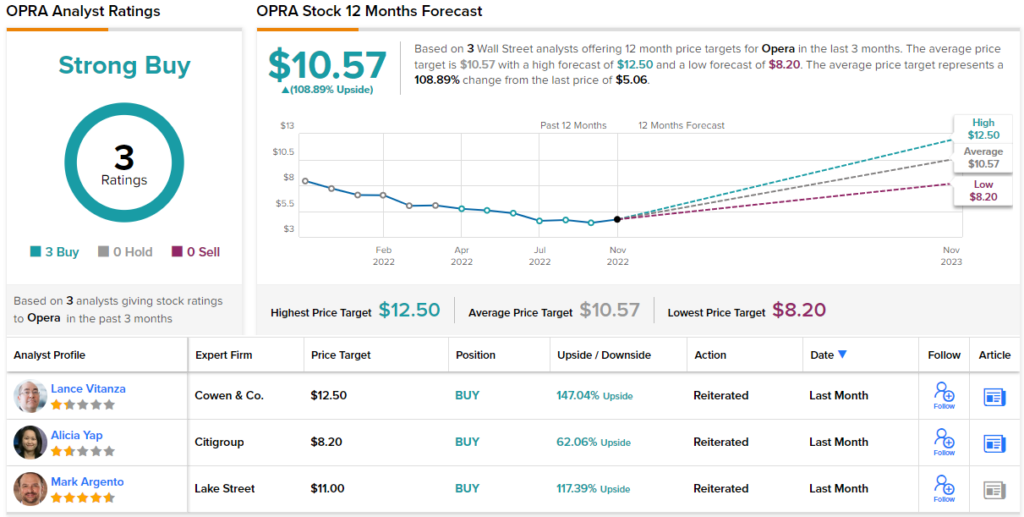

Despite the overall sound Q3 results, shares in Opera are down by 28% so far this year and Lake Street Capital Mark Argento smells opportunity. In short, the analyst believes that OPRA shares are crazy-cheap, and doesn’t shy from saying so: “While many stocks are cheap, this one takes the cake. To say that shares are dirt cheap is an understatement…. Given the unique nature of the company, its geography, and its business, investors have overlooked a business that is growing top line organically and has significant market penetration opportunities in developed counties. Even taking an ultra-conservative approach to an enterprise value calculation, OPRA is still trading at a double-digit free cash flow yield…. While we understand shares should trade at a discount to some of their larger internet/media peers, 1x EBITDA is absurd and is not sustainable.”

Argento, of course, puts a Buy rating on OPRA, and his price target, set at $11, implies a robust upside potential of 117% for the next 12 months. (To watch Argento’s track record, click here)

While there are only 3 recent analyst reviews on Opera’s stock, they all agree that it’s one to buy – giving the shares a unanimous Strong Buy consensus rating. The stock is priced at $5.06 and has an average price target of $10.57, suggesting a one-year gain of 109%. (See OPRA stock forecast at TipRanks.)

Yeti Holdings (YETI)

Next up, Texas-based Yeti. The company got its start in 2006, producing, marketing, and distributing a line of high-quality outdoor goods and gear, including its lines of insulated bags, coolers, and cups, as well as outdoor apparel for winter weather, and even rugged bowls and beds for dogs on the trail. Yeti has expanded from its relatively modest beginning into a large firm with a market cap of $3.8 billion and a devoted following among campers, fishers, and hunters. The company’s products are available through its network of brick-and-mortar stores, as well as through its online e-commerce site.

YETI shares have lost 43% year-to-date, a loss that is significantly deeper than the 14.5% decline in the S&P 500 over the same time. However, the stock has been paring back the losses recently, boosted by a strong Q3 showing.

Yeti posted a 20% y/y increase in sales from 3Q21 to 3Q22, from $362.6 million to $433.6 million. The company’s direct to consumer (DTC) sales were up 15% y/y, and made up 52% of the total. Yeti’s wholesale channel sales were up 25% y/y, to $206.2 million. During 3Q22, the company saw strong sales in Coolers & Equipment, especially the soft and hard coolers, and bags. The Coolers & Equipment segment was up 25% y/y, from $149 million to $185.7 million.

The top-line figure beat Street expectations, and likewise on the bottom-line; the company delivered adj. EPS of $0.63, edging ahead of the $0.59 forecast.

Brian McNamara chimes in from Canaccord Genuity, and he likes what he sees here; the company’s solid product line and large total addressable market lead him to describe this firm as “the ‘Nike’ of innovative outdoor products.”

Assessing the company’s prospects, McNamara said, “We believe this is a long-term growth story of a brand that is still underpenetrated in many parts of the U.S., while a nascent international business should be a disproportionate contributor of growth moving forward…. we believe market expectations are overly conservative…. we find the de-rating over the last year overdone and would encourage investors to use the underperformance as an opportunity to purchase this iconic global lifestyle brand at a discount.”

McNamara’s comments back up his Buy rating on the stock, and his $58 price target indicates potential for 23% upside on the one-year time frame. (To watch McNamara’s track record, click here)

The Moderate Buy consensus rating on YETI is based on 12 recent Wall Street reviews, which include 8 Buys and 4 Holds. The stock is selling for $46.99 and its $54.09 average price target suggests a gain of 15% for the next year. (See YETI stock forecast at TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.