The stock market had a good day today. The S&P has gained 1.63% and moderated its year-to-date losses to 19%. That rally has pushed the index up just out of bear territory.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Despite these gains, at least one major bear believes that the index hasn’t bottomed out yet. Mike Wilson, Morgan Stanley’s chief US equity strategist, sees more room for the index to fall, and predicts that the S&P will hit its low point somewhere between 3,000 and 3,200 – a drop that would mean another 20% loss for stocks. As for when, Wilson says, “We don’t know if it’s going to be this quarter or next quarter, but it’s probably some time in that timeframe.”

At the same time, Wilson won’t tell investors to abandon stocks. Morgan Stanley is taking a dual approach to equities, buying into companies that are still bringing in operating profits and cash flows despite a turbulent environment. “You shouldn’t abandon stocks,” he says, “there’s plenty of individual names that probably are extremely attractive.”

In these market conditions, two ‘extremely attractive’ attributes are share outperformance plus a high-yield dividend. With this in mind, we’ve used the TipRanks database to find two dividend stocks that are offering high yields of about 8%, and even better, both significantly outperformed the market this year — highlighting their defensive strength in the current volatile environment.

Coterra Energy (CTRA)

We’ll start with Coterra Energy, an exploration and production company in the North American oil and gas industry. Coterra has a profitable network of operations, in some of the continent’s richest, most productive oil and gas formations, including famed Marcellus shale of Pennsylvania and the Permian Basin of Texas, as well as Oklahoma’s Anadarko Basin. Coterra holds more than 593,000 net acres of land and land rights in these formations, and controls proven reserves in the range of 514 million barrels of oil equivalent.

This general position has, in the past year, generated solid profits and earnings for Coterra. The company’s last quarterly report, for 2Q22, showed a top line of $2.57 billion and a net income of $1.23 billion, along with $1.35 per share in adjusted earnings. The year-over-year gain in revenues and earnings was more than 5x, and was driven by quarterly production of 632,000 barrels of oil equivalent per day.

Along with increasing top and bottom lines, Coterra’s shares have been gaining all year. The stock is up an impressive 69% year-to-date, outperforming the broader markets by a wide margin.

In addition to strong financial results and share performance, Coterra also offers investors a commitment to capital return. The company has a share repurchase program, and bought back $303 million worth of stock in Q2; it also paid out a 65 cent dividend per common share. The dividend, with its $2.60 annualized value, yields 8.7%. With that yield, the dividend actually beats the current rate of inflation, ensuring a positive real rate of return for investors.

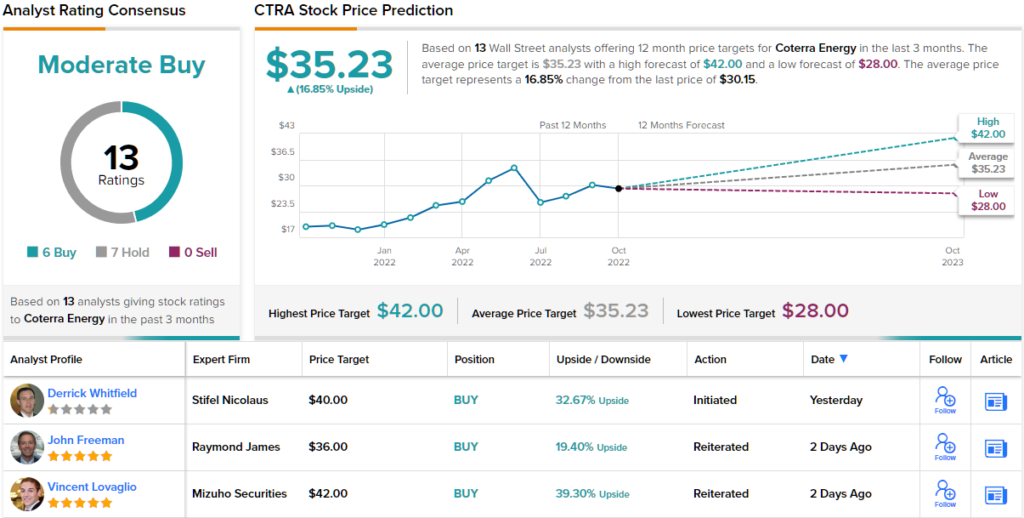

Analyst Derrick Whitfield, of Stifel, is bullish on Coterra, and lays out a clear case for buying into the company: “We are constructive on management and the company’s portfolio of resource projects, which were organically generated. CTRA offers investors a compelling combination of quality (asset and management) and value. Additionally, management remains committed to a +50% return to shareholders (excluding share buybacks) and has returned 69% and 80% of FCF through cash dividends and share repurchases over the last two quarters, respectively.”

Based on the above, Whitfield gives CTRA shares a Buy rating and a $40 price target that implies ~33% upside in the next 12 months. Based on the current dividend yield and the expected price appreciation, the stock has ~41% potential total return profile. (To watch Whitfield’s track record, click here)

Overall, Coterra has 13 recent analyst reviews, breaking down to 6 Buys and 7 Holds, for a Moderate Buy consensus rating. CTRA shares are trading for $30.15, and their $35.23 average price target indicates potential for ~17% upside on the one-year time frame. (See CTRA stock forecast on TipRanks)

Diamondback Energy (FANG)

For the second stock on our list, we’ll look at Diamondback, another of the hydrocarbon production firms working the Permian Basin in Texas. Last year, Diamondback’s average production reached 375,000 barrels of oil equivalent per day; in the second quarter of this year, that number has increased to more than 380,500 barrels of oil equivalent daily.

Rising production has clearly been a boon for Diamondback, which has seen its revenues and earnings both rise steadily over the past two years. In the most recent reported quarter, 2Q22, Diamondback’s revenues hit $2.77 billion and diluted EPS came in at an impressive $7.07 on $1.3 billion in adjusted net income. $1.3 billion was a good number for Diamondback, as it was also the free cash flow total for the quarter.

Solid earnings and cash flow supported Diamondback’s generous capital return – to the tune of $837 million in Q2, through both dividends and share purchases. We should note that Diamondback has increased its share repurchase authorization going forward to $4 billion, but for now we’ll focus on the dividend. The company makes both a base and variable payment to common stock shareholders; in the last declaration, for the dividend paid out in August, the base was set at 75 cents per share and was complemented by a $2.30 variable payment. It was the second quarter in a row with a $3.05 total dividend. Looking forward, the combination annualizes to $12.20 and gives 8% yield. With current inflation running at 8.2%, Diamondback’s dividend is high enough to provide real protection for investors.

In another interesting development for investors to note, Diamondback earlier this month closed a $1.6 billion acquisition in the Midland Basin, of FireBird Energy. The transaction included $775 million in cash, with the balance in stock, and brings a significant addition to Diamondback’s productive assets.

Year-to-date, shares in FANG are up ~50%. Yet, Stifel’s Derrick Whitfield sees the company in a strong position to continue its gains.

“We believe Diamondback is well-positioned to outperform in the current commodity environment based on its strong cash margins (81% vs. peer average of 77%) [and] defensive attributes (Minerals ownership, capital cost leadership, vertical integration, base dividend protected down to $35/bbl WTI)… In our view, the company’s cost leadership, balance sheet, minerals, and midstream ownership are a few of the reasons it is well-positioned to outperform as activity and inflationary pressures increase,” Whitfield opined.

To this end, Whitfield rates FANG a Buy, and gives the stock a $201 price target to suggest ~31% one-year upside potential. (To watch Whitfield’s track record, click here)

All in all, no fewer than 15 analysts have weighed in on FANG shares recently, with 13 Buys and 2 Holds giving them a Strong Buy consensus rating. The stock’s $153.36 trading price and $179.20 average price target imply a 16% gain for the next 12 months. (See FANG stock forecast on TipRanks)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.