We keep hearing about the ‘green’ economy, the shift from dirty energy sources to cleaner or renewable sources that will cause less environmental harm in the long run. The headlines usually go to wind or solar power, but those are hardly the only games in town. Investors can find plenty of opportunities in clean tech by adopting a broader view of the sector.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

That broader view should include energy storage, the key to success in moving our electric power needs away from fossil fuels. Meanwhile, batteries will become an ever more vital need, a fact that should direct our attention to lithium.

The two verticals within the clean tech stocks have already caught the eye of investment and research firm Raymond James. The company’s analyst Pavel Molchanov sees them as sound choices within clean tech, but reminds investors that research remains key to stock investing success. “As we always emphasize, clean tech is a stock picker’s market,” Molchanov said. “Within each vertical — even the narrow ones — we still have to focus on each individual company’s positioning (product mix, margin profile, industry partners, geographic footprint, etc.).”

That’s exactly what Molchanov has been doing and we can follow two of his latest picks using data from the TipRanks platform. These are Buy-rated shares with plenty of upside potential – and the Raymond James analyst says it’s time to pick up these clean tech stocks and build a diversified portfolio to take advantage of tomorrow’s tech economy. Let’s check the details.

Arcadium Lithium (ALTM)

Lithium stocks are probably the most basic way to buy into the battery sector. These are the companies engaged in the mining, production, and refining of lithium and lithium-based compounds and metals, materials that are absolutely essential to lithium-ion battery technology. While there are other battery technologies available, lithium-ion batteries are far and away the type most used in the most applications, especially in the electronics and automotive industries.

Arcadium is one of the world’s largest lithium producing companies. With its $4.7 billion market cap, and its active operations on a global scale, Arcadium boasts projects in resource exploitation, production, conversion, and mine-to-metal, all in lithium, and all aimed at producing the various forms of lithium required by modern industries. The company has ongoing projects in both North and South America, in East Asia, and in the UK. Arcadium’s North Carolina Bessemer City facility specializes in the production of high purity lithium metal, the only such production facility in the Western Hemisphere.

This company’s name and ticker are new to the New York Stock Exchange, even if the actual business is not. Arcadium, in its present form, was built from a merger-of-equals transaction completed in January of this year. Allkem and Livent, two major lithium companies, combined their business operations to create ‘a Leading Global Integrated Lithium Chemicals Producer.’

Arcadium has a set of premier lithium production and manufacturing sites located at key points in the global lithium supply chain. The company boasts some 2,600 employees and its formative components had $1.9 billion in combined total revenue in 2022, their last full year of separate operations before the merger process started. For 2023, the year during which the companies conducted merger operations, combined revenues came to $2 billion. Arcadium expects to realize between $60 million and $80 million in synergies and cost savings from the merger during 2024.

All of this caught Molchanov’s attention, but the analyst is most impressed by Arcadium’s potential for future expansion. He writes, “While there is no getting around the fact that the day-to-day trading action in all lithium stocks is tied to the underlying commodity, here are three reasons to own Arcadium beyond simply a commodity call. First, with the inaugural guidance for the combined company having come out in February, 2024 is set to be a year of cash flow neutrality, i.e., operating cash flow covering essentially all of the capital spending… Second, capacity expansion points to 2024 volumes posting healthy growth as the year progresses… Third, there should be increasing evidence of post-merger synergies over the next several quarters. Cost synergies are targeted at $125 million per year by 2027.”

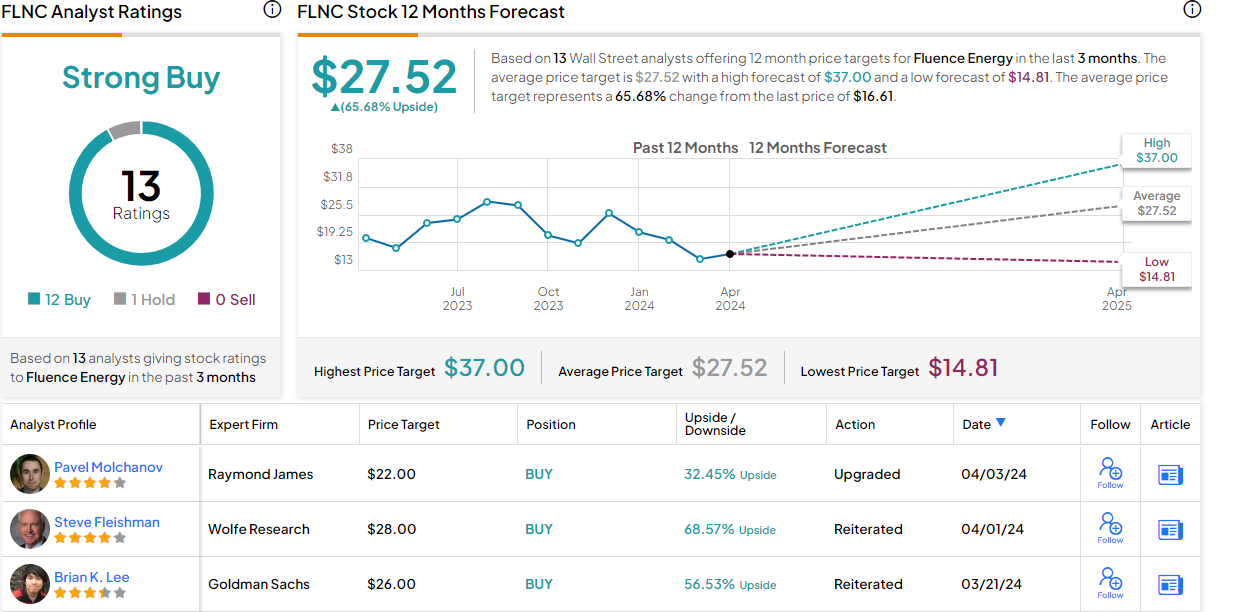

The Raymond James analyst recently upgraded his stance on this lithium stock from Outperform (Buy) to Strong Buy, and set a price target of $9, showing his confidence in a one-year upside of 115%. (To watch Molchanov’s track record, click here)

Amongst Molchanov’s colleagues, 6 others join him in the bull camp, 5 Recommend to Hold and one implores to Sell, all coalescing to a Moderate Buy consensus rating. There’s plenty of upside projected; the shares are trading for $4.19 and their $7.65 average target price suggests an 82.5% gain lying in wait for the coming year. (See ALTM stock forecast)

Fluence Energy (FLNC)

The second stock we’ll look at is Fluence Energy, a specialist company in energy storage. Fluence has created a line of products optimized for energy storage that are both scalable and economical, capable of operating at multiple levels, and featuring a modular construction that allows for ready customization or expansion. Customers can choose a wide range of installations, from large, grid-scale systems to smaller modular units. Fluence even has energy storage systems that are specifically designed to operate in conjunction with photovoltaic panels, a necessity in supporting solar power generation.

Fluence’s installations, based on its Gridstack storage units, are offered as turnkey projects, amenable to quick delivery and setup at the customer’s location. The company’s systems are designed to go online as soon as they are installed, so that customers can realize the benefits immediately. Fluence has several lines of energy storage systems available for customers to choose from, and all can be scaled to meet the customer’s needs.

Perhaps most importantly, from the customer perspective, Fluence offers four levels of support services – again, making the service scalable to the customer’s needs. These levels range from ‘guided service,’ in which Fluence teaches the customer’s maintenance team how to keep up with the energy storage system, to ‘asset management,’ in which Fluence handles all aspects of energy storage maintenance, making the project seamless from the customer’s perspective.

This company recently reported its financial results for fiscal 1Q24 (December quarter) and showed some important gains. Quarterly revenue came to $364 million, up 17% year-over-year, and the contract backlog expanded from $2.9 billion as of September 30, 2023, to $3.7 billion as of December 31. The company’s net loss narrowed year-over-year, from $37.2 million in fiscal 1Q23 to $25.6 million in the current report.

Fluence’s successes, in expanding its business and narrowing its losses, are attractive to analyst Molchanov, who says of the company, “We are turning positive on Fluence for the first time in its three-year history as a public company. It is hardly a revelation to point out that power storage for the grid represents a play on both climate megatrends: mitigation and adaptation. The former reflects the fact that intermittent renewables (wind and solar) are gaining share in the electricity mix around the world, and storage is essential for utilities to manage the grid’s supply/demand balance. The latter reflects the fact that the grid is experiencing more frequent and severe disruptions due to the worsening climate crisis, and enterprises – especially mission-critical ones such as data centers – need to protect themselves from power outages. With that in mind, U.S. storage installations more than doubled in 2023, with similarly robust growth around the world, and this is set to continue.”

Getting to the nitty-gritty, the analyst adds, “Bottom line: with valuation having come down to 14x FY26E adjusted EBITDA, we are ready to get on board.”

This is another stock that the Raymond James analyst has upgraded; he has moved his rating here from Market Perform to Outperform (i.e. Buy). This is complemented by a $22 price target that implies a one-year potential gain of 32.5%.

Molchanov is not the only bull here – far from it. The stock’s 13 recent analyst reviews include 12 Buys against a single Hold, for a Strong Buy consensus rating, and the $27.52 average target price suggests the shares will appreciate almost 66% from the current $16.61 trading price. (See FLNC stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.