The stock market continues to show bullish momentum, with tech companies, much like last year, emerging as key winners. Despite experiencing some volatility in late summer, the NASDAQ index has climbed 24% year-to-date and remains on a generally upward trajectory.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

While industry giants like Nvidia have dominated headlines, Berenberg analyst Nay Soe Naing is turning attention toward under-the-radar names in the chip software space.

To delve deeper, we’ve leveraged the TipRanks data platform to gauge Wall Street’s sentiment on two such stocks recommended by Naing. Both come with Buy ratings and promising upside potential. Let’s dive into the details, along with key insights from the Berenberg analysis.

Synopsys (SNPS)

The first company we’ll look at here, Synopsys, is a specialist in electronic design automation, with a focus on silicon design, the important first step in the manufacturing process for silicon semiconductor chips. The company offers solutions for silicon design and verification, silicon intellectual property, and systems verification and validation, and bases its solutions on artificial intelligence (AI) and software-defined systems. Synopsys boasts that its technology, and the tech and software solutions that it provides, make possible the innovations behind many of today’s big headline generators – autonomous vehicles, machine learnings, and high-speed communications, among others.

In recent weeks, Synopsys has made announcements showing that it is both expanding and streamlining its business. On the streamlining side, the company sold off its optical solutions group to Keystone Technologies, a leader in the field of design and emulation test solutions. The terms of this deal were not disclosed. And on the expansion side, Synopsys at the end of September entered into an agreement with TSMC, the world’s second-largest chip maker by market cap and third-largest by revenue, to provide advanced EDA and IP solutions to support TSMC’s most advanced technological process and manufacturing lines.

Synopsys may not be a household name, but it is big business. The company has more than 35 years’ experience, and employs over 19,000 people – and brought in over $5.8 billion in revenue for calendar-year 2023.

In its most recently reported quarter, for fiscal 3Q24, the company brought in $1.526 billion at the top line, for a 13%-plus year-over-year gain and beating the forecast by $10 million. The company’s bottom line, by non-GAAP measures, came to $3.43 per share, growing 27% year-over-year and beating expectations by 14 cents per share. Synopsys followed these sound results by guiding toward 15% y/y revenue growth for fiscal 2024; achieving that would be a company record.

For Berenberg analyst Naing, the key here is this company’s solid position leading its niche, as he writes, “Synopsys, much like its peers, is benefiting from the innovation-driven secular tailwinds in the semiconductor industry. However, as the largest semiconductor design solutions provider in the world, and with a differentiated product portfolio that is indexed more towards higher-growth product markets, and peerless in terms of innovation, we believe Synopsys’s medium-term growth potential is superior to that of its competitors, including its direct competitor Cadence.”

At his own bottom line, Naing says of Synopsys’ prospects, “While Synopsys’s profit margins may not be at the same level as some of the other sector leaders, it operates at incremental margins that are among the highest in the sector. In our view, Synopsys’s exceptional financial potential deserves a higher valuation multiple premium than it currently attracts.”

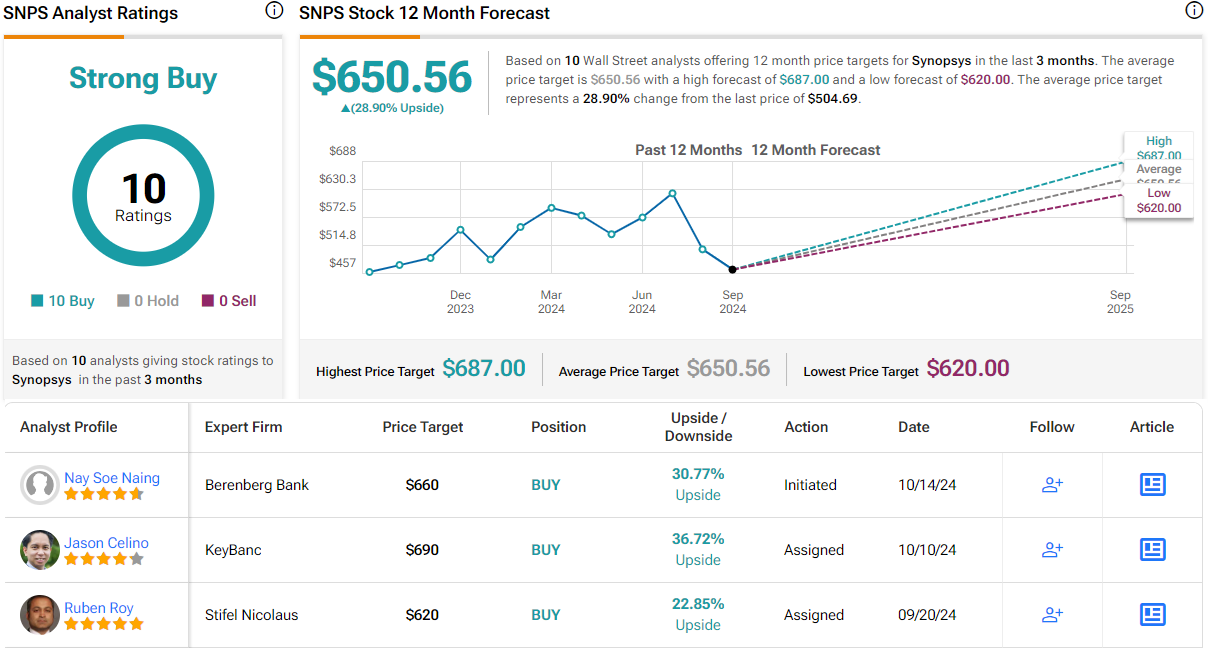

Naing initiates his firm’s coverage of SNPS with a Buy rating, and his $660 price target suggests that the stock will gain 31% heading out to the one-year horizon. (To watch Naing’s track record, click here)

The Strong Buy analyst consensus on Synopsys is unanimous, based on 10 recent reviews from the Street. The company’s shares are trading for $504.69 and the $650.56 average price target implies a potential one-year upside of 29%. (See SNPS stock forecast)

Cadence Design Systems (CDNS)

Next up is one of Synopsys’ chief competitors, Cadence Design Systems. Cadence has been in the business of electronic systems design since the early 1980s and is known for its software expertise. The company’s strategy is dubbed Intelligent System Design, and is used to deliver the best in software, hardware, and IP protections, and its services are used in a wide range of silicon-based technologies, including such vital components as semiconductor chips and integrated circuit boards and in industries from telecom to aerospace to life sciences.

Cadence saw $4.09 billion in sales last year, generated through a network that spans 26 countries around the world and employs over 11,000 people. The company’s product and service lines include analog and digital IC design; system verification; IC packaging and PCB design; Multiphysics and CFD analysis; and molecular modeling and biosimulation. The company’s work adds up to a broadly integrated set of end-to-end design solutions essential for today’s electronic designers to produce innovative products.

This month alone, Cadence has made a commitment to enter the imecAutomotive chiplet program, a collaborative endeavor to develop and produce the chiplets and chip sets that will inhabit the next generation of automobiles and make possible fully autonomous vehicles. In addition, Cadence has also announced that it will now integrate Nvidia NeMo and NIM microservices into its own generative AI applications, improving its own ability to innovate in semiconductor design.

On the financial side, Cadence saw 2Q24 revenues of $1.06 billion, $20 million better than had been anticipated and up 8.5% year-over-year. The quarterly EPS, of $1.28 in non-GAAP figures, was 5 cents per share better than the forecast. Looking ahead, Cadence finished the second quarter with a work backlog totaling $6 billion.

Opening his coverage of Cadence for Berenberg, Naing first points out the company’s solid industry position, saying, “Cadence, as one of the world’s largest semiconductor design solutions providers, plays an important role in driving innovation in the semiconductor industry. As such, it is benefiting from the structural trends in the semiconductor industry that are driven by technological advancements. At the same time, Cadence’s business, which is driven by R&D spending, is shielded from the cyclicality of the semiconductor industry.”

The analyst goes on to outline an upbeat path for Cadence in the coming year: “Also, owing to its best-in-class product portfolio and operational model, Cadence is outgrowing its peers and offers among the highest profitability potential of its peer group. In fact, we believe that Cadence will outgrow peers even faster than in recent years as it continues to capture the AI-driven semiconductor design opportunity.”

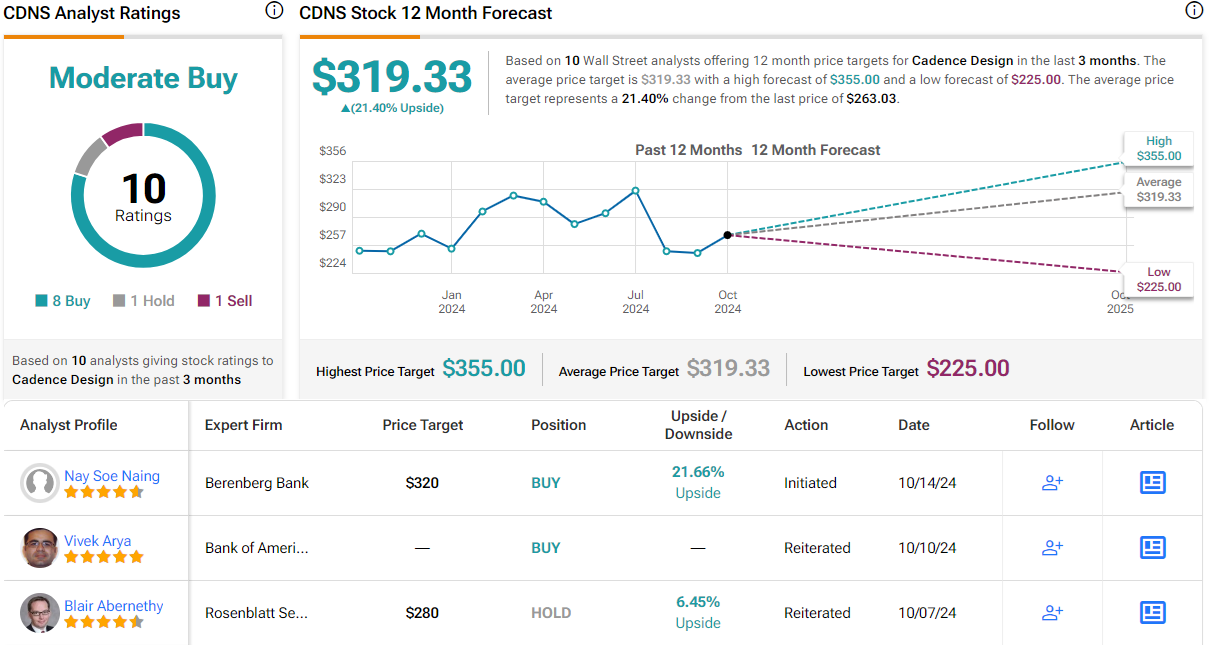

Unsurprisingly, this stance comes along with a Buy rating for the stock, and Naing’s $320 price target indicates his confidence in a one-year upside of 21.5%.

Like Synopsys above, Cadence has 10 recent Wall Street reviews on record. These include 8 to Buy, and one each to Hold and Sell, for a Moderate Buy consensus rating. The shares are trading for $263.03, with a $319.33 average price target, almost identical to Naing’s objective. (See CDNSstock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.