While Tesla’s recent Investor Day might have lacked the punch some investors were hoping for, CEO Elon Musk did double down on the need for a sustainable energy economy and stressed that it doesn’t have to come at the expense of other necessities.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

“There is a clear path to a sustainable-energy Earth,” Musk said. “It doesn’t require destroying natural habitats. It doesn’t require us to be austere and stop using electricity and be in the cold or anything.”

“In fact,” Musk went on to add, “you could support a civilization much bigger than Earth, much more than the 8 billion humans could actually be supported sustainably on Earth.”

Of course, it’s not only Musk who has such a forward-thinking agenda. There are many companies on the public markets pursuing those goals and they also offer opportunities for investors.

With this in mind, we dipped into the TipRanks database and pulled up the details on two sustainable energy stocks that have received a stamp of approval from Wall Street analysts, and offer solid upside potential. Let’s take a closer look.

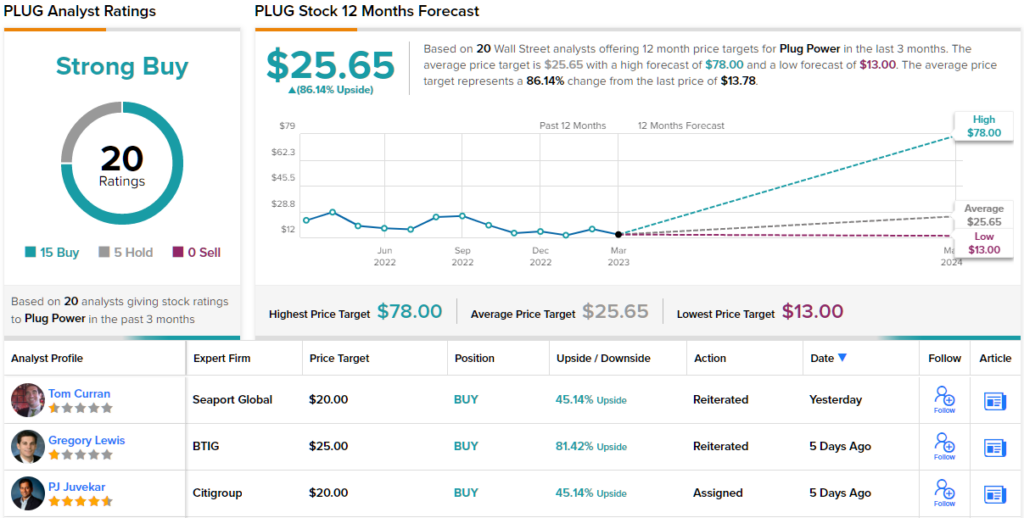

Plug Power (PLUG)

The first stock we’ll look at is a leader in a sector Musk has historically not been too keen on. However, while he was previously known as a big hydrogen skeptic, at the recent investor day, he conceded green hydrogen could yet have a role to play in assisting the world’s pivot to a sustainable energy future.

That is certainly the agenda of Plug Power. The company is at the forefront of the burgeoning global green hydrogen economy, for which it is building an end-to-end green hydrogen ecosystem. Its activities range from production, storage and delivery to energy generation — all designed to help clients reach their targets whilst decarbonizing the economy. The pursuit of that goal, however, has seen the company rack up the losses.

The problem in the most recent quarterly report – for 4Q22 – was that Plug Power also failed to meet expectations at the other end of the scale. The company delivered record sales of $220.7 million – amounting to a 36.3% year-over-year increase – yet falling short of consensus expectations by $48 million. And although gross margins bettered the negative 54% on display in 4Q21, they still showed a negative 36% with the company dialing in an a $680 million operating loss over the course of 2022. On the plus side, the hydrogen specialist stressed it remains on course to deliver revenues of $1.4 billion in FY2023, above the Street’s expectation of $1.36 billion. The company also expects it will generate a 10% gross margin.

Taking a sanguine view, J.P. Morgan analyst Bill Peterson thinks the company can overcome “near-term challenges” although it will have to prove it is up to the task.

“We continue to believe Plug has good backlog coverage across its various businesses, though converting backlog to sales will be highly dependent on focused execution,” the analyst explained. “Plug continues to see strong demand from customers across its business segments despite near-term customer readiness delays, and top-line growth potential continues to impress, and especially so for electrolyzers and stationary power… we see room for continued gross margin improvements throughout 2023 coming from scale, efficiency, and subsidies, such that Plug could potentially meet its 2023 profitability targets.”

To this end, Peterson rates PLUG stock an Overweight (i.e. Buy), while his $23 price target makes room for 12-month gains of ~67%. (To watch Peterson’s track record, click here)

Most analysts agree with the J.P. Morgan view; based on 15 Buys vs. 5 Holds, the stock claims a Strong Buy consensus rating. There’s plenty of upside projected here; at $25.65, the average target suggests shares will climb 86% higher in the year ahead. (See PLUG stock forecast)

Brookfield Renewable Partners (BEP)

Next up, we have clean energy powerhouse, Brookfield Renewable, a big player in renewable power and climate transition solutions. The company owns and operates renewable energy assets across diverse segments including hydroelectric, wind, utility-scale solar, distributed generation, and carbon capture, amongst other renewable technologies. Brookfield is a global concern with its top-notch assets located on four continents that are adopting more sustainable and cleaner power generation practices — North America, Europe, South America and Asia-Pacific (APAC).

After several quarters of sustained growth came to a halt in 3Q22, the company put that right in the most recent quarterly report – for 4Q22. Revenue rose by 9.2% from the same period a year ago to $1.19 billion, while edging ahead of the Street’s forecast by $10 million. FFO (funds from operations) grew from $214 million, or $0.33/unit in 4Q21 to $225 million – amounting to $0.35/unit. Funds from operations for the full year exceeded $1.0 billion ($1.56 per unit), for an 8% year-over-year uptick.

The company also pays a juicy dividend, which since 2011 has grown by at least 5% each year. The company raised it again in February – by 5.5% to a quarterly payout of $0.3375. This currently yields a handsome 4.8%.

Assessing this renewable energy player’s prospects, Jones Research analyst Eduardo Seda highlights the advantages of the company’s long-term contracted model.

“We note that approximately 94% of BEPs 2022 generation output (on a proportionate basis) is contracted to public power authorities, load-serving utilities, industrial users, and to Brookfield Corporation, and that BEP’s power purchase agreements (PPAs) have a weighted-average remaining duration of 14 years on a proportionate basis,” Seda explained. “As a result, BEP is able to enjoy both long-term visibility and stability of its diversified revenue and cash flow generation, and moreover, its distribution growth which is based on long-term sustainability.”

These comments underpin Seda’s Buy rating on BEP, which is backed by a $37 price target. Should the analyst’s thesis go according to plan, investors will be sitting on one-year returns of ~32%. (To watch Seda’s track record, click here)

Elsewhere on the Street, the stock receives an additional 2 Buys and Holds, each, all culminating in a Moderate Buy consensus rating. The shares are selling for $28.10, and their $35.83 average price target suggests room for 27.5% upside potential over the next 12 months. (See BEP stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.