The big question: Has the market hit a bottom yet? Well, according to Oppenheimer’s Head of Technical Analysis Ari Wald, there are signs one is forming, the most notable of which is that the Russell 2000 index – the barometer for small-cap stocks – “held to the June lows in the most recent late Q3 move to the downside.”

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Wald also notes that the signal of a market top is when the S&P 500 makes a “higher high, and small caps make a lower high,” and we are currently seeing the opposite scenario play out which might point to a market bottom.

Whether Wald is right or not remains to be seen, but in the meantime his analyst colleagues at Oppenheimer have noted 2 names that they think are well-positioned to push higher from here. We ran the tickers through the TipRanks platform to see what the rest of the Street has in mind for them. Let’s take a closer look.

Corebridge Financial, Inc. (CRBG)

We’ll start with Corebridge, a financial services and insurance products provider based in Texas. Its main offerings include Individual Retirement, Group Retirement, Life Insurance and Institutional Markets.

Many stocks have collapsed in 2022 but Corebridge has managed to sidestep the bear market. That, however, is entirely down to the fact this name is a stock market newbie. In September, Corebridge raised $1.68 billion, in what was the year’s biggest U.S. IPO, after being spun out from parent company AIG (the proceeds went directly to AIG).

While the company has yet to report any quarterly financial statements as a public entity, it should be noted that with more than $350 billion in assets under management, it is one of the biggest providers of retirement financial products, and a highly profitable one at that; in the first six months of the year, Corebridge generated revenues of $15.7 billion, while profit more than doubled from the same period a year ago to $6.4 billion.

In his initiation note, Oppenheimer analyst Chris Kotowski highlights the “strong cash generation potential.”

“As the life insurance operation of AIG, Corebridge has in recent years delivered more than $2B annually in adjusted earnings and cash distributions to its former parent,” The 5-star analyst said. “In the future, we see that cash coming to shareholders in the form of both dividends (currently targeted at $600M annually) and share buybacks, which we would expect to commence within a few quarters. We expect about $2.4B in adjusted earnings in 2023E, and management is targeting a total return to shareholders of 60-65%, which would equate to ~$1.5B, or a double-digit cash return given the current $13.1B market capitalization, plus capital retention for future growth.”

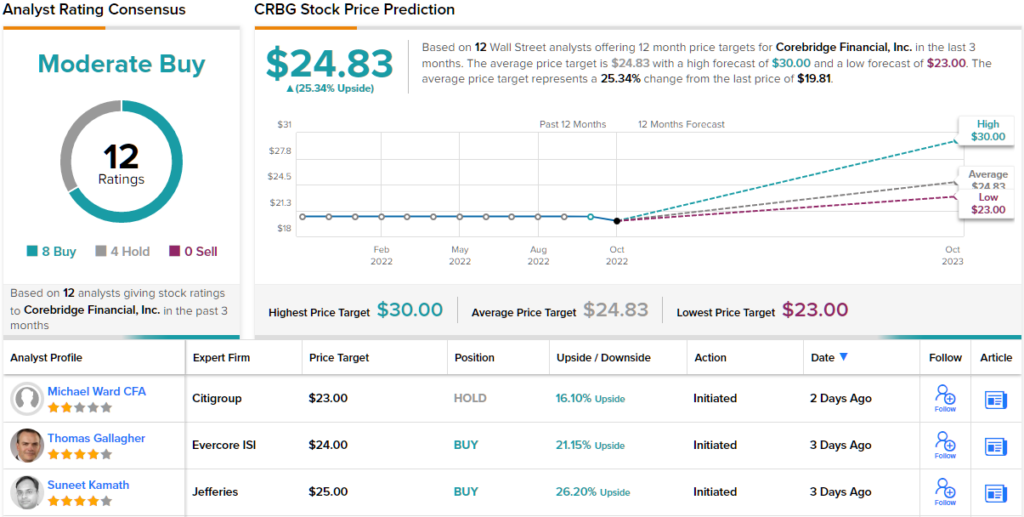

To this end, Kotowski puts an Outperform (i.e., Buy) rating on CRBG, backed by a $30 price target. The implication for investors? Upside of 51% from current levels. (To watch Kotowski’s track record, click here)

Overall, this new stock has a Moderate Buy rating from the analyst consensus, after attracting 12 reviews since the IPO. These reviews break down 8 to 4 in favor of the Buys over the Holds. Shares in CRBG are selling for $19.81 and the stock’s $24.83 average price target suggests it has room for 25% upside potential in the next 12 months. (See CRBG stock forecast on TipRanks)

POINT Biopharma Global (PNT)

The next stock we’ll look at is POINT Biopharma, a researcher in the field of radiopharmaceutical drug development and evaluation. Radiopharmaceutical therapy is an approach which uses radiation to target specific cancer cells with minimal impact on otherwise healthy cells. As such, the company is focused on developing and bringing to market radioligands that take the good fight to cancer.

POINT has several candidates in the early-stages of development, including potential pan-cancer target PNT2004, a best-in-class FAP-α targeted radioligand.

The company also has two late-stage programs in progress. One is for PNT2003, a somatostatin receptor (SSTR) targeted radioligand therapy being developed to treat patients with SSTR-positive neuroendocrine tumors. Its trial is now fully enrolled, and a data readout is expected later this year.

The other asset on the radar right now is PNT2002, currently being assessed in the Phase 3 SPLASH study and indicated as a treatment for metastatic castration-resistant prostate cancer (mCRPC). In the U.S., 52,000 men are either diagnosed with or progress to mCRPC each year. The company recently presented early positive data from the study.

Among the bulls is Oppenheimer analyst Jeff Jones who thinks the future is bright for this biotech.

“We see PNT as a leader in the radiopharmaceutical therapeutics (RPT) space based on: 1) deep pipeline, with two late-stage clinical programs—PNT2002 in PSMA + metastatic castration resistant prostate cancer (mCRPC) and PNT2003 in neuro-endocrine tumors (NETs)—each targeted for launch in 2025; 2) a robust supply-chain foundation which we see as critical for success in the RPT space; and 3) platform technology that may provide substantial differentiation for future drug candidates. PNT’s >$300M in cash, inclusive of its latest financing, supports operations through 2024E, positioning PNT for significant clinical read-outs, pipeline maturation, and commercial launch preparations,” Jones wrote.

POINT shares have bucked the trend for widespread losses in 2022 and even after a recent public offering of common stock sent shares lower, they are still up 38% since the turn of the year.

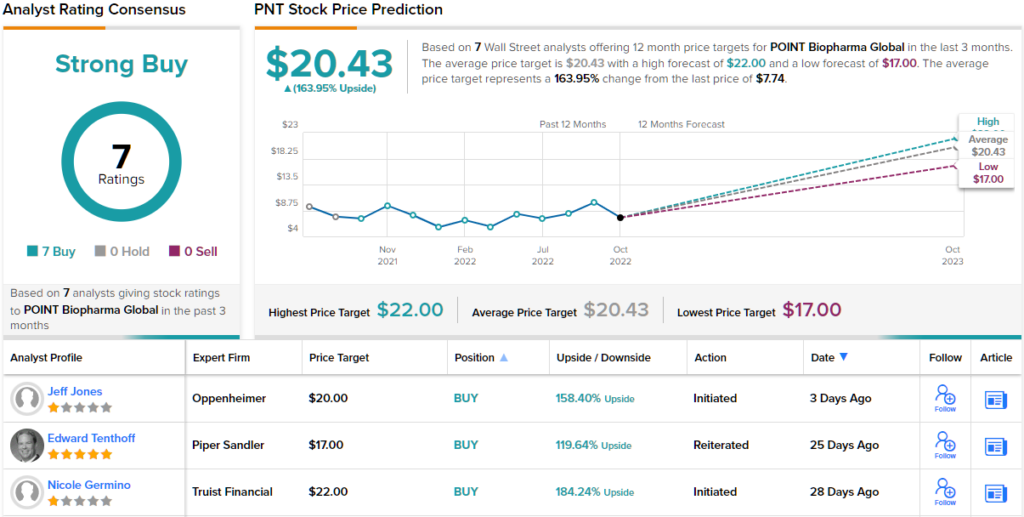

Jones evidently thinks there’s plenty of room left to run. Along with initiating coverage with an Outperform (i.e., Buy) rating, the analyst’s $20 price target implies shares will be changing hands for a 158% premium a year from now. (To watch Jones’ track record, click here)

All in all, some stocks make a roundly positive impression on Wall Street’s analysts, and PNT is one of those. This radiopharmaceutical researcher has a unanimous Strong Buy consensus rating, based on 7 recent positive reviews. The shares are priced at $7.74 and the average price target is even a touch higher than Jones would allow. At $20.43, it suggests that PNT shares can appreciate ~164% in the coming 12 months. (See PNT stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.