The energy landscape is constantly evolving, and today we are witnessing a significant shift.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The latest edition of Goldman Sachs’ Carbonomics report outlines the likely mid- to long-term course of America’s shale revolution. This report examines the technological advancements in exploration and extraction that transformed the US into a net oil exporter by 2018. Written under the leadership of the 5-star analyst Michele Della Vigna, the report elucidates the maturation and concluding phases of the shale industry.

Della Vigna goes on to lay out how renewable energy tech has the potential to unlock as much as double the energy scale of the shale revolution – and to make possible some $3 trillion in energy infrastructure investment by 2032. The analyst points out several supportive factors that will boost clean energy technology through the end of this decade, with a particular focus on the $1.2 trillion in government subsidies and incentive funding laid out in the Inflation Reduction Act of 2022.

In the Goldman view, the flood of Federal cash and the huge return potential for this ‘third American energy revolution’ make now the time for investors to start looking closely at green energy stocks. The firm’s analyst, Adam Samuelson, is on the job, recommending the stocks that will lead the charge into the new energy economy of the next decade.

We’ve used the TipRanks platform to pull up the details on three of his picks – it turns out all are rated as ‘Strong Buys’ by the analyst consensus. Let’s dive in.

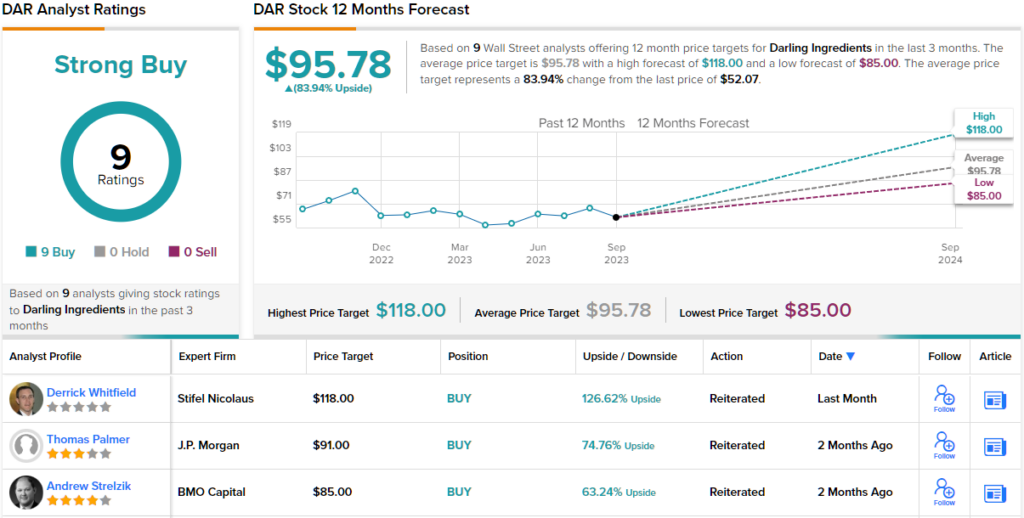

Darling Ingredients (DAR)

First up on the list is Darling Ingredients, a food industry company with an interesting connection to renewable fuels. Darling works on the recycling side of the food industry, collecting and processing edible by-products and food waste to create useful, sustainable products and renewable energy. The company operates over 260 facilities on five continents, gathering and repurposing approximately 15% of the waste generated by the global meat industry.

This gathered waste is processed into collagens, fertilizers, pet food ingredients, and useful animal proteins and meals. On the energy side, Darling’s operation can generate green energy in the form of renewable diesel. These value-added products bring a host of benefits, chiefly the reduction of potentially dangerous waste clogging up landfills and other disposal facilities. Darling’s largest footprint is in North America, where it has more than 170 locations; the company also operates 50+ facilities in Europe and has smaller operations in Asia, South America, and Australia.

Of particular interest to green energy investors is Darling’s partnership with the Texas-based petro-fuel company Valero. The two firms have a 50/50 agreement to operate Diamond Green Diesel, the world’s lowest cost and highest ‘green premium’ producer of renewable biodiesel. The company, also known as DGD, has been expanding due to increased demand for low-carbon alternative fuels and increased government regulations mandating lower carbon footprints and higher renewable levels. During the second quarter of this year, DGD saw record renewable diesel sales of 387.8 million gallons and realized an average EBITDA per gallon of $1.28. For 2023 as a whole, the venture’s sales have totaled 643.3 million gallons, with a $1.17 average EBITDA per gallon.

For Darling as a whole, 2Q23 saw the company bring in $1.75 billion in total revenues. While up 6% year-over-year, this figure missed the forecast by $100 million. Darling’s bottom line, the EPS of $1.55 per share, was 1 cent below expectations.

Goldman Sachs’ Adam Samuelson doesn’t hesitate to recommend this stock, despite the earnings miss. He sees the renewable biodiesel business as a key attraction, and writes, “We continue to believe DAR remains a uniquely advantaged, integrated low-CI feedstock and renewable diesel producer, with the shares offering a compelling entry point at 7.5x 2024E EV/EBITDA and >10% FCF yield. We expect both of these factors to come increasingly in focus over the next 6-12 months as steady DGD distributions drive a sharp inflection in parent FCF, deleveraging, and ultimately accelerating cash returns, while industry-wide RD expansion accelerates feedstock demand for the parent business and puts a spotlight on DGD’s margin advantage versus peers.”

Samuelson goes on to give the stock a Buy rating with a $102 price target indicating potential for an increase of a strong 95% in the coming year. (To watch Samuelson’s track record, click here)

Overall, the Strong Buy consensus rating on Darling is unanimous, based on 9 positive Wall Street reviews of the stock. The shares are priced at $52.07 and their $95.78 average price target implies a one-year gain of 84%. (See DAR stock forecast)

Green Plains (GPRE)

Next up on our list is Green Plains, a company in the bio-refining field, developing and producing low-carbon biofuels that can power our existing transportation network while also reducing tailpipe emissions. The company’s operations extend to industrial alcohols, corn oils, animal feeds, and pet foods as well, making Green Plains a well-diversified firm in the realm of biorefining organic products and waste.

Green Plains has extensive operations in the US Plains states and in the Mississippi Valley, and its 10 biorefineries, in the states of Minnesota, Iowa, Nebraska, Illinois, Indiana, and Tennessee, are capable of processing more than 300 million bushels of corn annually. The net product includes over 1 billion gallons of low-carbon biofuels, including ethanol, of which Green Plains is one of North America’s most important producers. The company also produces over 290 million pounds of renewable corn oils every year, and some 2.5 million tons of distillers grains and ultra-high protein products.

Our technological and industrial economy has an insatiable appetite for fuels, and Green Plains has a ready market for its products. Meeting that demand in the last quarter reported, 2Q23, the company showed a top line of $857.6 million. This result was down from $1.01 billion in the prior-year quarter but came in $52.2 million above the estimates. At the bottom line, Green Plains’ EPS was a net loss, of 89 cents per share, a result that was 79 cents per share worse than expected and compared unfavorably to the 73-cent net EPS profit reported in 2Q22. The company notes that second-quarter earnings in 2Q22 received a heavy boost from a one-time USDA pandemic relief payment of $27.7 million.

Goldman’s Samuelson sees Green Plains holding a solid position, despite y/y volatility in revenues and earnings, with its high capacity for generating useful low-carbon renewable fuel feedstocks. Demand for these products, and Green Plains’ other useful biofuel feedstocks, in his view, should provide support going forward.

“GPRE has ~1bn gallons of ethanol capacity (~6% of US capacity), which we believe to be a key feedstock for sustainable aviation fuel (SAF) production to take off, through the alcohol-to-jet (ATJ) technology. In addition, the company offers a multifaceted growth agenda pivoting around a lower carbon footprint, including corn oil production (low-carbon feedstock for renewable fuels) and clean sugar and protein technologies,” Samuelson noted.

These comments back up Samuelson’s Buy rating on GPRE shares, while his $39 price target implies an upside of ~30% in the next 12 months.

Zooming out, we find a Strong Buy consensus rating on this stock, supported by 8 recent analyst reviews that include 6 Buys and 2 Holds. The shares are priced at $30.06 and have a 32% one-year upside potential based on the average target price of $39.57. (See GPRE stock forecast)

Archer-Daniels-Midland Company (ADM)

Last on our list of Goldman biofuel picks is the Archer-Daniels-Midland Company, better known by its ADM initials. This is an agribusiness with a global footprint, operating in the production of both human and animal nutrition. In addition to working on healthier food products, ADM is also focused on improving our environment, through the development of plant-based substitutes for petroleum products.

ADM’s global business is composed of several segments, including human nutrition, animal nutrition, pet nutrition, and industrial biosolutions. These cover most of the feasible uses for the world’s large-scale farm crops, and can even make use of the crops’ agricultural waste products. The company’s work aims to make agriculture, at all scales, more productive and more sustainable, with direct access to the food processing industry and global supply chains.

The important point here is ADM’s industrial solutions segment, which includes an important biodiesel component, with strong demand both domestically and on the international export market. ADM supplemented this in its last reported quarter, 2Q23, with increased production of food oils, increased South American production of agricultural food products, and increased demand for softseed products that partially offset lower demand for soybeans and their derivatives.

Overall, this diverse business, with its massive global footprint, makes ADM a giant among the world’s agricultural companies. The firm has a market cap of $40 billion, and realized over $101 billion in revenues last year. In its last reported quarter, 2Q23, ADM’s top line came to $25.2 billion, a result that was considered a bit disappointing, as it was down 7.7% y/y and missed the forecast by $520 million. The company’s earnings result, a non-GAAP EPS, was more upbeat; at $1.89 per share, the EPS figure was 30 cents per share better than had been anticipated.

Checking in again with Goldman analyst Adam Samuelson, we find him upbeat on this company’s varied product lines and markets, and their inherent profit potential. Samuelson writes of ADM, “We see a favorable industry operating environment across the majority of ADM’s upstream value streams, notably underpinned by sustained expansion in vegetable oil demand for renewable diesel, coupled with solid execution, supporting results at-or-above the high end of the company’s $6-7 2025 EPS target range over the next two years.”

Looking ahead from here, Samuelson gives ADM a Buy rating with a price target of $102 suggesting an upside of ~36% for the coming year. (To watch Samuelson’s track record, click here)

All in all, this stock’s Strong Buy consensus rating is based on 7 recent Buys from the Street’s analysts, along with 2 Holds. The average price target here is $100.78, implying a gain of nearly 34% from the current $75.12 trading price. (See ADM stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.