Successful investing is all about building the right portfolio, populating it with stocks that will generate solid returns over the long run. Sounds simple, right? The only ‘trick’ is finding stocks that fit that profile, and the key is right in front of us, waiting in the raw data of the stock market.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Therein lies the rub. The markets toss up a huge volume of information, based on thousands of traders dealing in thousands of stocks – the result is millions of transactions every day, and it’s the work of a lifetime to make sense of it all. Even Wall Street’s best analysts will usually focus on a segment of the whole.

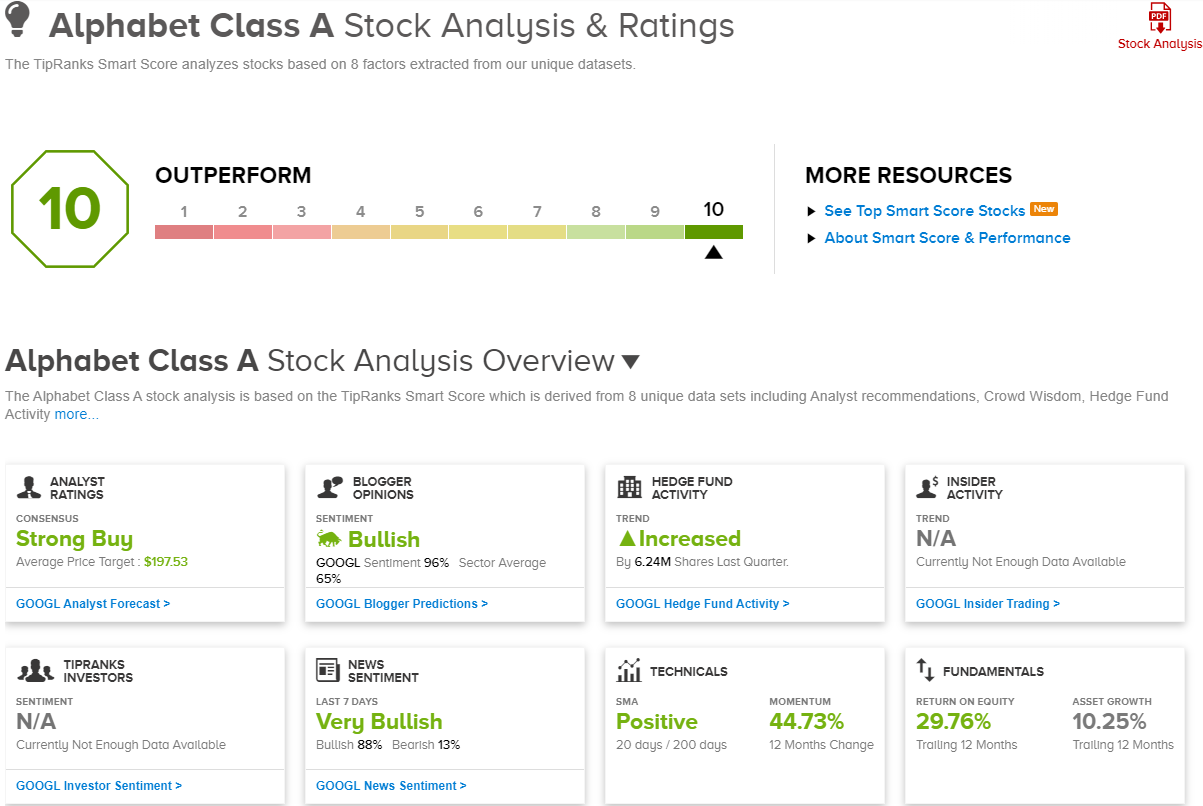

This is where the TipRanks Smart Score comes in. It’s a data sorting and collating tool, based on a combination of AI and natural language processing, designed to gather all the data on any given stock and then compare that stock’s performance to a set of factors known as accurate predictors of future outperformance. The stock’s comparison results are then distilled into a single score, on a scale of 1 to 10. A stock that rings in at a ‘Perfect 10’ is one that has definitely earned additional investor interest.

That’s especially true when market-leading companies like Alphabet (NASDAQ:GOOGL) and Alibaba (NYSE:BABA) are picking up the ‘Perfect 10’ Scores. We’ve used the TipRanks database to look up the bigger picture on both; these top-scoring stocks also bring Strong Buy ratings and double-digit upside potentials to the table. Here are the details.

First up, a giant of the tech world. Best known as the parent company of both Google and YouTube – Alphabet is the leader in the world of online search and holds a dominant position in online advertising and video content distribution. The company recently became just the fourth Wall Street firm to surpass $2 trillion in market cap, and is one of just six publicly traded companies with a market cap exceeding $1 trillion. Currently, Alphabet is valued at $2.17 trillion.

Given its overall strong position in tech, Alphabet is at the forefront of development in the AI field, and is applying generative AI to its Google search engine, and to its Google Cloud subscription service. Alphabet even has an autonomous driving division, Waymo, that has put AI-based self-driving vehicles on the streets of San Francisco.

At the financial bottom line, Alphabet’s earnings have been on an upward trajectory for the past year. In the company’s most recent earnings report, covering 1Q24, Alphabet reported $1.89 in EPS, up from $1.17 in the prior year and 38 cents per share better than had been anticipated. The company’s revenues, which totaled $80.54 billion and beat the forecast by $1.84 billion, were powered by advertising revenue. Ad revenue for the quarter came to $61.7 billion, up 13% year-over-year.

All of this – the solid business model, the tech leadership, and the strong finances – have caught the attention of Tigress analyst Ivan Feinseth, who writes of Alphabet, “Search and Advertising revenue will continue to see accelerating growth, and the ongoing integration of AI functionality will continue to drive its leadership position across all key technology trends and business lines. GOOGL continues to benefit from strong advertising revenue and user engagement, driving another quarter of strong results across all key business lines, including Cloud, which continues to benefit from increasing AI integration.”

The 5-star analyst goes on to give these shares a Buy rating with a $210 price target that points toward a one-year upside potential of 20%. (To watch Feinseth’s track record, click here)

Like most tech giants, Alphabet has picked up plenty of Wall Street recommendations – no fewer than 37, with 32 Buys and 5 Holds to back up the Strong Buy consensus rating. Shares in GOOGL are selling for $174.99 and the $197.53 average target price implies a gain of nearly 13% in the next 12 months. (See GOOGL stock forecast)

Alibaba

Next up is Alibaba, best known as the ‘Amazon of China.’ That’s a bit unfair, really. Alibaba is a powerful online retail and services tech company in its own right. The company’s founder is the near-legendary Chinese tech entrepreneur and innovator Jack Ma, and his creation is the absolute leader in China’s domestic online retail market. The company has been in business since 1999, and has branched out beyond China’s borders, and beyond ecommerce.

The company does offer a wide range of online retail services on the global market, and has moved into other tech sectors, including digital media, entertainment, and cloud computing. The company has several business segments, including innovation initiatives, but its chief business remains the Chinese Commerce segment.

That core business gives Alibaba a solid foundation to stand on. China has a population of approximately 1.4 billion, including approximately 800 million in its expanding urban regions. In its domestic market, Alibaba offers an unparalleled range of products and boasts that it can deliver anything to anywhere in China, with guaranteed next-day or 2-day delivery. The company’s global online retail side features nearly 6,000 product categories and over 200,000 suppliers making more than 200 million products available in over 200 countries.

Alibaba last reported financial results for fiscal 4Q24, which ended on March 31 of this year. The company’s top line came to $30.73 billion, up 7% from the prior fiscal year Q4 and some $310 million over the estimates. The company’s bottom line was reported as $1.40 by non-GAAP measures, missing the forecast by 2 cents per share.

This retail and tech company attracted a review from Benchmark analyst Fawne Jiang, who thinks BABA’s strengths outweigh potential headwinds. Jiang writes, “Key drivers for the next leg of the stock, in our view, are 1) sustainability of positive market share dynamics, 2) ecommerce monetization improvement driven by new ad product launch (slated in F2H25) to close the gap of CMR and GMV; and 3) reaccelerated cloud growth bolstered by AI cloud (F2H25). Uncertainty remains in light of 1) GMV growth largely depends on consumer sentiment (recently improving); 2) investment may create profitability volatility in the near Qs and FY25. Net net, we are incrementally more comfortable for a potential full-fledged turnaround playing out in F2H25 along with a stabilizing macro backdrop.”

For Jiang, another of the Street’s 5-star stock pros, these shares have earned a Buy rating, along with a $118 price target that suggests a 45% upside on the one-year horizon. (To watch Jiang’s track record, click here)

BABA’s 17 recent stock reviews include 14 Buys to 3 Holds, for a Strong Buy consensus rating, and the average target price, of $103.46, implies an upside of 27% from the current share price of $81.26. (See BABA stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.