The auto industry is changing in a multitude of ways. Electric powertrains are challenging the traditional combustion engine, and other technologies, such as mobile wireless connectivity and artificial intelligence, are bringing a sea change to the way we drive. New opportunities are opening for investors in these emerging technologies. These aren’t going to be risk-free choices – remember how many car companies popped up in the 1920s and ‘30s before Detroit stabilized with the Big Three – so the ‘trick’ to success will be recognizing potential winners.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

In this context, it’s worth noting LiDAR, the sensor technology crucial for enabling autonomous cars. LiDAR merges high sensitivity with AI, giving rise to intelligent sensors for autonomous vehicles. Despite its potential, early investors in LiDAR have faced challenges. The sector experienced overvaluation due to a surge of SPAC transactions as emerging companies sought capital. Nonetheless, the dynamics around this are changing, as explained by Craig Hallum analyst Richard Shannon.

“While the lidar space has been a poor performer since many of these stocks went public in the past 2-3 years, these stocks have started to bottom out in the last quarter… We think this is due to low valuations (negative EV in some cases, albeit using the last reported qtr’s cash) and the prospect of major awards to be announced in the next 6-18 months. As such, we think it’s now time for investors to more seriously consider the lidar space for long-term investment,” Shannon opined.

Shannon isn’t just analyzing the LiDAR industry as a whole, he’s also putting his finger on two stocks that he sees as winners. Looking into their details through the TipRanks database, we find that these are low-cost stocks – both well under $10 per share – and Shannon sees plenty of upside potential in them.

Cepton, Inc. (CPTN)

We’ll start with Cepton, an early researcher and builder in LiDAR tech that has been pushing the boundaries of how and where LiDAR can be used. The technology itself, whose name comes from ‘light detection and ranging,’ uses lasers to detect and track objects, with greater speed and sensitivity than infrared or radar systems. LiDAR can function as the ‘eyes’ of an autonomous vehicle, and Cepton is also working to adapt the system to smart cities and industrial applications.

Cepton’s LiDAR units are based on one of the company’s proprietary systems: Micro Motion Technology (MMT), which is mirrorless, rotation-free, and frictionless – allowing for 3D LiDAR imaging. The units are small enough to fit onto existing vehicle frames unobtrusively, providing driver assistance and autonomous systems with wide fields of view and high-resolution sensing in all weather conditions. Cepton has been collaborating with General Motors, a stalwart of the Detroit auto industry. It boasts an extensive presence in the Motor City, including an ‘excellence facility’ in Troy, Michigan, designed to offer local support to automakers and the supporting OEMs within their supply chains.

Earlier this week, the company unveiled its financial results for the second quarter of 2023, revealing total revenues of $2.79 million. This marked a 9% year-over-year increase and exceeded estimates by $0.27 million. These encouraging revenue figures were driven by record-breaking unit deliveries in both the automotive and smart infrastructure sectors, complemented by a rise in average selling prices. At the bottom line, Cepton revealed an EPS loss of 8 cents per share according to non-GAAP measures. This figure was in line with expectations.

Turning to Craig-Hallum’s Richard Shannon, we find the analyst taking an upbeat view of Cepton. He believes the company is well-positioned to expand its business, and that its current share price, below $1, represents a chance for investors to buy in at a significant discount.

“We highlight CPTN as a favorite idea in the lidar space, for a few reasons: 1) its valuation is inexpensive, even assuming the shares OS/dilution model we summarized above, 2) we think it has a good chance of winning one/multiple top 10 wins in the next year or more. The bear case involved the balance sheet and the stock being below $1.00, and both of those can be solved if it gets an OEM win before year’s end,” Shannon opined.

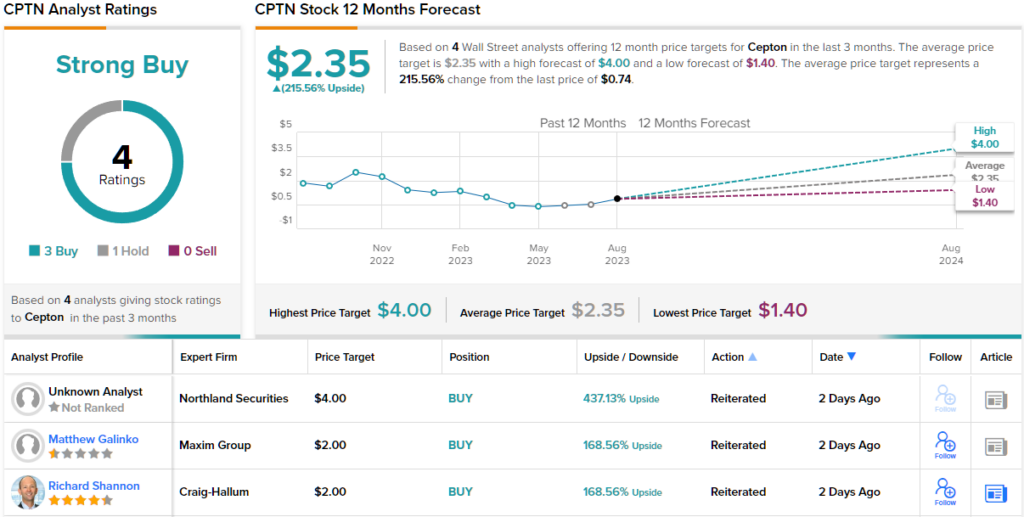

Quantifying his bullish stance, Shannon rates CPTN a Buy with a $2 price target that implies a robust 168% upside potential for the next 12 months. (To watch Shannon’s track record, click here)

Overall, there are 4 recent analyst reviews on Cepton, including 3 Buys against a single Hold, giving the stock its Strong Buy consensus rating. The shares are trading for just $0.74 each, and the $2.35 average price target suggests they will gain over 215% in the year ahead. (See CPTN stock forecast)

Ouster, Inc. (OUST)

Up next is Ouster, a cutting-edge LiDAR company based in San Francisco. The tech firm’s goal is to replace analog architectures in sensor systems – a complex legacy of older technologies – with simplified, semiconductor-based technology to accelerate product development, manufacturing, and the pace of customer adoption. Ouster’s digital technology plays a key role in LiDAR’s evolution.

The company designs and builds a range of LiDAR systems suitable for short-, mid-, and long-range applications, spanning from warehousing to industrial robotics and autonomous cars. In a move promising to expand this capability, Ouster announced a merger-of-equals with Velodyne, another player in the global LiDAR scene focusing on sensor hardware, in February of this year. This partnership grants the companies access to each other’s technologies, backed by a financial base including $315 million in cash, with estimated annual cost savings between $80 million and $85 million.

Ouster is poised to unveil its 2Q23 results today, with industry analysts estimating revenues of $19 million and non-GAAP earnings of $1.21 per share. For a snapshot of the company’s current status, a retrospective look at this year’s Q1 results proves insightful.

During the first quarter, revenue reached $17.23 million, falling short of forecasts by a mere $71K, but exhibiting a year-on-year growth of 101%. This revenue total was complemented by $33 million in quarterly bookings. At the bottom line, the non-GAAP EPS loss of $1.87 missed expectations by 15 cents. Notably, Ouster reported shipping over 3,000 sensor units in Q1, which included shipments of the new REV7 systems to 110 customers.

All of this has caught the attention of Richard Shannon, and the analyst writes of the stock, “We highlight OUST as a favored idea for two reasons: 1) it is the cheapest lidar stock, by a large margin, and 2) we think it’s highly likely it won’t have to raise any cash to get to breakeven. We note that our estimates are more bullish on a profit/cash flow basis than our competitors, and believe investors that scrub their numbers will come to this conclusion as we have.”

Shannon goes on to put a Buy rating on this stock, along with a $10 price target that points toward a 94% upside potential in the year ahead.

All in all, Ouster gets a Moderate Buy rating from the Street, based on 3 Buys and 2 Holds set in recent months. The $5.06 share price and $7.03 average price target combine to suggest a one-year gain of 36% for OUST. (See OUST stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.