Inflation chat is once again this week’s hot topic. December’s consumer price index (CPI) will be released on Thursday with analysts hoping a repeat of last month’s positive declaration in inflation levels.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

The forecast is for core CPI to have climbed 0.3% in December. While this is a touch higher than November, it would still be in line with the quarter’s average, and less than the 0.5% average exhibited between January and September against a backdrop of the highest inflation in decades.

The results will also provide an indication on whether the Fed will ease the scale of its rate hikes when it meets on Jan. 31-Feb. 1 to decide on the matter. The hope is that there will only be a 25 basis-point increase in the Fed’s benchmark rate, but a half-point increase is not out of the question either.

With all possibilities open, it’s best to take a prudent approach to stock picking right now and lean into the blue chip stocks – the companies with an excellent reputation and a history of success even in a difficult macro environment.

With this in mind, we delved into the TipRanks database and pulled out two such names – both stock market giants that outperformed the market last year and that could protect the portfolio against any incoming volatility. Let’s check the details.

Walmart Inc. (WMT)

Blue chip stocks, you say? Well, there’s no better place to start than with Walmart, officially the world’s largest company by revenue. As of October 2022, the retail giant topped the Fortune Global 500 list, generating around $570 billion in annual revenue. Walmart boasts 10,586 stores and clubs spread across 24 countries, operating under 46 banners, with ~2.3 million worldwide employees, of which 1.6 million are U.S.-based.

Walmart’s credentials as a stock to own in difficult times is reflected by its solid performance over the past year. Despite all the major indexes seeing out 2022 firmly planted in negative territory, WMT shares have sidestepped the carnage and are up by 2%.

That’s because in the real world, Walmart has shown it is resilient to the tough conditions. This was evident in the company’s most recent quarterly statement – for the third quarter of fiscal year 2023.

Revenue rose by 8.8% year-over-year to $152.8 billion, beating the Street’s call by $6 billion, while comparable sales grew by 8.2%, also above consensus expectations of 6.9%. On the bottom-line, the company delivered EPS of $1.50 – easily trumping the $1.32 forecast. Importantly, for Q4, Walmart expects consolidated net sales growth of around 5.5%, and said consolidated adjusted operating income is expected to drop by 6.5% to 7.5%, improving on its previous guidance of a 9% decline.

All of this caught the attention of Credit Suisse’s Karen Short who sees multiple reasons to have WMT shares in a portfolio. These include, “1) WMT has been gaining meaningful market share since early 2021; 2) Our view that WMT is a well-positioned defensive name in an uncertain macro backdrop; 3) Price gaps to conventional grocers remain wide; 4) A potentially weak macro backdrop should accelerate share gains;, 5) In light of a potential combination of two of the largest conventional food retailers (Kroger and Albertsons merger), we believe WMT is well positioned to be even more offensive than usual to gain share; and 6) Alternative profit streams should continue to evolve and contribute to operating profits.”

Unsurprisingly, then, the 5-star analyst rates WMT shares an Outperform (i.e. Buy) while her $170 price target makes room for gains of 17% in the year ahead. (To watch Short’s track record, click here)

Most analysts are reading off the same page; the stock claims a Strong Buy consensus rating, based on 20 Buys vs. 5 Holds. (See Walmart stock forecast)

Visa Inc. (V)

One of the most valuable firms in the world, Visa is a leader in international payments. The company doesn’t actually issue cards, extend credit, or set rates and fees for consumers. What it does is provide financial institutions with access to payment instruments that carry the Visa name, which they can use to provide credit, debit, prepaid, and cash access services to their customers. Over 200 countries and territories can accept digital payments thanks to its network, which can perform up to 30,000 transactions simultaneously and reach as much as 100 billion computations every second.

Visa’s most recent earnings report – for the fiscal fourth quarter of 2022 (September quarter) – was a strong one. Revenue climbed by 19% from the same period a year ago to $7.8 billion, beating Wall’s Street’s expectations by $250 million. The analysts were calling for adj. EPS of $1.86 but Visa delivered a much better $1.93. In further good news, the quarterly cash dividend was increased by 20% to $0.45 a share and a new $12.0 billion share repurchase program was also authorized.

This is the kind of stuff which has shielded Visa from the stock market wreckage; the shares climbed 4% over the past year. 2023 should be another good year, according to Evercore analyst David Togut, who lays out the bull case for V, bear market or not.

“V’s resilient business model and sizable moat around its network offers best-in-class risk/reward with downside protection in an uncertain macro environment and material upside opportunity in a rising economy,” the analyst explained. “With less than 50% of V’s revenue generated outside of the US and an inflation-hedged, ad valorem revenue model, we see moderate risk to V’s revenue as many international economies may underperform the US.”

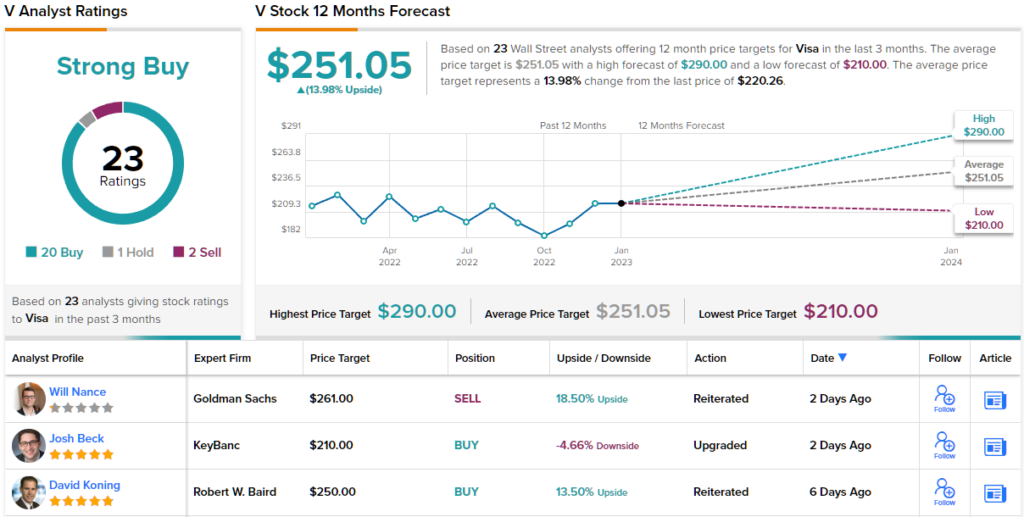

To this end, Togut rates V shares an Outperform (i.e., Buy) along with a $290 price target. The implication for investors? Upside of ~32% from current levels. (To watch Togut’s track record, click here)

As for the rest of the Street, most are on board, too. The ratings mix show 20 Buys, 1 Hold and 2 Sells, all coalescing to a Strong Buy consensus rating. (See Visa stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.