With Q3 drawing to a close, Tesla (NASDAQ:TSLA) will soon be announcing its quarterly delivery haul.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

After the first half of the year was marred by shrinking vehicle sales (down 13% year-over-year), Wedbush analyst Daniel Ives says he is seeing a “stabilization of demand globally” that should allow the company to surpass Street expectations for the quarter, with demand improving in the all-important Chinese region. Achieving a quarterly run rate of around 500,000 vehicles will be crucial, says Ives, as Tesla prepares to launch new models for customers in 2026. And while it’s true there are “weak pockets” in Europe, Ives believes Tesla is beginning to experience a pickup in demand, setting the stage for stronger growth through 2026.

However, that is not what really matters for the stock, as there are other far more important developments taking place right now, namely the big opportunity in AI. “We believe Tesla is taking major steps in advancing its AI Revolution path with autonomous and robotics front and center heading into 2026 that will be a game changer and define Tesla’s future,” Ives, who ranks amongst the top 4% of Street stock experts, went on to say.

Ives – a big TSLA bull – thinks the AI opportunity cannot be overstated. In a “bull case scenario,” he sees Tesla hitting a $2 trillion market cap in early 2026 and reaching $3 trillion by year-end as full-scale production of its autonomous and robotics initiatives ramps up. The AI valuation will “start to get unlocked,” with Ives believing the transition toward an AI-driven valuation over the next six to nine months is now at play. Key drivers include the adoption of FSD (full self-driving) across Tesla’s installed base and the rollout of the Cybercab in the US.

As no other company can match its combination of scale, scope, and expanding AI capabilities, Ives reckons Tesla could capture around 70% of the global autonomous market over the next ten years, and he expects FSD adoption to exceed 50%, potentially transforming Tesla’s financial model and margins.

Like Musk himself and other TSLA bulls, over the past decade, Ives has never viewed the company just as a carmaker but as a leading global tech disruptor. The first phase of this vision has unfolded over the last five years, and now Tesla is entering the “most important chapter” in its history, with a focus on an autonomous future. “Additionally,” the 5-star analyst said, “the new Musk pay package and what is likely a big stake in xAI to be approved at the shareholder meeting in November will be another key step in the AI story taking hold at Tesla.”

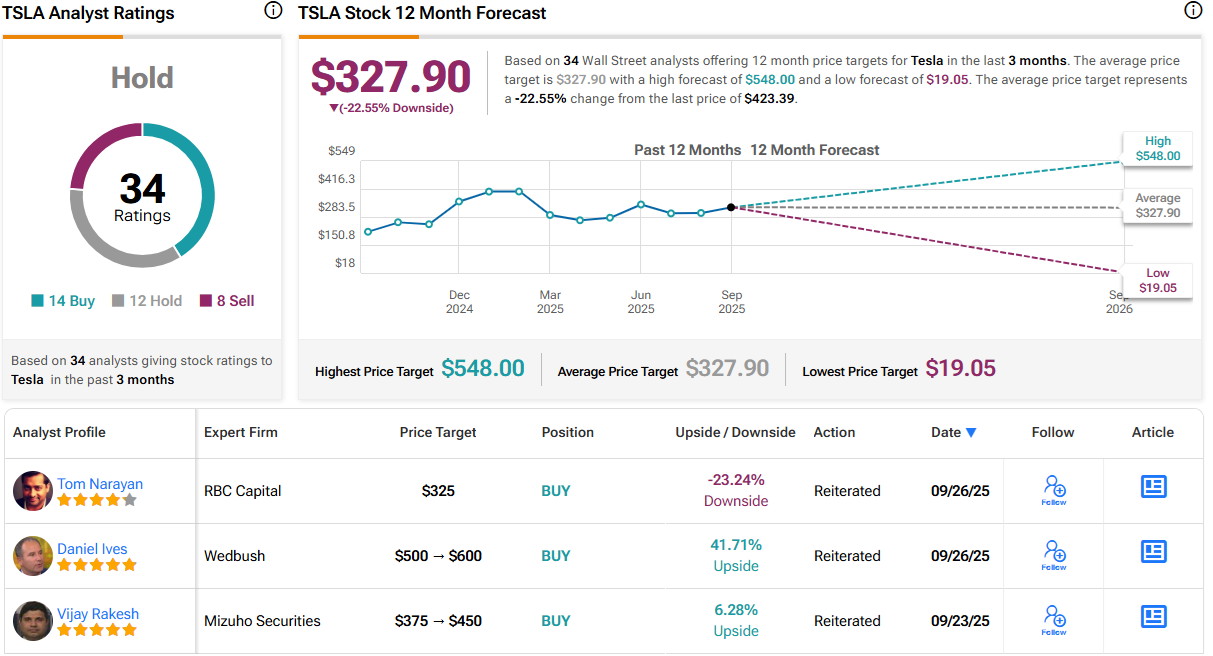

And with all of that to come, Ives has now raised his price target from $500 to a new Street-high of $600, suggesting the stock will gain 42% in the months ahead. Naturally, Ives’ rating stays an Outperform (i.e., Buy). (To watch Ives’ track record, click here)

That’s the bull case, but most on the Street are less enthusiastic. The stock only gets a Hold consensus rating, based on a mix of 12 Holds, 14 Buys and 8 Sells. Most also see it as overvalued; at $327.9, the average target factors in a one-year slide of 22.5%. (See Tesla stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.