The Q3 earnings season is now in full swing, and looking at the financial results so far, the news is pretty good.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

David Kostin, chief US equity strategist for Goldman Sachs, outlines the situation, and why it bodes well for investors: “3Q earnings season has kicked off, with the earliest reporting firms clearing the low bar set by consensus estimates. The largest Financials companies have now reported, and results generally exceeded expectations. Of the 66 companies that have reported 3Q results thus far, 50% of firms have surpassed consensus expectations by more than one standard deviation, compared with the long-term average of 48%.”

“We expect S&P 500 cash spending will grow by 8% in 2024 (to $3.6 trillion) and 11% in 2025 ($4.0 trillion) alongside strong earnings growth and a friendly macro backdrop,” Kostin further added.

Against this backdrop, we’ll be seeing some important earnings releases this week. Tesla (NASDAQ:TSLA), one of the ‘Magnificent 7’ tech mega-caps, and Boeing (NYSE:BA), one of the aerospace industry’s storied names, are both scheduled to report on Wednesday.

Goldman’s analysts are doing the background research on both stocks – and coming to a clear decision on which stock makes the better buy before the upcoming earnings releases. Let’s take a closer look.

Tesla

First, let’s look at Tesla, Elon Musk’s flagship company. Since its start in 2003, Tesla has become both the world leader in the development, marketing, and sales of electric vehicles (EVs), as well as the largest car company – of any stripe – in the global automotive market. Tesla boasts a market cap of $705 billion, a figure more than triple that of second-place Toyota and far ahead of any other EV company. We should note, however, that when counting by revenue Tesla does not crack the top ten among its peers and ranks 11th among the world’s automakers.

It’s not just sheer size, or even Musk’s notoriety, that makes Tesla special. The company is the only US electric car company to have reached profitability, and has been reporting consistently positive EPS since 2020. This success rides on the successful series of electric cars that the company has brought to the market, vehicles known for high-tech innovation, exciting performance stats, and luxury cachet in both styling and pricing.

Tesla’s production figures tell part of the story. In the third quarter of this year, the company built a total of 469,796 vehicles and made 462,890 deliveries. The bulk of these numbers reflected the popularity of the company’s Models 3 and Y cars, which accounted for 439,975 third-quarter deliveries, while Tesla’s other models totaled 22,915 deliveries. We should note, however, that these figures came in below expectations, a fact that reflects a recent trend of declining deliveries.

Declining deliveries are not the only headwind that Tesla has hit recently. On October 10, the company held its ‘We, Robot’ event, an event featuring the company’s ongoing development of autonomous vehicle and robot technology. While Tesla unveiled several cool products – including a robot bartender and a two-door ‘cybercab’ – the event as a whole underwhelmed observers. The new tech operated smoothly, but some was remote-controlled than fully autonomous, and there was a feeling that ‘We, Robot’ really showcased the fact that Tesla is still running well behind Google’s Waymo – which has already put autonomous taxis on the streets of San Francisco. We should note here that after the robotics event Tesla shares fell by 9%.

Looking ahead to the Q3 earnings report, the market expects that Tesla will report approximately $25.67 billion in revenue and a 60-cent non-GAAP EPS compared to last year’s respective $23.35 billion and 0.73. Tesla is scheduled to report its Q3 results on October 23.

For Goldman’s 5-star analyst Mark Delaney, Tesla presents something of a mixed picture. He believes that the company’s long-term prospects are sound – but also that its current valuation is maxed out. As he writes, “While we believe that Tesla can grow longer-term including with FSD [full self-driving, ed.], we believe headwinds in the auto business (e.g. a high degree of competition and pricing pressure in EVs) will limit the rate of its EPS growth in the near to intermediate term, we expect it will take time to grow its FSD/software business to a more meaningful level, and we believe valuation is full.”

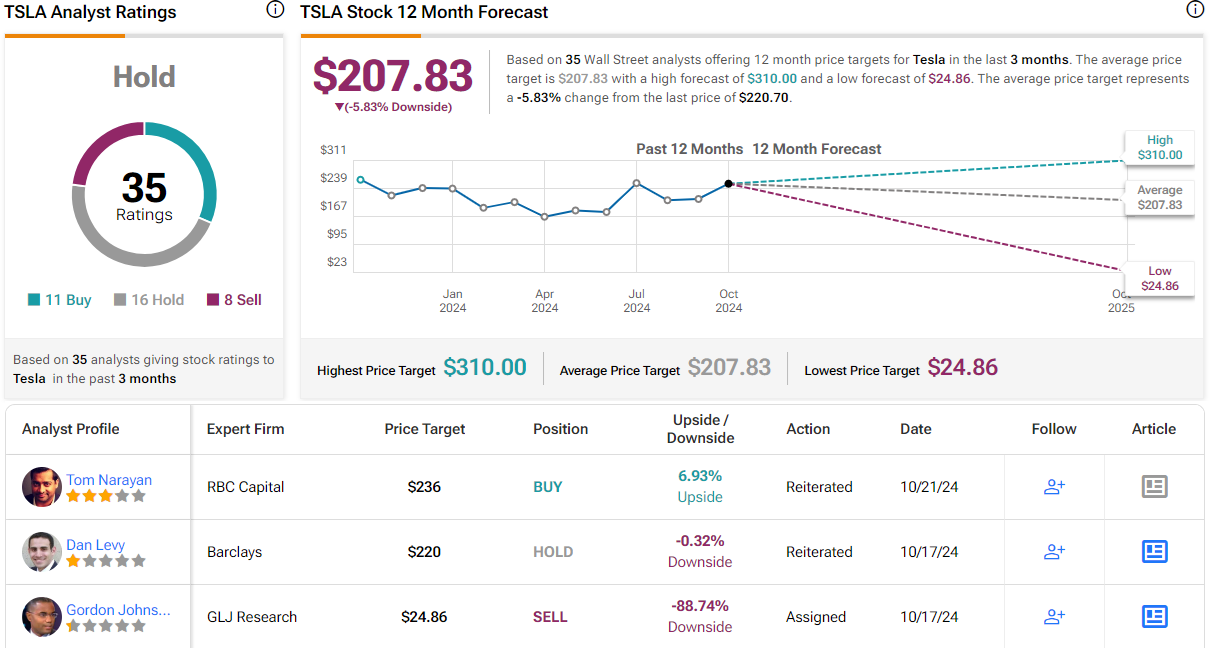

Delaney puts a Neutral rating on TSLA, along with a $230 price target that suggests a modest 4% gain for the shares in the next 12 months. (To watch Delaney’s track record, click here)

The overall Street view here is also cautious. The stock has a Hold consensus rating, based on 35 reviews that include 11 to Buy, 16 to Hold, and 8 to Sell. Shares in TSLA are priced at $220.70, and their average price target is $207.83 – implying that the stock may lose 6% of its valuation in the coming year. (See TSLA stock forecast)

Boeing Company

The second stock on our list, Boeing, has had plenty of recent headlines – and for all the wrong reasons. The storied aerospace firm saw its Starliner space capsule fail spectacularly when it malfunctioned while docked at the International Space Station – stranding two astronauts in orbit. While the company was able to successfully deorbit the Starliner without its crew aboard, the stranded astronauts will have to be brought back to Earth on Elon Musk’s SpaceX Crew Dragon spacecraft – and NASA has cleared the Starliner from the 2025 launch schedule.

The space program failure would have been bad enough for Boeing, but the company has also been plagued by a serious labor strike. The International Association of Machinists is striking against Boeing as labor and management strive to work out a new contract to bring the workers back to the job. This looks like it may happen, as the union membership is scheduled to vote on a new contract offer later this week.

These developments cap what’s been a difficult several years for Boeing. The company has faced aircraft groundings after a spate of crashes and in-flight accidents involving its popular 737 airliner series, and has also faced regulatory repercussions from the Federal Aviation Administration. It’s no wonder that BA shares are down by more than 40.5% so far for the year-to-date.

The picture is not completely bleak, however. Boeing remains one of the top two producers of commercial airliners in the world, second only to Airbus, and the company has so far this year delivered a total of 291 commercial passenger jets. Of that total, 229 were from the popular 737 series, reflecting the company’s success in meeting FAA regulatory oversight and safety requirements for the jet. Boeing had 116 commercial deliveries during Q3.

In addition, the company’s military operations remain on track. Boeing has several ongoing projects building and delivering military aircraft, and in the third quarter the company delivered a total of 34 new and remanufactured Apache helicopters, 10 F-15 fighter jets, and 10 KC-46 tanker aircraft. Despite all of its recent problems, the company’s commercial and military aircraft lines continue to provide Boeing with a sound foundation. And, last week, Boeing took preparatory steps to issuing new stock, a move that the company could use to raise as much as $10 billion in new capital.

Despite all its current issues, Goldman analyst Noah Poponak points out why investors should pay attention here. He says of the aerospace giant, “IAM workers at Boeing are on strike, though we expect a resolution soon, and for Boeing to be able to pick back up its aircraft production and delivery momentum. Deliveries the last few months have improved and September was tracking quite strong before the strike. The company faces a balance sheet question, and has suggested raising capital is possible given the importance of the credit rating… While BA continues to face several challenges to work through near-term, we see attractive valuation relative to long-term fundamentals.”

For Poponak, this all adds up to a Buy rating for BA, which he complements with a $200 price target indicating room for a 29% upside potential on the one-year horizon. (To watch Poponak’s track record, click here)

This is roughly in-line with the Street’s view of Boeing. The stock has a Moderate Buy consensus rating, derived from 21 recent analyst reviews that break down to 14 Buys, 5 Holds, and 2 Sells. BA stock is selling for $155 per share, and its $197.83 average target price implies a one-year upside potential of ~27.5%. (See Boeing stock forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.