Target Corporation (TGT) surprisingly delivered a bearish announcement on Tuesday, outlining efficiency and inventory challenges as matters that need to be resolved during its second quarter. The company has announced that it will take costly but necessary steps to ensure the firm gets back on track in the longer run.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

According to the firm’s Chairman and CEO, Brian Cornell: “The additional steps we are announcing today will ensure that we deliver for our guests while driving further growth. While these decisions will result in additional costs in the second quarter, we’re confident this rapid response will pay off for our business and our shareholders over time, resulting in improved profitability in the second half of the year and beyond.”

Based on the stock’s recent performance, investors are seemingly worried about Target’s prospects as this announcement comes only a few weeks after the company missed its earnings target by 87 cents per share amid rising input costs.

Much uncertainty remains in the air, but I’m bullish on the stock; here’s why.

Inventory Liquidation

Although no formal steps have been announced, it’s assumed that Target will utilize inventory liquidation methods to write down its aging inventory. Inventory liquidation means that Target will offload old inventory at a reduced cost, which could be unprofitable to the firm on a cash basis. However, if Target has already recognized the cost of the inventory it will liquidate, then it could, in fact, report excess profitability on an accrual basis.

In a nutshell, inventory liquidation is a temporary concern, and it’s nothing new. Additionally, the liquidation and cost recognition processes don’t always converge, meaning that it’s impossible to forecast the effect of the process on the firm’s second-quarter earnings report.

Potential Segment Support

The inventory liquidation process suggests that Target misjudged its consumer base’s strength. Nevertheless, the firm sells staple and affordable discretionary goods. Thus, Target is a non-cyclical firm.

To understand why staple goods will likely outperform other consumer segments, it’s necessary to observe the yield curve. The yield curve implies that interest rates could reach a surplus of 3%, which means that the economy will contract if the curve’s spot rates come to fruition. Thus, consumer staples as a non-cyclical segment will likely be the choice of many investors, as the segment could be one of few to sustain growth rates.

Input Costs

Input costs will likely wane, as rising interest rates will trigger wage elasticity as well as price elasticity of raw materials. Contrary to the belief of many, Target isn’t struggling to match its wage costs. In fact, the firm’s net income per employee ($13,020) currently exceeds its five-year average by 26.35%.

Furthermore, Target’s return on invested capital of 21.7% suggests that the firm holds an ultra-strong market position, allowing it to hold bargaining power over its suppliers. Thus, if anyone’s going to feel cost pressure, it would be Target’s upstream suppliers instead of the firm itself.

Valuation

Target’s stock is undervalued relative to its normalized five-year average. First of all, the stock’s price-to-earnings ratio suggests that it is trading at a discount worth 23.3%. In addition, Target’s forward PEG ratio of 0.74x implies that the stock’s forward earnings-per-share growth will likely be robust.

Lastly, Target’s price-sales ratio of 0.72x conveys that the market hasn’t yet priced the firm’s top-line earnings, leaving investors with a lucrative value gap.

Solid Dividend Prospects

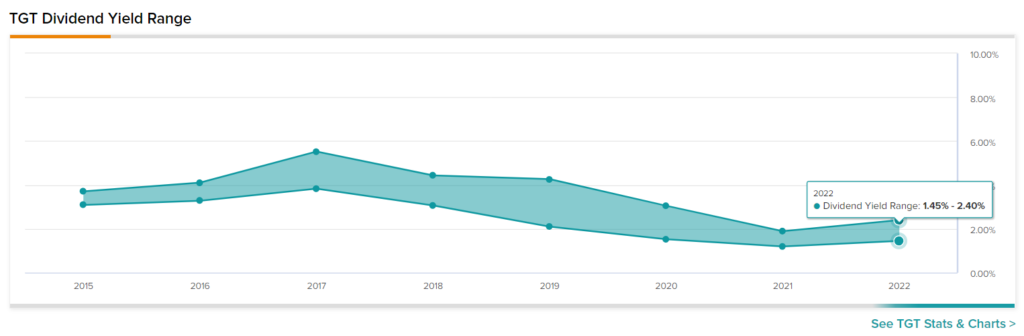

TipRanks’ dividend yield range tool shows that Target’s yield range sits between 1.45% to 2.40%, which is certainly very attractive. Target’s a respectable dividend stock that’s provided 13 straight years of payout growth. Moreover, the firm has the capacity to cover its dividend payments with relative ease as it boasts a dividend coverage ratio of 2.9x.

Wall Street’s Take

Turning to Wall Street, Target earns a Moderate Buy consensus rating based on 18 Buys and eight Hold ratings assigned in the past three months. The average TGT stock price target of $193 implies 23.7% upside potential.

The Bottom Line

Target presents an excellent “buy-the-dip” opportunity. The market’s overreaction to its recent earnings report and its inventory liquidation isn’t objective. Furthermore, Target could be one of the top performers during challenging economic circumstances, as non-cyclical consumer goods provide a risk-off option to investors.