Did you ever really like a stock, but the outlook is uncertain, and you can’t bring yourself to hit the Buy button? Before you pull the trigger on Taiwan Semiconductor Manufacturing (NYSE:TSM) stock, there are crucial factors that need to be carefully considered. Taiwan Semiconductor is an important company, no doubt, but I am neutral on TSM stock and don’t recommend taking action on it.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Taiwan Semiconductor Manufacturing is a behemoth among chipmakers. Hailing from Taiwan (of course), Taiwan Semiconductor manufactures over 90% of the world’s leading-edge computer chips, believe it or not.

As we delve into Taiwan Semiconductor’s valuation, dividend yield, and other considerations, you may be tempted to back up the truck and buy TSM stock immediately. However, there are a couple of known unknowns that should make prospective Taiwan Semiconductor investors think twice and delay any hasty trades.

The Bull Case for Taiwan Semiconductor Stock is Strong

First of all, Taiwan Semiconductor Manufacturing is a powerhouse among global semiconductor makers. If you’re an American stock trader and you only know about U.S.-based chipmakers, today’s a great day to conduct your due diligence on Taiwan Semiconductor.

The bull case for TSM stock grows even stronger when you look at the company’s valuation. It’s quite reasonable, as Taiwan Semiconductor’s GAAP-measured trailing 12-month price-to-earnings (P/E) ratio is 17.5x. That’s substantially lower than the sector median P/E ratio of 27.4x.

Next, passive-income investors should be glad to discover that Taiwan Semiconductor pays a forward annual dividend yield of 1.43%. That beats the technology sector’s average dividend yield of 1.025%. Also, not too long ago, Taiwan Semiconductor hiked its quarterly dividend payout by almost 17%.

Using TipRanks‘ data really helped me see the big picture with Taiwan Semiconductor. Glancing at the company’s earnings page, I found that Taiwan Semiconductor is not only consistently profitable but also has a good track record of beating quarterly consensus EPS estimates.

On top of all that, TD Cowen recently raised its price target on TSM stock from $85 to $95. According to TheFly, the TD Cowen analysts considered the possibility of Taiwan Semiconductor’s 2024 revenue growth being “second half weighted with a cyclical recovery in PC and mobile demand.”

Taiwan Semiconductor, Imminent Earnings, and the “Fog of War”

Whether a recovery in “PC and mobile demand” actually happens remains to be seen. Nevertheless, by this point you might already be highly enthused about Taiwan Semiconductor stock. That’s understandable, but you’ll definitely want to temper your excitement because there are uncertain factors to consider.

For one thing, Taiwan Semiconductor Manufacturing is expected to release its Q4-2023 financial results on January 18. Analysts expect the company to report quarterly EPS of $1.38, which would be higher than any of Taiwan Semiconductor’s three most recent quarterly EPS results.

A share price drawdown could ensue if Taiwan Semiconductor breaks its winning streak of EPS beats this time around. As the old saying goes, the bigger they are, the harder they fall.

Furthermore, there are geopolitical factors at work, and eager investors need to think about what’s known and what’s uncertain. What’s known right now is that Lai Ching-te of the Democratic Progressive Party was just re-elected as Taiwan’s president.

To put it in simple terms, China’s government wants to incorporate Taiwan as part of its “One China” policy/principle. In contrast, the Democratic Progressive Party is firmly opposed to Taiwan becoming part of China.

In other words, there’s probably going to be a lot of friction between China and Taiwan this year. This poses a potential problem for Taiwan Semiconductor, which operates two chipmaking plants in China.

China is currently an importer of chips from Taiwan. Richard Cronin of Washington-based think tank the Stimson Center explained, “China’s dependence on Taiwan to cover its chip deficit has been called its ‘Silicon shield.’”

However, that’s a precarious business relationship. It’s hard to tell how long that “shield” can withstand China’s alleged drone spying on Taiwan. Therefore, holding TSM stock in 2024 looks like a risky proposition.

Is TSM Stock a Buy, According to Analysts?

On TipRanks, TSM comes in as a Strong Buy based on three Buys and one Hold rating assigned by analysts in the past three months. The average Taiwan Semiconductor Manufacturing price target is $111.25, implying 9.9% upside potential.

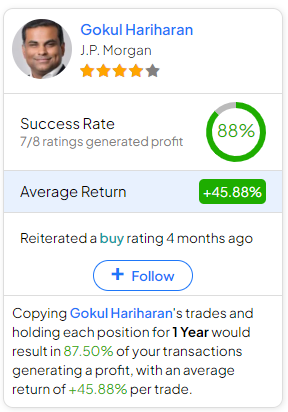

If you’re wondering which analyst you should follow if you want to buy and sell TSM stock, the most profitable analyst covering the stock (on a one-year timeframe) is Gokul Hariharan of JPMorgan Chase (NYSE:JPM), with an average return of 45.88% per rating and an 88% success rate. Click on the image below to learn more.

Conclusion: Should You Consider TSM Stock?

At first glance, Taiwan Semiconductor Manufacturing has everything that a smart investor could ask for — value, dividends, earnings beats, you name it. Frankly, Taiwan Semiconductor almost seems like a perfect investment.

Yet, there’s an imminent earnings event that could mar Taiwan Semiconductor Manufacturing’s track record of EPS beats. More consequentially and alarmingly, there’s tension between China and Taiwan that’s likely to persist for a while. With all of that in mind, I’m staying on the sidelines when it comes to TSM stock and am not considering any position at all.