The big news recently concerned the August jobs report, which came in below expectations. The softness in the jobs market spooked investors, and market watchers are now looking to the Fed’s next meeting, and an anticipated cut in the key funds rate.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

So, where does the stock market go from here? The overall trend of the past year remains bullish, and investors aren’t fleeing the market – yet. But the question remains, where should investors start putting their money? A recent report from Morgan Stanley’s chief US equity strategist, Mike Wilson, suggests buying stocks that show a combination of defensive positions and overall quality.

“Until the bond market starts to believe the Fed is no longer behind the curve (spread between 2-year yield and Fed Funds narrows), growth data reverses course and improves materially or additional policy stimulus is introduced, it will be difficult for equity markets to trade with a more risk on tone, in our view,” Wilson said. “This means valuations are likely to remain challenged for the overall index… In such an environment, quality + defensive equities should continue to show outperformance.”

The stock analysts at Morgan Stanley are following this lead, and pointing out solid defensive plays that should command investor attention going forward. We’ve used the database at TipRanks to look at the broader picture on two of these quality defensive stocks, so let’s take a dive into the details.

Johnson Controls (JCI)

We’ll start with Johnson Controls, maybe not a household name but a well-known player in the world of HVAC. Johnson Controls is a Fortune 500 name, boasts a market cap of almost $46 billion, and generated $26.8 billion in its fiscal year 2023, its most recent full fiscal year. The company has built its success on the basic necessity of the core service it provides: HVAC, fire control, and safety/security systems for commercial and office spaces.

Johnson Controls has been in business since 1885, when it was founded as an electric service provider. The company’s longevity is a distinct asset – this is a firm that knows how to adapt to changing times, and can show investors a long record of success. The company operates at a global scale, in more than 150 countries, and employs approximately 100,000 people. Johnson is known for integrating the latest technologies into its ‘smart building systems,’ including AI and machine learning, without forgetting the basics of the hands-on mechanical technology.

Earlier this summer, Johnson Controls made an important change, when it announced an agreement to sell off its Residential and Light Commercial HVAC business division. The buyer, Bosch, will acquire this segment of Johnson in a transaction valued at $8.1 billion; JCI’s consideration of the total comes to $6.7 billion. The move will turn Johnson Controls into a pure-play provider of ‘comprehensive solutions for commercial buildings.’

Also in July of this year, Johnson Controls announced the pending retirement of CEO George Oliver after 7 years in the position. Oliver will remain at the helm until a replacement chief executive is appointed, and will continue as chairman of the Board of Directors.

Turning to the financial side, we find that Johnson Controls reported a top line of $7.2 billion in its last quarter, fiscal 3Q24. This figure was up a modest 1% year-over-year, but missed the forecast by $140 million. At the bottom line, the company reported an EPS of $1.14 in non-GAAP measures, beating the estimates by 6 cents per share.

For Morgan Stanley analyst Chris Snyder, the key here is this company’s solid position in its niche, and a sound outlook going forward. As he writes, “JCI portfolio transformation brings attractive risk-reward as the company is now a pureplay provider of commercial building solutions (HVAC, Controls, Fire & Safety) – resulting in a more durable business and providing a re-rating opportunity. We see ~30% pro-forma service mix and increased exposure to industrial mega-trends (Data Center, US Reshoring) pushing the equity into a more premium comp group. While our math pegs pro-forma F’26 EPS L-MSD below existing operations, this can be offset with relatively minor cost take (~4% of divested sales). What’s left is largely unchanged EPS for a high-quality business while JCI equity continues to trade at 2-3 turn discount vs the peer group.”

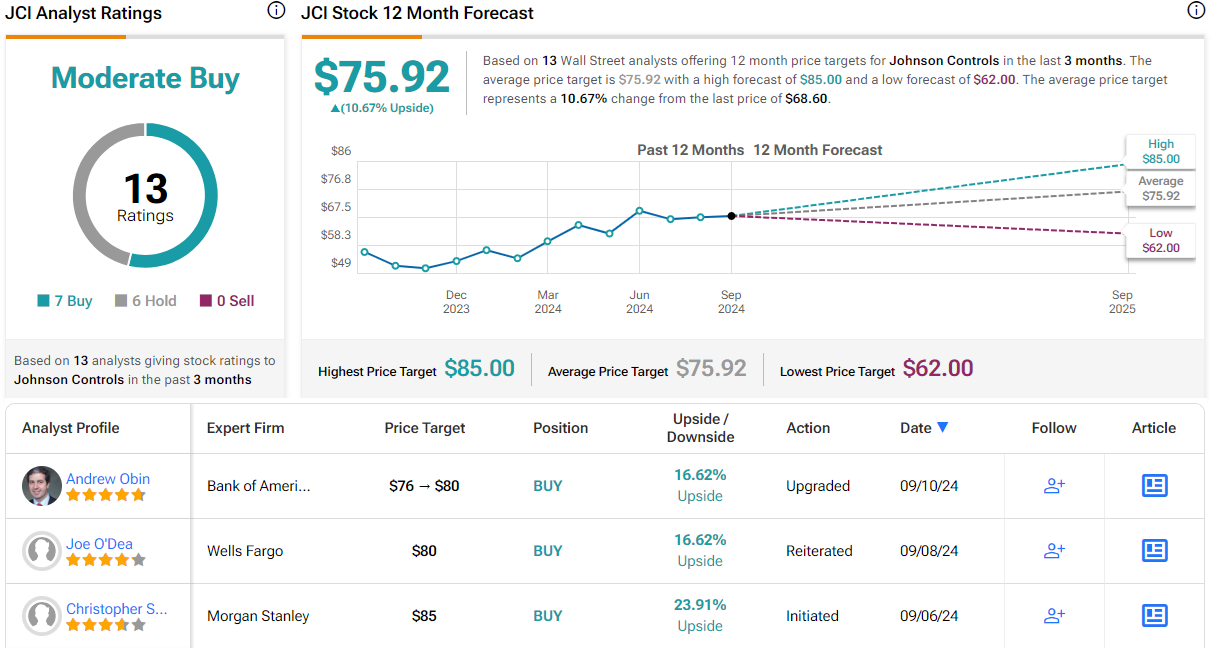

These comments support Snyder’s Overweight (Buy) rating on the stock, and his price target, of $85, indicates an upside of 24% for the year ahead. (To watch Snyder’s track record, click here)

This stock sports a Moderate Buy rating from the Street’s analysts, based on 13 reviews that include 7 Buys and 6 Holds. The shares are priced at $68.60 and the $75.92 average price target implies a one-year upside potential of almost 11%. (See JCI stock forecast)

General Dynamics (GD)

The second stock we’ll look at here is General Dynamics, an aerospace and technology manufacturing company – and one of the major defense contractors working in the US economy. General Dynamics was founded in 1893 and focused on the development of submarines as the Holland Torpedo Boat Company; it provided the Navy’s first modern subs as early as 1900. Since then, it has only grown. It provided 80 submarines for the US Navy during the Second World War, and expanded into the aerospace industry after the war. It changed its name to General Dynamics in 1952, and since then, it has built a reputation as an innovator, with a hand in the development of the F-111 strike aircraft and, later, developing and building the wildly successful F-16 fighter.

Today, General Dynamics operates through four business divisions: Aerospace, Marine Systems, Combat Systems, and Technologies. The company’s highest profile products today come from the Marine Systems division, where the Bath Iron Works and the Electric Boat segments produce, respectively, the Navy’s Arleigh Burke-class destroyers and its nuclear-powered submarines. In addition, the Aerospace division includes the famous Gulfstream jets.

In recent months, General Dynamics has secured several important contracts, showing how the company remains relevant to the defense industry. It started the month of August by announcing a $174 million contract for retrofit, repair, and support of the US Army’s Stryker vehicles, and followed this later in the month with a $1.32 billion contract modification that allows it to purchase ‘long lead time’ materials for the Virginia-class nuclear submarine program. And, in early September, GD secured a $491 million modification to an Air Force contract, for the Proliferated Warfighter Space Architecture Ground Management and Integration program, ongoing in Huntsville, Alabama and Grand Forks, North Dakota.

General Dynamics last reported earnings results for 2Q24, and in that quarter, top line revenues came to $12 billion – up 18% from the prior-year period and beating expectations by $500 million. The bottom line EPS figure of $3.26, while up more than 20% year-over-year, missed the forecast by 7 cents per share.

On the balance sheet, General Dynamics finished the quarter with $1.4 billion in cash on hand – after paying out $389 million in total dividends, repurchasing $34 million worth of stock, and investing $201 million in capital expenditures. Looking forward, the company can lean on a $91.3 billion work backlog.

Kristine Liwag, one of Morgan Stanley’s 5-star analysts, covers this defense giant, and in her coverage she notes that the company has plenty of strengths: “We see GD with a premier balance sheet and strong prospects for capital return upside. A refreshed line-up of new Gulfstream aircraft coupled with strong demand for GD’s defense products (e.g., ammo, ground vehicles) together present strong earnings growth potential… We see GD entering a unique period of margin acceleration.”

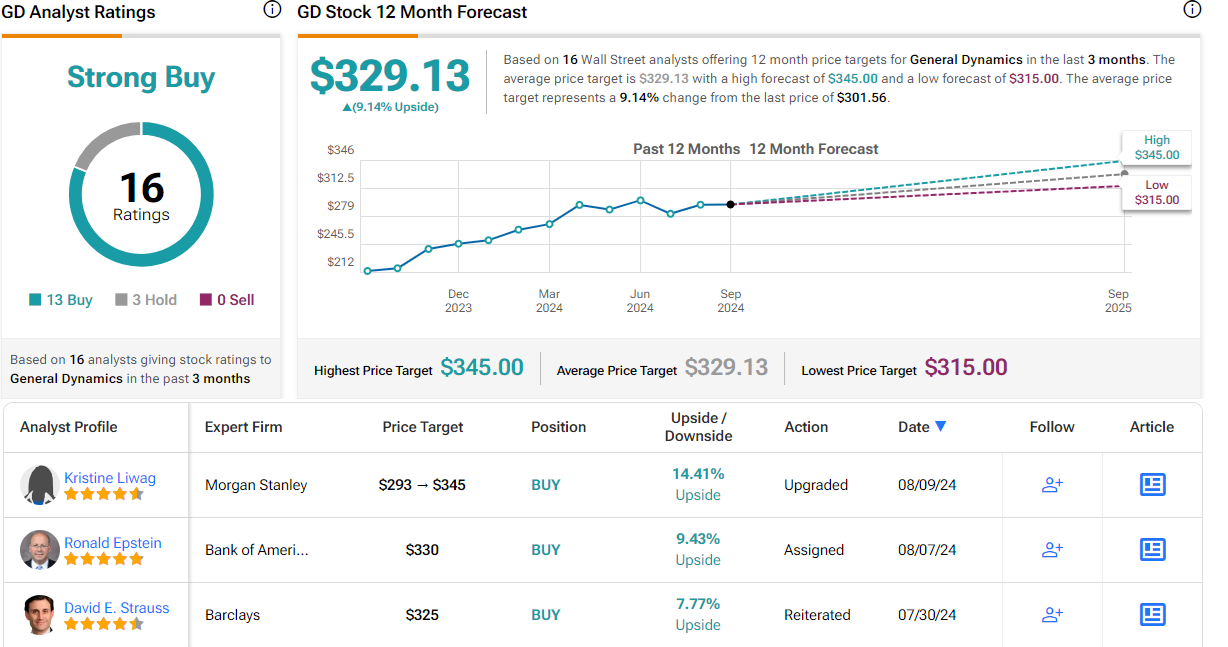

To quantify her stance, Liwag rates GD shares as Overweight (Buy), and her $345 price target indicates room for a 14.5% gain in the next 12 months. (To watch Liwag’s track record, click here)

This stock has earned a Strong Buy consensus rating from the analysts, with the 16 recent recommendations breaking down to 13 Buys and 3 Holds. The stock’s $301.56 trading price and $329.13 average target price together suggest an upside of 9% by this time next year. (See GD stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.