The wait is finally over for Palantir (NYSE:PLTR). Following several delays, last week, England’s National Health System (NHS) made an official announcement that a seven-year contract worth £330 million (~$415 million) for its new Federated Data Platform (FDP) had been awarded to a group led by Palantir with 4 other firms – Accenture, PwC, NECS, and Carnall Farrar – all acting as support.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The objective of the new platform is to integrate disparate NHS data from various systems, enhancing overall organizational visibility, minimizing wait times and delays, and facilitating quicker diagnoses. The NHS anticipates an investment of at least £25.6 million (~$32 million) over the first year, with the rollout of some new software slated for the upcoming spring.

Palantir, having previously collaborated with the NHS on the COVID-19 data store and vaccination program through a nominal £1 contract, recently secured a 12-month £25 million contract to transition its ongoing work with the NHS to the future FDP, a project currently in development by Palantir and its partners.

As it amounts to a major piece of new business and further increases its government work beyond the defense and intelligence sectors, Deutsche Bank analyst Brad Zelnick thinks the contract is a “net positive for Palantir.”

However, shares trended lower following the announcement and considering the finer details of the agreement that is not much of a surprise. “The announcement is likely viewed as a modest disappointment to investors given the presumed single contract had previously been pegged at £480m (~$600m) over five years and it was unclear that multiple other GSI partners would be sharing in the work,” the 5-star analyst explained. “Note, Palantir will still be able to bid on additional procurement for the platform, and as we’ve often seen with government contracts, these can potentially be expanded upon over time.”

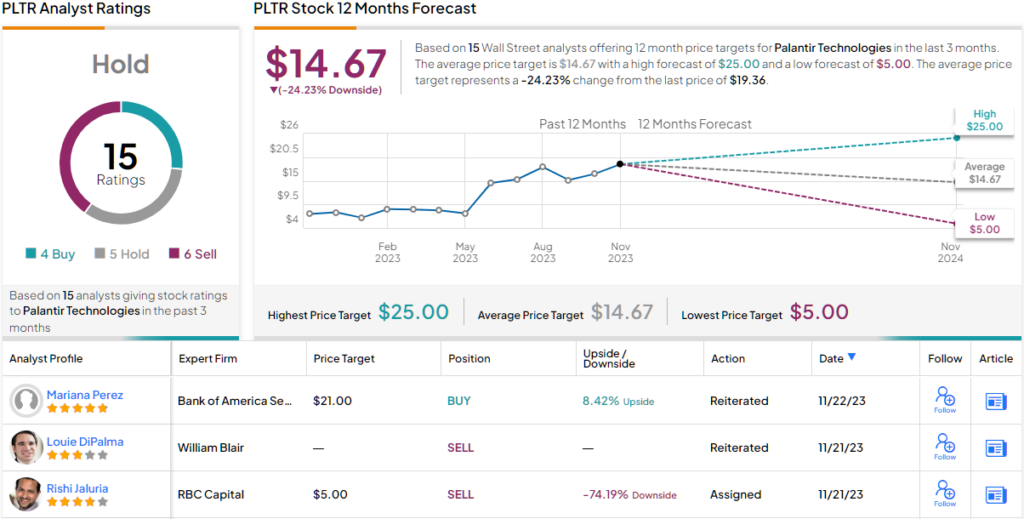

Nevertheless, that is not enough for Zelnick to change his Palantir stance. Accordingly, struggling to see a “clear line of sight” to the substantial overall acceleration required to justify its current valuation, Zelnick maintained a Sell rating on the stock, backed by an $11 price target. It’s a sharp 43% drop from current levels to reach Zelnick’s objective. (To watch Zelnick’s track record, click here)

The rest of the Street’s take is only marginally better. Based on a mix of 4 Buys, 5 Holds and 6 Sells, the stock claims a Hold consensus rating. A year from now, shares are expected to change hands for ~24% discount, considering the average target stands at $14.67. (See Palantir stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.