Last week we heard comments from Federal Reserve chair Jerome Powell, and in his remarks, he indicated that the Fed is likely to start paring back interest rates, perhaps as soon as next month. The conventional wisdom is predicting two 25-basis point cuts by year’s end.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The prospect of rate cuts is undeniably positive for the stock markets overall, but it’s particularly favorable for consumer stocks. Lower rates translate to cheaper credit and increased liquidity, both of which support consumer spending.

Covering the consumer sector for Piper Sandler, analyst Anna Andreeva has an interesting take on the segment. She writes, “We believe investors should pick their spots within discretionary given an episodic consumer, ongoing consolidation of spend toward non-discretionary and shift from goods to services, plus, in addition to well-articulated pressures on the lower income consumer, higher income demand appears to be more selective as well. Our framework is based on: 1) greatest possibility of estimate revisions against expectations; 2) channel checks and intra quarter data points; 3) valuation and buy-side sentiment.”

Andreeva goes on to recommend several consumer stocks as Buys for the coming months. We’ll zoom in on the details of two of her choices, consumer names that she identifies as ‘top picks.’ Here are the details on them, using data drawn from the TipRanks platform as well as comments from Andreeva’s recent note.

Chewy (CHWY)

We’ll start in the pet supply niche, a niche we don’t often think about but one that carries high potential. According to a recent study by Forbes, Americans spent $136.8 billion on their pets as recently as 2022 – and that number was up 11% from the prior year. The same study also showed that 66% of all US households – a total of 86.9 million – owned a pet, with the large majority of those household pets being dogs and cats. In 1988, the percentage of pet-owning households stood at 56%.

Chewy, which is working to make itself the most trusted destination for pet owners, operates primarily as an online retailer. The company offers a wide variety of the goods and services needed in a pet-friendly home, including food, toys, treats, and even prescription veterinary medications or pet insurance coverage. These products are available for our ubiquitous dogs and cats, of course, but also for birds, small mammals, reptiles, and even the non-pet animals that depend on us: the livestock and working animals on our farms.

In addition to its online retail business, Chewy also opened a network of brick-and-mortar veterinary clinics. The company currently has clinics in Atlanta, Denver, and South Florida, and offers wellness visits, emergency care, surgical services, and membership plans. Chewy has plans to continue expanding its vet clinic network.

Earlier this week, the company released its fiscal Q2 earnings, with the print showing a beat on the bottom-line, as adj. EPS of $0.24 outpaced expectations by $0.03. The top line came to $2.86 billion, up 2.6% year-over-year and in-line with the estimates.

For Piper Sandler’s Andreeva, the key to this stock lies in ‘pet trends,’ and the overall data on pet ownership in the US is supportive. Andreeva writes, “While topline trends are likely still muted, CHWY appears to be at profitability inflection aided by both gross margin expansion (sponsored ads, mix shift to higher margin revenue streams, well controlled discounting) and SG&A leverage (automation and efficiency gains). Net ads under pressure for six quarters has been the #1 thesis of the bear case on the stock—while it’s too early to tell if new pet adoption trends have meaningfully stabilized, our pet survey work suggests interest picking up. Any degree of positive new pet formation trends for a category leader in pet would be constructive for the stock.”

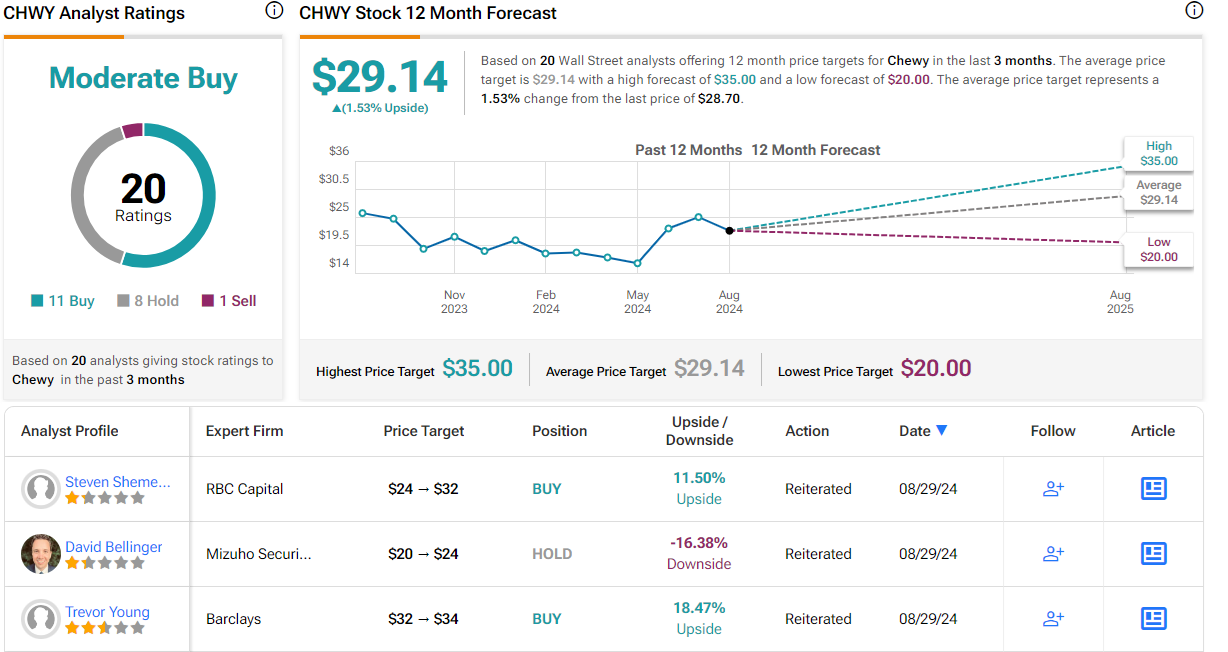

The analyst rates CHWY as Overweight (i.e. Buy), while her $35 price target implies a one-year upside potential of 20.5%. (To watch Andreeva’s track record, click here)

That Piper Sandler stance is more bullish than the overall Street view. CHWY shares have a Moderate Buy consensus rating, based on 20 reviews that include 11 to Buy, 8 to Hold, and 1 to Sell. The shares are selling for $28.70 and the $29.14 average price target suggests the shares will stay rangebound for the time being. (See Chewy stock forecast)

Wolverine World Wide (WWW)

The second Piper Sandler pick is a footwear company, the west Michigan-based Wolverine World Wide. The company is best known for its eponymous Wolverine boots and shoes, but it also owns such well-known brands as Hush Puppies, Saucony, and Stride Rite, and is the licensed manufacturer and distributor of Cat Footwear and Harley-Davidson Footwear. The company has a strong bent toward heavy-duty work shoes and boots, is known for quality, and boasts that its products are found in more than 170 countries around the world.

In recent years, the company has focused on restructuring its business to streamline operations. In 2019, the company split itself into two operating segments, the Michigan Group and Boston Group, and in the past year, it has divested itself of two brands, Keds and Sperry. In addition, in 2021, Wolverine acquired the British-based activewear and lifestyle brand Sweaty Betty.

The company’s restructuring has coincided with several consecutive quarters of falling revenues, although that trend reversed in the most recent readout. In, 2Q24, Wolverine reported a year-over-year decline of 27.8% at the top line, for a total of $425.2 million, although that represented a sequential improvement of ~7.5% while the figure beat the estimates by nearly $15 million. At the bottom line, Wolverine reported earnings of 15 cents per share by non-GAAP measures, beating the estimates by 4 cents per share.

The earning beats form an important note in Andreeva’s take on Wolverine’s stock. She notes that the company’s streamlining has carried it through a difficult period, but predicts stronger results going forward.

“We think the algo of MSD sales growth, EBIT margin recapture and FCF deployment towards debt repayment/share repurchases driving 20% EPS growth into ‘25 and beyond is underappreciated at 10-11x P/E. For the past three quarters, WWW beat top-line consensus expectations by 4% but Adj. EBITDA/EPS by 100%+/over 300%, respectively, and we expect earnings upside to drive multiple expansion,” Andreeva opined.

These comments support Andreeva’s Overweight (i.e. Buy) rating on the stock, and her $18 price target points toward a gain of 30.5% on the one-year horizon.

Overall, WWW shares have picked up a Moderate Buy from the analyst consensus, based on 7 recent reviews that include 2 Buys and 5 Holds. The shares are priced at $13.79 and the $13.67 average target price implies they are currently fully valued. (See WWW stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.