As we usher in 2024, the economic landscape is showing signs of improvement. The rate of inflation is gradually stabilizing, and the Federal Reserve has hinted at the possibility of future rate cuts. However, it’s important to note that this optimistic outlook is not evenly distributed, and some market sectors are still facing uncertainties.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Energy is usually a no-brainer, featuring a combination of essential service and reliable dividends that always attract investors. Looking ahead in this new year, however, Mizuho analyst Nitin Kumar has taken a deep dive into the hydrocarbon scene, and he sees ‘limited upside’ to commodity prices. Noting that energy stocks are closely correlated with those commodity prices, Kumar advises caution for investors.

“Although the post-pandemic recovery in oil demand continues to play out and physical market balances remain tight, the level of OPEC+ support and non-OPEC supply growth (including US) suggests global oil markets have limited upside in 2024 (albeit limited downside as well). Meanwhile, US natural gas supply remains resilient despite stronger (ex-weather) domestic demand, and LNG export demand seems to be delayed until late 2024/early 2025. With commodity prices likely trading sideways in 2024, we believe investors should focus on stocks that can create their own catalyst – either through the asset base or through extraordinarily low balance sheet leverage,” 5-star analyst opined.

But which stocks should those be? Kumar has identified two names that demonstrate resilience in the face of these headwinds. Interestingly, Kumar’s confidence is widely echoed. According to TipRanks database, both of these stocks have garnered unanimous ‘Strong Buy’ ratings from the consensus of analysts. Let’s take a closer look.

Civitas Resources (CIVI)

We’ll start with Civitas Resources, an energy company that is a leader in hydrocarbon production – and in making sustainable oil and gas operations. Civitas has productive oil and gas assets in both Colorado and Texas, and is the first net carbon-neutral production firm in the state of Colorado. Civitas aims to become the first such producer in Texas by the end of this year.

When it comes to productive assets, Civitas’ operations are focused mainly in the Denver-Julesburg (DJ) basin in Colorado. At the end of 2023, the company had 470,000 net acres in the DJ, while in Texas, it claimed holdings of 70,000 net acres in the rich Permian basin. Together, these asset groups generated 280,000 Boe/d in total production.

In the company’s first news announcement of 2024, on January 2, Civitas gave notice that it had closed its acquisition of certain Vencer Energy assets in the Midland basin formation in Texas. These assets include known production of both oil and gas, and going forward will materially strengthen Civitas’ position in the Texas oil patch. Per the agreement, Civitas made a $550 million cash payment to Vencer on January 3; the company has already paid $1 billion in cash and issued 7,181,527 shares of common stock to Vencer.

Civitas has access to the financial resources to back this transaction. At the end of 3Q23, the last reported, the company had $1.3 billion in liquid assets on hand, in both cash and available credit, and had generated $205.6 million in free cash flow during the quarter.

The cash position was derived from Civitas’ $1.04 billion in total revenues for Q3, a top line that was up 4% year-over-year and $30 million ahead of the forecast. However, the company’s net income, reported as GAAP EPS of $1.56, was 95 cents per share below expectations.

For investors, Civitas offers an attractive capital return proposition. The company regularly distributes both a fixed and a variable dividend. The most recent dividend payment, distributed on December 29, amounted to a combined $1.59 per common share, with $1.09 attributed to the variable component. On an annualized basis, this translates to a generous $6.36 per share dividend, yielding an impressive 9.5%.

In his write-up on Civitas, Mizuho’s Kumar starts with a look at the company’s expansion activities, writing, “2023 marked a transformative year for CIVI, with three significant basin-entry acquisitions into the Permian which reshaped its asset base (now roughly balanced between the Permian and DJ Basin) and extended its inventory duration (albeit at ~10 years, still light vs. peers). Initial execution as a pro forma company demonstrated in 3Q23 should give investors additional confidence in CIVI’s ability to fully integrate the acquired assets into 2024, where we also see upside bias to its initial outlook.”

He goes on to point out the company’s strong capital return program, and its potential for the near future: “Cash returns rank among the strongest in the sector, with CIVI offering a compelling … payout yield for 2024e. On our revised price deck, we have CIVI shares trading at a steep discount to SMID-cap peers on both FCF/EV and EV/EBITDX, too wide a valuation gap in our view considering the vastly improved asset base and expanded inventory duration.”

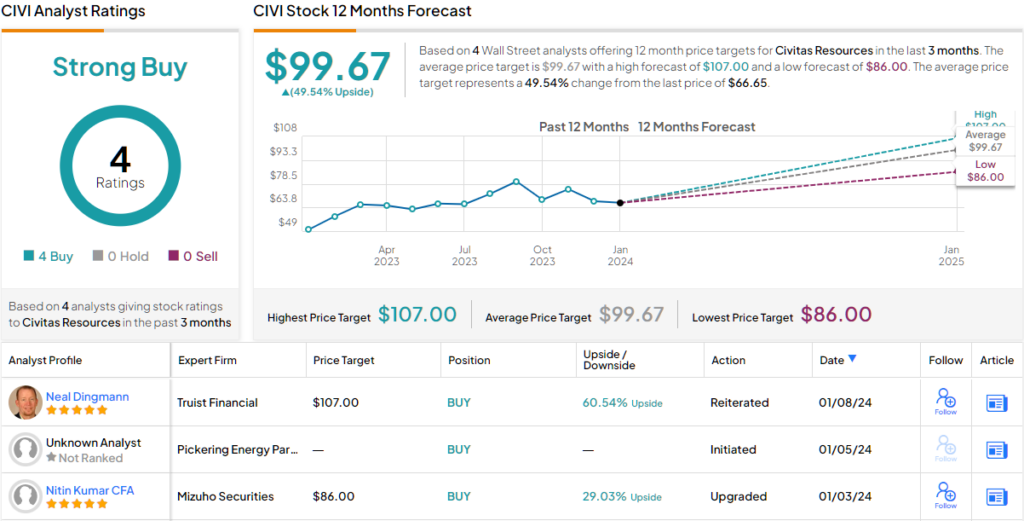

These comments combine to support Kumar’s Buy rating on CIVI stock, while his $86 price target implies the shares will gain 29% over the course of 2024. (To watch Kumar’s track record, click here)

The Strong Buy consensus rating on CIVI is unanimous, based on 6 recent positive analyst reviews. The shares are trading for $66.65, and their $99.67 average price target implies ~50% upside potential on the one-year time horizon. (See CIVI stock forecast)

Matador Resources Company (MTDR)

Next on our list is Matador Resources, another hydrocarbon operator working in Texas. Matador’s focus is on natural gas, particularly unconventional plays. The company has active gas drilling operations in the Texas-New Mexico Delaware basin, in the South Texas Eagle Ford formation, and in Louisiana’s Haynesville and Cotton Valley formations. Supporting these operations, Matador works with a set of active midstream assets, including gathering and processing services for natural gas, crude oil transport, gathering activities for both crude oil and produced water, and third-party produced water disposal.

Matador released its last production update this past November, an update that included results from 21 wells which the company acquired from Advance Energy Partners Holdings in April of last year. The new wells are located in Matador’s New Mexico Ranger asset area and make up the largest single-batch development project the company has ever put into operation. Matador’s production totaled 135,000 Boe per day during 3Q23.

In addition to the boost in production from the new wells, Matador also announced that its lenders have authorized an increase of $50 million in the company’s revolving credit facility. The new upper limit is $535 million.

The company’s strong production numbers lend support to its solid credit – and to its revenue and earnings numbers. Matador reported a topline of $772.3 million in 3Q23; while down some 8% year-over-year, that figure beat the forecast by over $70 million. At the bottom line, Matador’s non-GAAP earnings were reported as an EPS of $1.86; this was down 30% year-over-year but came in 21 cents better than had been anticipated. The company reported an adjusted free cash flow of $144.6 million in the quarter.

All of this caught Nitin Kumar’s attention. The top-ranked analyst noted Matador’s productive business model and its expanding assets as particularly attractive for investors. In Kumar’s words, “MTDR has pursued a differentiated strategy within the E&P sector, with a priority on measured production growth in favor of formulaic cash payouts to shareholders. Capital efficiencies demonstrated to date and strong initial results from the recently-acquired Advance assets position MTDR with solid operational momentum heading into 2024, where we see a differentiated upstream profile… MTDR trades at a premium to peers on 2024e FCF/EV but in-line on 2025e, presenting an attractive valuation in our view given its differentiated growth strategy, recent operational momentum, and above-average inventory depth.”

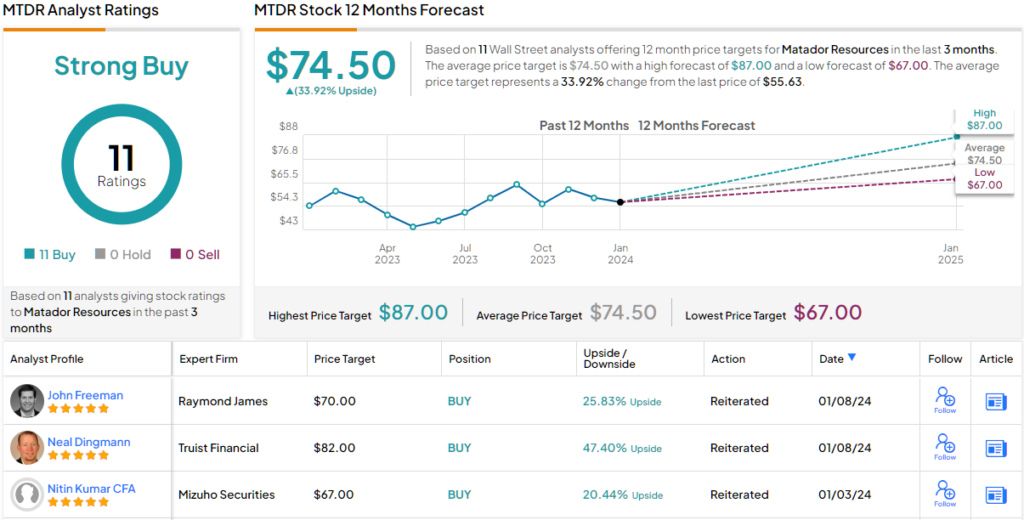

Looking forward, Kumar gives MTDR shares a Buy rating, with a $67 price target that indicates a 20% gain in store for the stock in the next 12 months.

Overall, Matador has 11 unanimously positive analyst reviews to back up its Strong Buy consensus rating, while the $74.50 average target price suggests a 34% increase from the $55.63 current trading price. (See Matador stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.