Starbucks (NASDAQ:SBUX) stock is warming up again after many years of rollercoaster-like ups and downs. For its fiscal fourth quarter, Starbucks not only blew away the estimates (global sales surged 11%, even as prices rose) but also served up a “Triple Shot Reinvention” strategy that includes several growth pathways.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Undoubtedly, there were numerous concerns that Starbucks’ growth profile would cool at the hands of a troubled domestic and Chinese economy. After such a strong quarter in the books and more light shed on its growth plans, it may very well be time to order up a venti-sized position in the stock as Starbucks stays resilient en route to greater growth.

Further, CEO Laxman Narasimhan looks capable enough to take the company to new levels. As such, I’m staying bullish on the name, as its new strategy is likely to also take SBUX stock to new heights.

Starbucks Stock is Starting to Feel Caffeinated Again. Thank the Triple Shot Strategy

As a part of the Triple Shot Reinvention plan, Starbucks aims to restore the power of the brand (it’s lost a bit of its luster in recent years), improve its digital presence, and ramp up its global store expansion. If Starbucks can deliver in the three key areas it outlined, I do not doubt that Starbucks stock will be more deserving of a higher multiple again.

At writing, shares of Starbucks trade at 28.6 times trailing price-to-earnings (P/E) — arguably a solid multiple for a growth stock. However, given that the multiple isn’t a heck of a lot higher than the likes of restaurant plays lacking on the growth front — think Yum! Brands (NYSE:YUM), which goes for nearly 24 times trailing P/E — I’d argue Starbucks ought to be worth north of 30 times P/E once again. Don’t forget — Starbucks stock has averaged a trailing GAAP P/E multiple closer to 50 times over the last five years.

Of course, we must give Mr. Laxman enough time to execute Starbucks’ new plan as we enter a potentially rough environment for the consumer. Even if we are in for a hard landing for the economy in 2024, don’t expect Starbucks to gravitate off its new strategic growth pathway. After all, it’s a longer-term, multi-year plan that could bring the magic back to the Seattle-based coffee chain.

Starbucks’ Global Expansion Could Be Its Biggest Growth Driver

I’m a pretty big fan of Starbucks’ new plan, as are many investors who bid up the stock post-earnings. That said, the firm’s most critical growth driver, I believe, is its ability to expand internationally. Arguably, Starbucks already has a powerful brand. Plus, its digital presence is already the envy of many players in the industry.

Though many chains have attempted to replicate the success of Starbucks’ loyalty app, none quite hit the spot as well as Starbucks. There’s a reason the company put its software-as-a-service (SaaS) hat on by offering its mobile tech back in 2019.

As a part of the Triple Shot global expansion plan, Starbucks aims to accelerate its efforts to operate as many as 55,000 locations by 2030. Undoubtedly, the Chinese market is paramount to Starbucks’ long-term expansion efforts. The Chinese economy may be in a rut right now, but it won’t be forever. As Starbucks continues expanding, even in the bad times, it will set the stage for incredible growth at some point down the road once the next bull market is ready to kick into high gear.

The company is aiming to grow its Chinese store count to 9,000 by 2025’s end. And that’s just one milestone, according to Mr. Laxman.

Of course, increasing the pace of new store openings will not come cheap, especially in a high-rate world. On the efficiency side, Starbucks hopes to save $3 billion in three years. Indeed, automation could play a big part in helping save the firm costs over the long run, as I described in a prior piece.

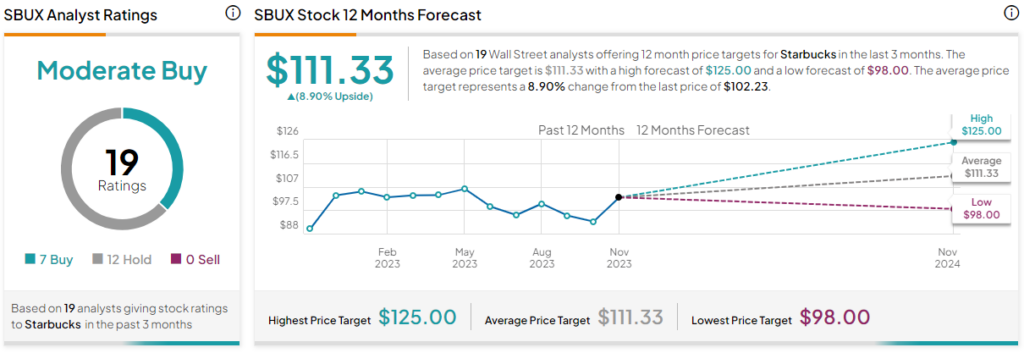

Is SBUX Stock a Buy, According to Analysts?

According to analysts, SBUX stock comes in as a Moderate Buy. Out of 19 analyst ratings, there are seven Buys and 12 Hold recommendations. The average Starbucks stock price target is $111.33, implying upside potential of 8.9%. Analyst price targets range from a low of $98.00 per share to a high of $125.00 per share.

The Bottom Line on Starbucks

Starbucks is back on the right track, with a new Triple Shot Reinvention plan and a very smart CEO who has what it takes to bring out the best in the firm. It’s been a rocky past few years, but Starbucks seems poised to finally move on as it puts its foot on the gas.