It’s been a year of relief for most mature technology stocks, with most of the year’s recovery momentum concentrated on mega-cap tech (think the Magnificent Seven stocks). Still, another class of recovering tech stocks may have more room to run as they begin to pick up traction, many months after mega-cap tech led the upward charge. Some of the higher-growth tech firms — like SQ, INTU, and DKNG — were punished more severely in 2022 and have still yet to recover most of the ground lost.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

The following companies may have greater sensitivity to higher rates due to their high price-to-earnings (P/E) multiples or lack thereof. In any case, as rates begin to reverse as they have in recent weeks, I’d look for the more aggressive high-growth tech companies to potentially kick off the next leg of the market rally.

It’s the Cathie-Wood-esque growth stocks that may be next up to the plate as the market looks for a new group to lead the pack. Therefore, in this piece, we’ll check out TipRanks’ Comparison Tool to have a closer look at the three intriguing high-growth plays mentioned above that Wall Street continues to view in high regard.

Block (NASDAQ:SQ)

Block, formerly Square, is the fintech pure-play run by the legendary Jack Dorsey. The stock got crushed in the past two years, shedding more than 85% of its value from its 2021 peak to its recent October 2023 trough.

Undoubtedly, the headwind of high rates has weighed on SQ quite heavily, as has a rise in competition in the digital wallet and payment space. In a prior piece, I highlighted that the userbase (and network effects) over at Cash App was a major reason to hang onto the stock, even if the firm didn’t have anything to set itself apart from the pack in the fintech scene quite yet.

With various crypto project wild cards and a decent quarterly earnings beat in the books, I think there’s no better time than to go bargain-hunting for SQ stock, especially if you’re in the belief that rates on the 10-year U.S. Treasury note have peaked. Though there aren’t too many catalysts that could propel a sustained rally, I am bullish due to SQ’s low valuation and the potential value that Block can unlock in its payments ecosystem.

Just last week, Block posted some respectable revenue and earnings numbers, beating on both fronts, thanks to Cash App and Square. The stock finished up over 10% the day after the earnings report, which also included a guidance raise (gross profit of $1.96-1.98 billion expected for Q4) and a $1 billion share repurchase plan.

Though Block may be lacking in any catalysts, there’s a lot of intriguing innovation going on behind the scenes. Dorsey acknowledged his firm has been “quiet lately” due to its focus.

Indeed, Dorsey and the company have been flying under the radar of late. However, it may be a mistake to discount the potential for new features and innovations to help drive quarterly growth from here. With such a low bar after the stock’s multi-year sag, I’d not be shocked if Block stock is in for another few post-earnings pops as the economy gradually recovers over the next three years.

Block may lack a trailing price-to-earnings multiple for now, but it’s on the right track. Currently, shares go for just north of 18 times next year’s expected P/E. The Cash App and Square userbases alone, I believe, warrant a much higher multiple.

What is the Price Target for SQ Stock?

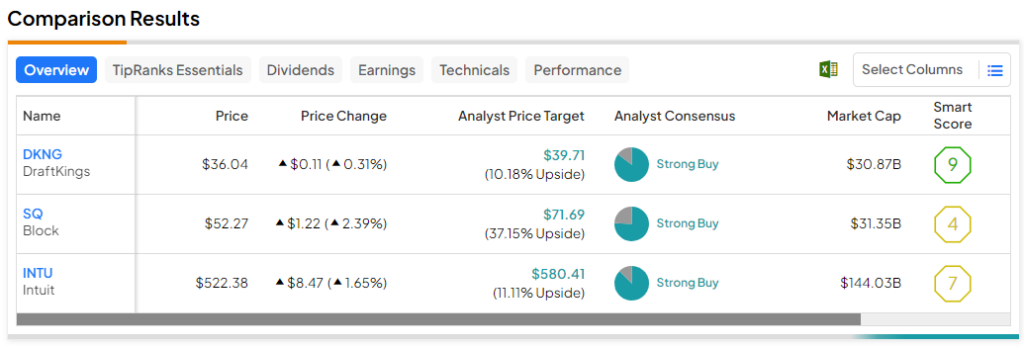

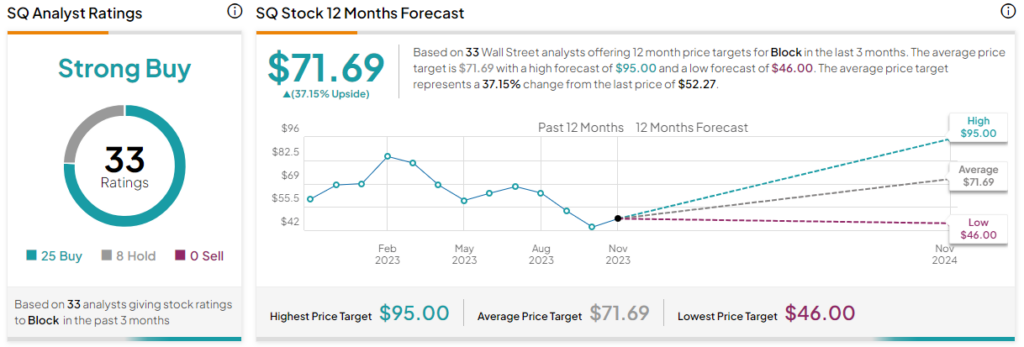

Block has a Strong Buy consensus rating, with 25 Buys and eight Holds assigned by analysts in the past three months. The average SQ stock price target of $71.69 entails 37.2% upside potential from current levels.

DraftKings (NASDAQ:DKNG)

DraftKings is another 2021-22 loser that’s been a huge winner so far this year, with shares now up 225% year-to-date. The company recently reported an incredible third quarter alongside increased guidance. Sales soared an impressive 57% to $790 million, while the firm added a whopping 2.3 million monthly unique players for the quarter. There’s an online betting boom, and DraftKings has front-row floor seats to it.

It’s been just two weeks since my last DKNG piece, where I shed light on the stock’s +30% upside potential. Fast forward to today, and shares are up around 32%, and the analyst upgrades have continued to flow in over the past few weeks.

Hats off to Morgan Stanley’s Stephen Grambling, who said to buy the stock ahead of earnings. Though the stakes are that much higher post-earnings, I still view ample upside to be had in the stock for longer-term investors seeking to capitalize on the digital gaming boom.

Given its impressive brand and marketing campaigns, I view DraftKings as a firm that can not only capitalize on the boom in online sports betting but take market share away from other rivals. It’s a crowded space to be in right now, but DraftKings stands out as a king among men after its impressive quarterly beat.

What is the Price Target for DKNG Stock?

DraftKings is a Strong Buy, according to analysts, with 23 Buys and four Holds assigned in the past three months. The average DKNG stock price target of $39.71 implies a 10.2% gain from here within the next 12 months.

Intuit (NASDAQ:INTU)

Intuit is a mature $146 billion financial software giant that has also begun to pick up traction this year. Shares are up over 33%, and they could end 2023 even higher as the firm looks to incorporate new innovations in its QuickBooks accounting software. Indeed, generative artificial intelligence (AI) is a huge growth lever that could help grant Intuit a leading spot in the so-called AI race.

Undoubtedly, small-business accounting is an arena that could be made a heck of a lot less stressful with the help of a tailored chatbot. According to Nhung Ho, Intuit’s VP of AI (yes, Intuit has a VP of AI), its AI assistant not only aims to make its users “more money with less work” but also give them “complete confidence.” Indeed, confidence in accurate results is key. In that regard, I think Intuit is hitting the nail on the head.

Given Intuit’s AI potential and its commitment to improving the lives of its small-business clients, I am bullish and view the seemingly rich 59.5 times trailing P/E multiple as not rich enough.

What is the Price Target for INTU Stock?

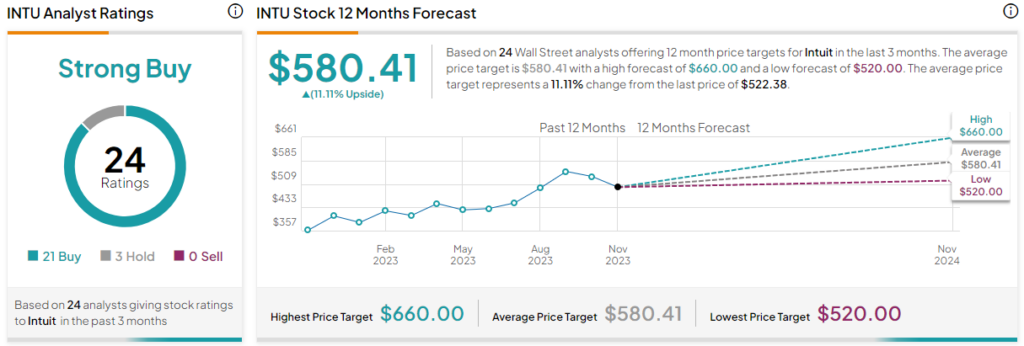

Intuit is a Strong Buy, according to analysts, with 21 Buys and three Hold ratings assigned in the past three months. The average INTU stock price target of $580.41 implies 11.1% upside potential.

Conclusion

The Magnificent Seven probably won’t keep doing the heavy lifting forever. Recovering high-growth tech stocks, like SQ, DKNG, and INTU, could be quick to make up for lost time. Of the trio, Wall Street expects the biggest gains from Block stock, with almost 40% in year-ahead upside potential.