Simon Property Group stock (NYSE:SPG) has unleashed a barrage of dividend increases, reinforcing its bull case. The world’s largest retail REIT continues to post improving financials in the aftermath of the pandemic, resulting in multiple dividend hikes recently. In fact, the company closed Fiscal 2023 with record FFO/share (funds from operations per share, a cash-flow metric used by REITs), surpassing its pre-pandemic levels for the first time.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

I believe the ongoing momentum is set to persist. Therefore, I remain bullish on SPG stock.

Full Post-COVID Recovery Drives Dividend Increases

After overcoming the challenges posed by the pandemic, which greatly affected retail REITs, including Simon Property, the company has experienced a remarkable rebound in occupancy levels. This, coupled with increased rental rates, has propelled Simon Property to achieve a complete recovery. Thus, the company has successfully implemented a series of substantial dividend increases, showcasing its resilience and financial strength post-pandemic.

To begin with, I believe it all starts with retailers feeling a heightened sense of confidence in consumer spending over the past few quarters. It seems that retailers’ optimism is being fueled by several indicators pointing towards a reassuring “soft-landing” scenario. These include low unemployment and easing inflation. As a result, SPG has seen a significant upswing in occupancy levels, which landed at 95.8% at year-end – a noteworthy increase of 90 basis points compared to Fiscal 2022.

Simultaneously, seizing the substantial demand for its properties, Simon has pursued increasing rental rates, resulting in a base minimum rent (BMR) of $56.82 at the end of the year — a 3.1% uptick from the previous year. This is one of the highest BMRs I have ever seen a retail REIT achieve, underscoring Simon Property Group’s high-quality property portfolio.

The combination of rising occupancy and record base minimum rent levels led to total revenues for the year coming in at $5.66 billion, up 7% year-over-year. Interestingly, this brings SPG remarkably close to its pre-pandemic Fiscal 2019 revenue of $5.67 billion, signaling a full post-pandemic recovery.

SPG’s bottom-line results were even more impressive, with funds from operations per share (FFO/share) for the year landing at $12.51, up from last year’s $11.95 and setting a new record from 2019’s $12.37.

To me, it’s very impressive that Simon Property’s profitability has rebounded with such vigor, considering that most REITs out there are currently feeling the negative effects of multi-decade-high interest rates. Being the largest REIT in the space, however, Simon has managed to leverage its high-quality portfolio to maintain an attractive credit profile.

In particular, while the REIT’s average cost of debt did increase from a low of 3.03% in 2021 to 3.70% in 2023, it still remains at very competitive levels. Further, Simon’s weighted average yield to maturity stood at 7.2 years at the end of 2023, meaning the company is more or less insulated from potentially harmful refinancings in the medium term.

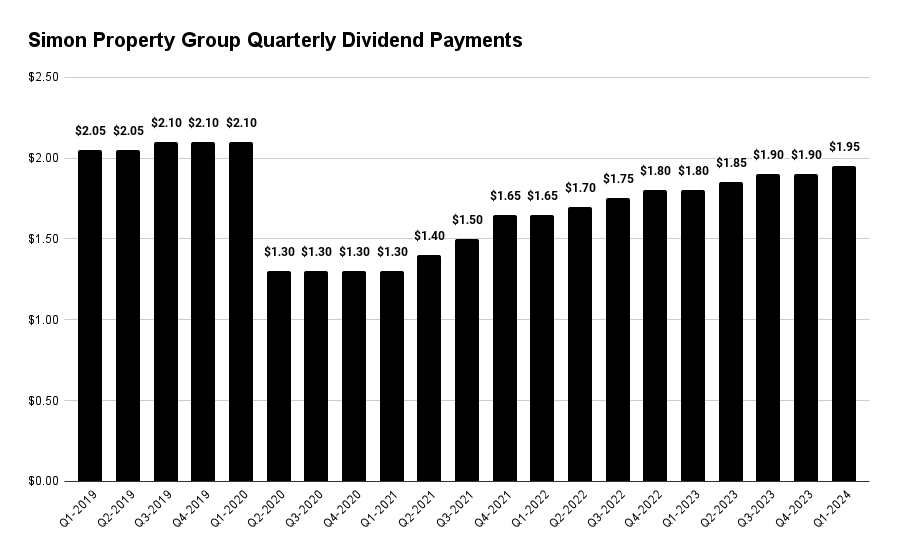

Seeing such a strong credit position and FFO/share reaching new highs, management has felt confident about continuing its aggressive post-pandemic dividend raises. As you can see in the bar chart below, Simon slashed its dividends to manage the underlying crisis once the pandemic hit. However, nine hikes have occurred thus far, with the most recent increase to $1.95, bringing the quarterly rate one step closer to its pre-pandemic level of $2.10.

It’s also worth noting that SPG’s payout ratio has improved substantially, as its FFO/share hit new records in FY2023, but the dividend is still hovering below its 2019 levels. The company’s FFO payout ratio was 60% last year, down from 69% in 2019. I believe this should encourage management to keep raising its dividend comfortably in the coming quarters, which, combined with its already decent dividend yield of 5.4%, forms a compelling dividend growth case.

Another factor signaling that SPG can easily afford further dividend increases is that the REIT recently announced a $2 billion stock buyback program. Not only does this imply notable excess cash generation, but it also suggests that management finds Simon’s current valuation attractive.

Is SPG Stock a Buy, According to Analysts?

Wall Street’s view of Simon Property Group seems a bit more conservative. The retail real estate giant currently features a Moderate Buy consensus rating based on five Buys and eight Holds assigned in the past three months. At $150, the average SPG stock forecast implies just 4.5% upside potential.

If you’re looking for the right analyst to guide your decisions in buying and selling SPG stock, look no further than Caitlin Burrows, who represents Goldman Sachs (NYSE:GS). Her performance over a one-year time frame has been outstanding, boasting an impressive average return of 34.17% per rating with a success rate of 100%. Click on the image below to learn more.

The Takeaway

SPG’s strong post-COVID recovery, marked by increased occupancy levels and rising rental rates, has paved the way for a series of dividend increases. The company ended Fiscal 2023 on a high note, with record FFO/share and an improved payout ratio, signaling that the ongoing dividend growth streak will likely persist. This momentum, coupled with a robust credit profile and an attractive dividend yield, form a compelling investment case, reinforcing my bullish view of the stock.