While Sonos (NASDAQ:SONO) does have some exciting new developments afoot, I’m still bearish on the company. There’s a lot going on, but much of it depends on things working out in the future. Sonos makes some of the best speakers and audio gear around. Its recent earnings results gave the stock a small boost. The company posted a -$0.50 per share loss, worse than the TipRanks projections that called for -$0.44 per share. Still, its adjusted earnings per share came in at -$0.32, ahead of the -$0.33 non-GAAP consensus estimate.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Revenue was also a win at Sonos. The company posted $316.3 million in revenue, which beat projections of $298.7 million.

Earnings beats are generally good news, evidenced by SONO stock outperforming the market today, but I question whether it can continue. I’m not alone in this conclusion, either.

Is Sonos Stock a Good Buy, According to Analysts?

Turning to Wall Street, Sonos has a Hold consensus rating. That’s based on two Holds assigned in the past three months. The average Sonos price target of $17 implies 0.8% downside potential. Both analysts currently giving Sonos coverage have the same price target of $17 per share.

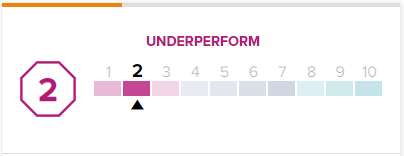

Also, Sonos has a Smart Score of 2 out of 10 on TipRanks. That’s the second-lowest level of “underperform.” This makes a very strong possibility that Sonos will ultimately underperform the broader market.

The real disaster comes from hedge funds. Hedge funds sold 3.2 million shares last quarter. Given that they only had around 3.362 million shares of Sonos to begin with that quarter, this represents a sell-off of over 96%, and the sentiment is now considered “very negative.”

The company’s financials won’t offer much help either. Revenue has been in decline for the last three quarters, as the company started December 2021 with $664.48 million. That dropped to $399.78 million in March, and $371.78 in June. Now it’s $316.3 million.

While the holiday shopping season will likely help recover those figures, the company seems to routinely lose out whenever large amounts of gifts aren’t being purchased.

Big Plans, but Perhaps Not Big Enough

Granted, things don’t look that great at Sonos. Several indicators are turning against it, and even today, the stock has downside risk against its average price target. However, the company has a slate of plans that may help it turn things around; one of the biggest is several new models. A report from The Verge notes that the company is set to enter four new product categories starting next year. One of these is expected to address a hole in the company’s product lineup that has been around for years: headphones.

Sonos recently acquired T2 Software, a company that might have been the missing link between Sonos’s current product line and the potential release of wireless headphones. Naturally, any of these plans are subject to change, especially if the company should have to pivot into a recessionary footing where home audio is a distant concern for homeowners.

There’s also a potential high point for investors as Sonos pursues litigation targeting Google (NASDAQ:GOOGL). A win there could mean a win for investors as well.

Consumers, meanwhile, begin to grow concerned about the lack of discounts at Sonos. One report noted that a Black Friday deal from Sonos would be welcome.

New product arrivals, like the Sonos Sub Mini, are also proving valuable additions to home theater systems. Given the state of theater operators like AMC Entertainment (NYSE:AMC), home theater systems should be enjoying a boom.

Conclusion: An Increasingly Muted Future

The news doesn’t look good for Sonos right now. Declining revenue is never a good sign, and sentiment indicators in the negative are also a negative sign. The analyst perspective—where it even exists—is fairly sour as well. Throw in an environment where consumers are the least likely to purchase home audio equipment that they’ve been in years, and the end result doesn’t look good for Sonos. Take all these factors together, and you can see why I’m bearish.