Shares of Millennial-loved fintech darling SoFi Technologies (NASDAQ:SOFI) have been steadily trending lower of late, with shares down around 32% from recent 52-week highs. Despite the ominous stock chart, many upbeat analysts still believe the stock’s a tempting dip buy at current levels. The fintech bubble may have burst two years ago, but SoFi seems like one of the industry players poised to rise from the rubble.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Indeed, the company’s recent quarterly earnings beat is encouraging, as too are comments made by its CEO Anthony Noto in a recent sitdown with Mad Money host Jim Cramer, who noted SoFi is stealing market share from the big banks. Targeting the big banks could mean big growth opportunities to be had for the $7.26 billion firm that rose to fame for its student loan services.

At this juncture, it seems like SoFi is ready to ramp up its disruptive innovative capabilities to beckon more folks away from traditional banking services.

All things considered, I have to stand with the many bullish analysts covering the name. Sure, SOFI stock has been battered, but in the digital age, I’m inclined to side with the neobanks over the old-school banks that are more or less being forced to spend on technological initiatives or run the risk of being left behind.

SoFi Has Room to Run as It Expands Its Financial Services Footprint

SoFi has come a long way since its days serving mostly students seeking to borrow or manage their university loans. Though the company is still a dominant behemoth in the realm of student loans with around 60% market share, it’s other areas of financial services that could really help drive growth in the long term.

With a broader range of financial services and plenty of upselling opportunities (many loyal student loan customers are ready to refinance with SoFi with student loan payments resuming), SoFi’s growth narrative still seems as sound as ever.

More recently, the company assisted in underwriting the Instacart (NASDAQ:CART) IPO, marking a notable first for the company.

Eugene Simuni, an analyst over at Moffett Nathanson, viewed SoFi’s involvement with the CART IPO as a “very positive development.” I couldn’t agree more. SoFi is becoming less of a niche fintech play and more of a neobank over time. As the company begins cutting more into the turf of the big banks, I think the rewards will eventually come.

For now, however, the company is still in full-on growth mode, and investors shouldn’t expect the firm to take its foot off the pedal, even as high-interest rates incentivize firms to cut back on excess expenditures, including those essential to a long-term growth engine.

As interest rates finally do peak (and perhaps slide), I believe SoFi is one of the technology firms that could stand to explode higher as investors rotate back into the most disruptive of innovators. For now, SoFi stock is one of the market’s losers of the high-rate world. However, once the tables turn, I do not doubt SoFi stock’s ability to pick up where it left off before the Fed started cranking rates higher.

Five-Star Analyst Sees a Path for Considerable Upside

Five-star-rated Jefferies analyst John Hecht is one of the bigger bulls on SoFi stock, with a Buy rating and a $15.00 price target, which entails 87.7% upside potential from current levels. Mr. Hecht doesn’t think it will take much to move the needle much higher on the stock, stating, “Even a modest recovery would be a catalyst for loan growth.”

I’m inclined to agree. The stock has been so heavily punished already, now sitting down around 72% from its 2021 all-time highs of around $28 per share. At writing, shares go for 4.0 times price-to-sales (P/S). That’s about in line with the financial services industry average price-to-sales multiple. Given SoFi’s tech edge and its strong and mostly young user base, shares deserve a much fatter premium, in my opinion, as the company aims to one-up the banks over the coming years.

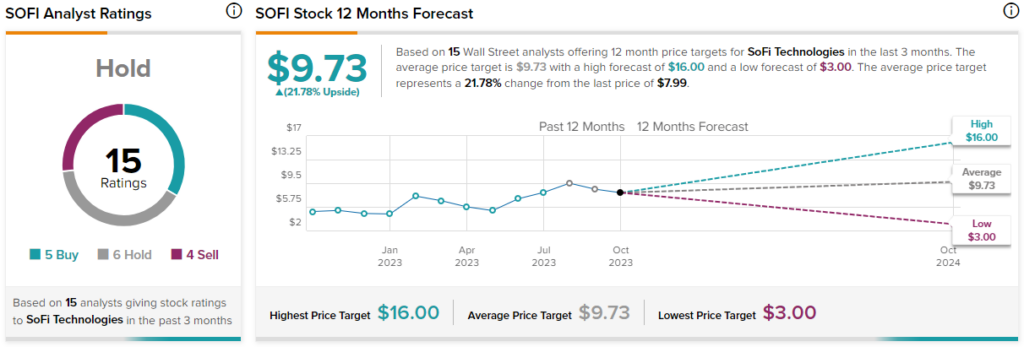

Is SOFI Stock a Buy, According to Analysts?

On TipRanks, SOFI stock comes in as a Hold. Out of 15 analyst ratings, there are five Buys, six Holds, and four Sell recommendations. The average SOFI stock price target is $9.73, implying upside potential of 21.8%. Analyst price targets range from a low of $3.00 per share to a high of $16.00 per share.

The Bottom Line

SoFi stock has already been punished for being a high-growth, high-spending disruptor in a high-interest-rate world. As the firm continues to bring the fight to traditional banks with its high-tech advantage, I wouldn’t bet against the firm, as even a small positive could be a huge positive for the firm, given how much the bar has been lowered in recent years.