Shares of data cloud company Snowflake (SNOW) was arguably one of the most exciting (and expensive) growth stocks in the market before its meltdown.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

After suffering a near-60% drop from peak to trough, shares of the disruptive big-data innovator are still one of the priciest plays in the entire stock market.

At writing, shares go for over 54 times sales. At its low point, SNOW stock traded at around 45 times sales. Hardly a bargain, given how quick investors were to turn against high-multiple stocks.

While Snowflake stock has endured a painful collapse, thanks in part to muted revenue guidance as a part of its latest quarter, one can’t help but notice SNOW stock has not fallen by nearly as much as some of the other high-multiple stocks out there.

Amid the growth sell-off, some stocks have been cut by 80% from their peak levels, making a 55-60% plunge less devastating. I’m neutral on the stock.

Warren Buffett’s Stake

While I do think Warren Buffett’s uncharacteristic investment in Snowflake is a massive vote of confidence in the firm’s longer-term fundamentals, the stock still remains a tough one to get behind, especially if the tech carnage isn’t yet over.

If anything, lower revenues moving forward could cause SNOW to really fall under its own power. This remains a top risk. Though I wish to take CEO Frank Slootman’s word, it’s hard to tell the difference between an overly conservative guide and one that could signal the beginning of a bleak trend.

Given rising recession risks and Snowflake’s 35% rally off its lows, the stakes seem way too high. The stage could be set for another snowstorm of volatility, even as the rest of the market finds its footing.

Nothing short of perfection and upbeat guidance should be baked in at such a valuation.

Snowflake Innovating Rapidly

Snowflake’s consumption-based model could be the way of the future. Although it makes valuing cloud companies like Snowflake harder, it makes things more convenient for users.

With the recent acquisition of Streamlit, users have more reasons to use the Snowflake platform and its growing toolset. Just how much could the addition of such an intriguing data visualization technology bolster usage? It’s hard to say over the near term, especially if the economy falters this year.

More recently, Snowflake launched its Healthcare and Life Sciences cloud offering, a product that could help reignite growth as the firm looks to widen its moat around the data cloud.

The company is innovating rapidly, but are such innovations driving revenue optimally? Probably not. Slootman is focused on the long run, and is willing to move through messier numbers if it means creating value and trust with its customer base.

For such reasons, Snowflake’s conservative guide is certainly not ideal.

Wall Street’s Take

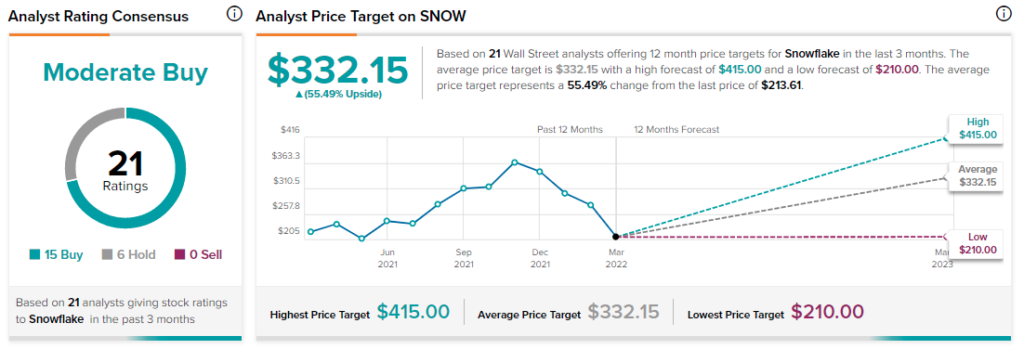

According to TipRanks’ rating consensus, SNOW stock comes in as a Moderate Buy. Out of 21 analyst ratings, there are 15 Buy recommendations and six Hold recommendations.

The average Snowflake price target is $334.65, implying 55.5% upside potential. Analyst price targets range from a low of $210 per share to a high of $415 per share.

Bottom Line

Snowflake remains one of the most expensive stocks in this market. If the bottom is in for speculative tech (the recent rally suggests such), SNOW stock could regain its footing on the back of a beat on an already lowered revenue bar.

However, if we’re at the cusp of recession and revenues fall short of already lowered expectations, count me as unsurprised if the stock falls further.

Download the TipRanks mobile app now

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure