Snowflake (NYSE:SNOW) stock has undergone a significant decline lately, but there could be more pain ahead for the stock, given its pricy valuation.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Specifically, Snowflake has already lost more than 68% of its value since November of 2021, when shares briefly traded at almost $430/share. During this period, the company has evolved considerably, posting some of the most impressive growth metrics among its cloud peers. Still, despite the disanalogous development of a declining stock price against growing financials, Snowflake’s valuation remains rather hard to justify.

Accordingly, there could be more downside for Snowflake moving forward, which is why I am bearish on the stock.

Why Snowflake Trades at a Steep Premium

As mentioned, despite Snowflake already suffering dramatic losses, the stock continues to trade at a premium valuation. At a forward P/S ratio and forward P/E ratio of 15.3 and 234.7, respectively, Snowflake remains one of the most expensive stocks in the market. It makes anyone wonder why investors are willing to pay such rich valuation multiples for the stock. We can break this answer down into qualitative and quantitative points of view.

The Qualitative Point of View

From a qualitative point of view, Snowflake is considered one of the most innovative companies within the cloud computing space for several reasons that set it apart from its peers. I have attempted to summarize the company’s unique attributes and explain them in simple terms.

- Cloud-native architecture:

Snowflake was built from the ground up to operate in the cloud, and its architecture is designed to fully leverage the resources of cloud computing. This allows the company to develop its solutions with greater scalability, flexibility, and cost-efficiency capabilities compared to traditional on-premises solutions.

- Performance and speed:

Due to Snowflake’s unique architecture, the company is able to deliver high-speed querying and processing of large datasets, even when multiple users are accessing the system simultaneously. This is because the company separates its compute and storage layers, which allows for self-supported scaling of each component.

- Superior security:

Snowflake offers built-in security elements such as data encryption, role-based access control, and multi-factor authentication. This helps to secure the protection of sensitive data while meeting all compliance requirements.

- Ease of use:

Snowflake’s capabilities may be sophisticated and complex, but the platform’s user-friendly interface and simplified SQL (programming) language make it easy for non-technical users to access and examine data. Also, Snowflake integrates with many popular cloud tools and platforms, further streamlining the data analytics process.

The Quantitative Point of View

From a quantitative point of view, investors have been willing to pay a premium valuation for the stock due to the significantly above-average growth metrics the company has been able to deliver. Of course, it’s worth noting that Snowflake’s growth is driven by the unique qualities we just discussed.

In particular, despite the corporate world striving to control expenses these days, which has led to decelerating revenue growth for all cloud companies, including Snowflake, revenue growth remains outstanding. In its most recent Q4 results, Snowflake posted revenues of $589 million, 53% higher compared to the prior-year period. Again, this implies a deceleration compared to the 101% revenue growth the company posted in Q4-2021, but its overall trajectory remains beyond impressive.

The company has also guided for Q1 revenue growth to be between 44% and 45%. Assuming there is prudent consideration embedded in this outlook, we can expect revenue growth of just under 50%, implying Snowflake’s impressive momentum is to last in the coming quarters, despite the ongoing slowdown in global cloud spending.

Is SNOW Stock a Buy, According to Analysts?

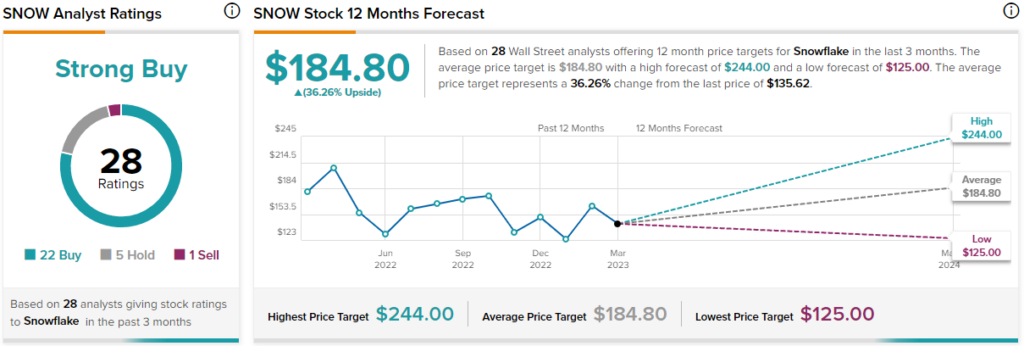

Turning to Wall Street, Snowflake has a Moderate Buy consensus rating based on 22 Buys, five Holds, and one Sell assigned in the past three months. At $184.80, the average Snowflake stock forecast implies 36.3% upside potential.

Takeaway – Why There Could be More Pain for Snow Stock

In my view, Snowflake stock does deserve to trade at a premium valuation, given its unique qualities and industry-leading growth metrics. However, the aforementioned multiples are very hard to justify, even following the stock’s prolonged decline. This is especially true in the current market landscape, in which investors tend to prioritize profits over growth, and in that aspect, Snowflake fails to deliver.

Precisely, despite the company growing at excellent rates and its data-as-a-service business model enjoying gross margins north of 75%, operating expenses actually exceed both revenues and gross profits. Snowflake’s operating expenses in Q4 grew by an equally tremendous rate of 55.1% to $623.1 million, leading to Snowflake posting an operating loss of $239.8 million. What’s even more concerning is that management doesn’t really seem worried about controlling expenses, with Q4 stock-based compensation skyrocketing 72% to $250.7 million.

All around, without diminishing Snowflake’s impressive growth prospects, I don’t believe that the stock can keep hovering near such excessive valuation multiples, given the lack of profits and continuous dilution. Investors are not being compensated with a measurable earnings/dividend/buyback yield, meaning there is not really any margin of safety or a floor for the stock. This could result in further stock price headwinds in the coming quarters.