Software stocks have taken a dive like the rest of the technology industry, but that could offer buying opportunities if you know where to look. In this piece, we used TipRanks’ Comparison Tool to evaluate two software stocks. Although Snowflake (NYSE: SNOW) and Palantir Technologies (NYSE: PLTR) are both software companies, they are quite different, addressing different markets and utilizing different kinds of proprietary technology. Those differences may call for a contrarian view.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Variety is the Spice of the Software Sector

Software has had a challenging year like the rest of the tech sector, but one benefit of software stocks is that they come in a wide variety. For example, while Snowflake and Palantir are both in the data and analytics space, they utilize two different business models. Snowflake takes a traditional cloud-based approach to data warehousing, while Palantir uses its own private operating system models.

These different approaches to data analysis enable Snowflake and Palantir to address different parts of the industry. Palantir doesn’t actually store data but instead enables companies to manage and analyze their own on-premises and cloud data. Its use of private operating system models offers greater customizability, and its defense specialization makes it unique among software firms.

On the other hand, Snowflake’s more traditional approach allows companies to not only analyze their data but store it as well. The differences between these companies are critical when it comes to valuation.

Snowflake (SNOW)

In many ways, it seems like Snowflake can do no wrong where investors are concerned. Although the stock is down 55% year-to-date, it remains a darling of the software sector despite having been one of the sector’s most expensive stocks in 2020 and 2021. As a result, a Hold mindset may be appropriate due to its valuation, crowding, and other factors.

Snowflake isn’t profitable yet, and it doesn’t look like it will be profitable anytime soon. It trades at a price/sales multiple of around 30x, higher than its competitor Zscaler (NASDAQ: ZS). Additionally, Snowflake is extremely crowded right now, with 59% institutional ownership. While this crowding can be a positive thing when things are good, it can turn terrible at a moment’s notice, leaving institutions competing to dump their shares.

One issue with Snowflake’s business model is that it’s not subscription-based like other cloud-based models are. Customers pay for the amount of storage they use rather than a flat monthly rate, which could be a problem if or when enterprises start looking for places to cut back as their earnings tumble in a recession.

This consumption-based business model also means Snowflake could be more expensive for some enterprises than they expected when signing up. For that reason, price transparency and predictability are lacking at a critical time in the business cycle.

On the other hand, one thing Snowflake has going for it is that its product is cloud-agnostic, meaning it can work with multiple clouds from multiple providers. Additionally, the SaaS firm is growing rapidly, with its product revenue surging 83% year-over-year to $466.3 million in the second quarter of Fiscal 2023. Total revenue also rose 83% to $497.25 million. However, Snowflake lost $222.8 million in the July 2022 quarter, an increase from the $189.7 million it lost in the July 2021 quarter.

At the end of the day, the company may have a bright future, and many investors are certainly betting on that. However, in the current environment, it looks fairly valued or perhaps slightly overvalued due to its lack of profitability or visible path to profitability. Further, the significant decline in deferred revenues in the most recently completed quarter is cause for concern.

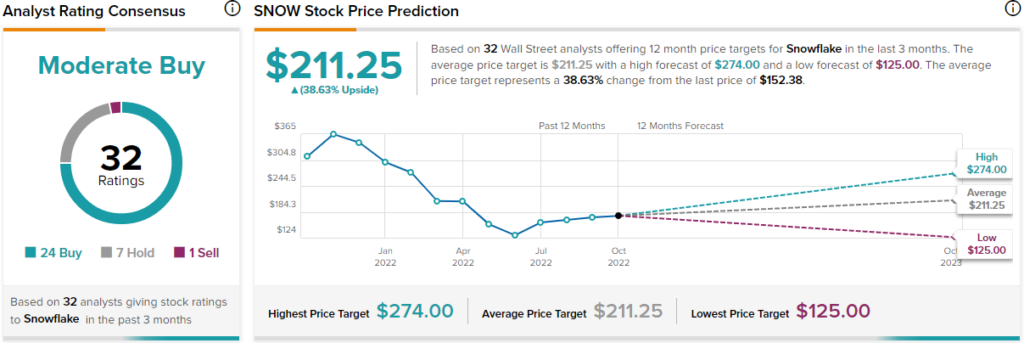

What is the Price Target for SNOW stock?

Snowflake has a Moderate Buy consensus rating based on 24 Buy ratings, seven Hold ratings, and one Sell rating over the last three months. At $211.25, the average price target for Snowflake implies upside potential of 38.6%.

Palantir Technologies (PLTR)

The general view of Palantir Technologies is the complete opposite of Snowflake’s. After careful analysis of many factors, it’s difficult to understand why the market hates this stock so much. Thus, a long-term bullish view appears appropriate due to its government contracts and low P/S ratio of about 9x.

One important thing to point out about Palantir is its exposure to the defense industry through its data analytics software that’s specialized for defense and intelligence gathering. Of course, the sector hasn’t done particularly well this year, declining about 20% year-to-date based on the S&P Aerospace & Defense Select Industry Index.

However, the geopolitical uncertainty that includes the war in Ukraine and the situation between China and Taiwan calls for a more constructive view of the industry. Thus, it’s unclear why Palantir’s stock isn’t seeing support like fellow defense contractors Raytheon (NYSE: RTX), which is down only 4% year-to-date, and Northrop Grumman (NYSE: NOC), which is up 20%.

One of Palantir’s big contract wins this year was a $229 million one-year contract with the Defense Department. In fact, that contract is an expansion of one that originally was just for the U.S. Army Research Laboratory because it now covers all branches of the military. The company will provide artificial intelligence and machine learning capabilities to all branches of the U.S. military.

Google (NASDAQ: GOOG) (NASDAQ: GOOGL) actually abandoned that contract due to a widespread protest about its technology being used for surveillance. This could be one reason the market hates Palantir Technologies so much, but from a financial standpoint, there is much to like.

Palantir also announced that it had renewed a contract with the Department of Homeland Security. It also works with Immigrations and Customs Enforcement — another contract that has been controversial.

Unfortunately, it has a string of earnings misses and even slashed its revenue outlook in its most recent earnings report. However, that reduction was explained by the unclear timing of the company’s government contracts, which have since been renewed and expanded.

While Palantir isn’t profitable yet, its management said during an earnings call earlier this year that they expect to be profitable by 2025. In the meantime, the company has a healthy balance sheet with ~$2.4 billion in cash and equivalents versus $933.5 million in liabilities.

What is the Price Target for PLTR stock?

Palantir Technologies has a Hold consensus rating based on two Buys, two Holds, and four Sells assigned over the last three months. At $10.50, the average price target for Palantir Technologies implies upside potential of 30.11%.

Conclusion: Hold on to Snowflake; Consider Buying Palantir

As things stand right now, the market is in love with Snowflake, at least as much as it can be while selling it off, and it views Palantir as an anathema. However, a review of the data suggests a contrarian view may be in order.

Ultimately, Snowflake looks fairly valued or potentially a bit overvalued. In contrast, Palantir looks undervalued, which appears temporary, although it may take a few years for this to play out.