Visa (NYSE:V) shares are trending higher following better-than-expected Fiscal Q4-2022 results aided by robust momentum in consumer payments and a rebound in cross-border travel. The current discounted valuation likely presents a great buying opportunity, especially given Visa’s long-term growth potential.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Investors can get added reassurance in the stock from increased dividends and buybacks announced by the company, exuberating a strong outlook for the global payment processing company.

A Snapshot of Visa’s Q4-2022 Results

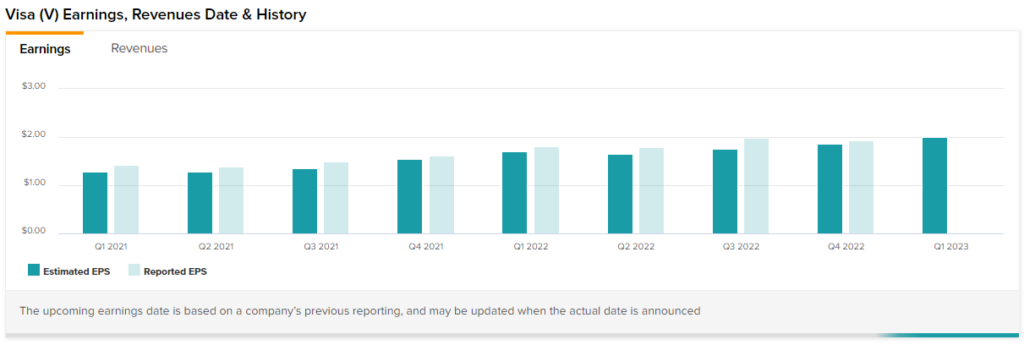

Adjusted earnings of $1.93 per share beat consensus estimates of $1.87 per share. Further, it was much higher compared to earnings of $1.62 per share in the prior-year period.

Moreover, revenues jumped 18.9% year-over-year to $7.8 billion and exceeded consensus estimates by $250 million. The top line benefited from solid 36% growth in total cross-border volumes. Meanwhile, total processed transactions grew 12% to 50.9 billion.

Visa Increases Dividends & Buybacks

Concurrent with the earnings, the company announced a 20% hike in its quarterly dividend to $0.45 per share. The dividend is payable on December 1 to shareholders on record as of November 11.

On top of that, the company rewarded shareholders with a new share repurchase program of $12 billion.

Is Visa Stock a Buy or Sell?

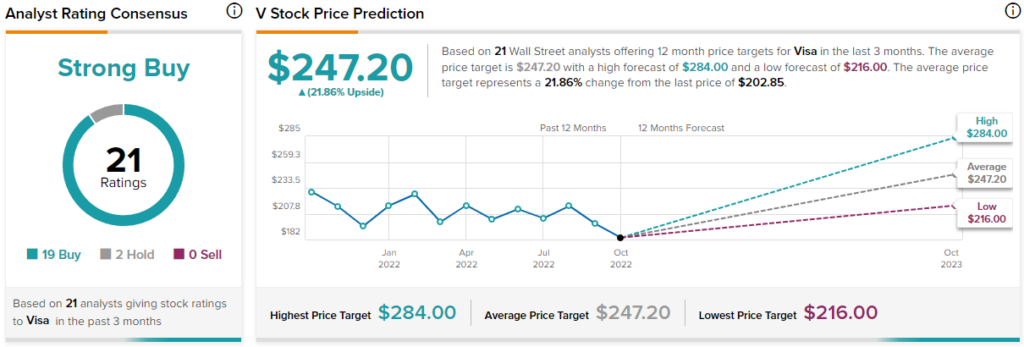

The Wall Street community is clearly optimistic about the stock. Overall, the stock commands a Strong Buy consensus rating based on 19 Buys and two Holds. Visa’s average price target of $247.55 implies 21.73% upside potential from current levels.

Following the upbeat results, Jefferies analyst Trevor Williams increased his price target on Visa to $225 from $220 and reiterated a Buy rating.

Williams stated, “While we would have preferred a more conservative baseline for the initial FY23 revenue outlook (assumes no recession) to help de-risk the go-forward, we’re encouraged by continued strength in domestic volumes/ongoing cross-border recovery, take comfort in management’s commitment to use expenses as a buffer against any top-line slippage, and like the entry point with valuation near five-year lows.”

Conclusion: Consider Purchasing Visa Stock

Based on cross-border recovery, inflation, and secular growth in payments, payment processing companies like Visa and Mastercard (NYSE:MA) will continue to report solid growth in the coming months.

Notably, both stocks are trading at a discount to their own five-year historical P/E averages. Visa is currently trading at a P/E ratio of 25x, reflecting a 28% discount from its five-year average of 35.36. Meanwhile, Mastercard’s P/E ratio is 31x, a 25% discount from its five-year average of 41x.

The discounted valuation potentially presents a great buying opportunity for Visa and even Mastercard, given the strong growth fundamentals for both companies.

Mastercard, expected to release its Q3 results tomorrow, is already trending higher this week.