Shopify (TSE:SHOP) (NYSE:SHOP) is scheduled to release its fourth-quarter 2022 results on February 15, after the market closes. The company’s strong performance during the Black Friday Cyber Monday weekend might have supported its performance in Q4. Shopify provides a cloud-based commerce platform for small and medium-sized businesses.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Overall, the quarter witnessed a slowdown in consumer discretionary spending due to the challenging macroeconomic environment. Further, the strengthening of the U.S. dollar in the to-be-reported quarter is likely to have hurt bottom-line growth.

The Street expects Shopify to post a loss of $0.01 per share in Q4, compared with earnings of $0.14 per share in the year-ago quarter. Meanwhile, revenue expectations are pegged at $1.6 billion, representing a year-over-year growth of 14.3%.

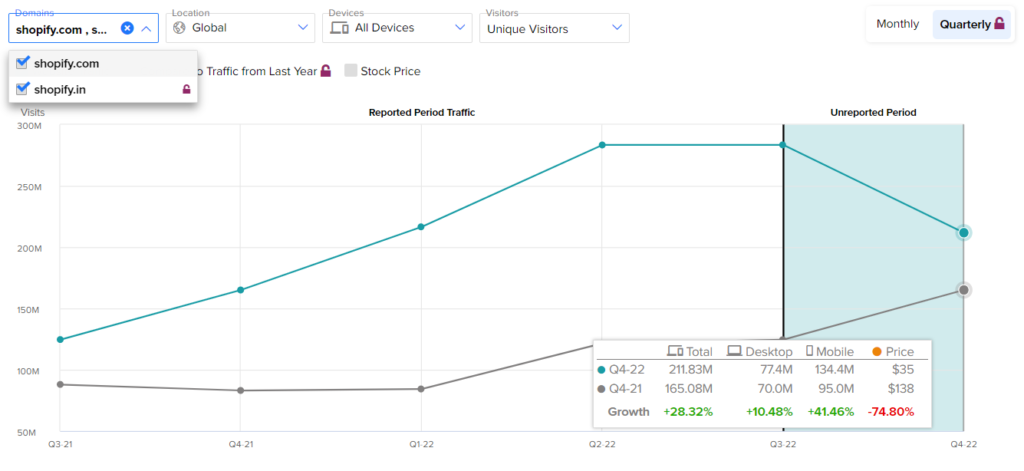

Website Traffic Paints a Positive Picture

SHOP’s total website visits are a good indicator of user involvement on its platform. As per the TipRanks Website Traffic tool, total global visits to shopify.com and shopify.in climbed 28.3% year-over-year in the to-be-reported quarter.

The increase in monthly visits could indicate that demand for the company’s products remained upbeat during the quarter.

Is Shopify a Buy or Sell?

Wall Street is cautiously optimistic about the stock with a Moderate Buy consensus rating. This is based on nine Buy, 13 Hold, and two Sell recommendations. The average SHOP stock price target of $42.86 implies 12% downside potential from the current level. Shares of the company are up 26.8% in the past three months.

Ending Thoughts

The company’s efforts to expand its total addressable market with investments in various areas, including logistics, payments, and marketing, should support its performance in the upcoming quarter. Furthermore, the retailer recently increased prices on their merchant subscription plans. The move bodes well for its top-line growth.