Many investors find it beneficial to include real estate investment trusts, or REITs, in their portfolios. These companies bring a suite of advantages that can’t be overlooked. To start with, they offer a sound way to buy exposure to real property, landholdings, without actually buying real estate. REITs are also known as champion dividend payers, as they’re required to distribute up to 90% of their taxable income to shareholders – and dividends make a convenient mode of compliance.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

For Wedbush analyst Richard Anderson, these basic facts about REITs make them indispensable. But some quirks of current conditions make them even better, in his view.

First, a number of REITs have been underperforming recently, offering investors low-cost entry points. And second, while the Federal Reserve has hinted that it will hold rates at high levels for longer, it has also indicated that the current round of rate-tightening is behind us now – and Anderson points out that US REITs tend to outperform after a round of higher interest rates. The combination of higher rates in a more stable environment is beneficial for these stocks.

Anderson doesn’t leave us with a macro view of the industry. The analyst delves into the micro level, selecting two REIT stocks, both of which are high-yield dividend payers, offering a dividend return of up to 8%. We ran them through the TipRanks database to see what makes them stand out.

Healthcare Realty Trust (HR)

The first high-yield dividend payer we’ll look at is Healthcare Realty Trust, a real estate investment trust that specializes in, you guessed it, medical office space. The company’s portfolio makeup makes it clear that HR is the leader in the medical office building REIT niche. The company owns 714 properties across 35 states, totaling almost 42 million square feet of usable, leasable space.

HR has focused its efforts on major urban areas, with properties in the fast-growing metro area of Dallas, Texas, making up 9.7% of the medical office building portfolio, or 3.308 million square feet. Other metros where Healthcare Realty Trust has a major presence include Houston, Texas; Boston, Massachusetts; and Charlotte, North Carolina.

This company assumed its current form through a merger completed in July of last year. That transaction, a merger with Healthcare Trust of America, put HR in a class of its own by combining two of the country’s largest owners of medical office spaces into the leading pure-play medical office building REIT.

On the financial side, HR generated total revenues of $338.1 million in the last reported quarter, 2Q23. This was in line with the results from 4Q22 and exceeded the forecast by $8.3 million. At the bottom line, as far as dividend investors are concerned, the company delivered a normalized funds from operations (FFO) per diluted share of 39 cents. This was down from 42 cents in 4Q22, and it slightly missed the estimates by one cent per share.

However, the FFO fully covered the 31-cent common share dividend, which was last paid out in August. At the annualized rate of $1.24 per common share, the dividend is yielding 8.4%, more than double the current annualized inflation number.

Turning to Anderson, and the Wedbush view of this stock, we find that the analyst is appreciative of the business model, particularly the stability inherent in medical office buildings. He writes, “MOBs [medical office buildings] have been the beneficiary of the movement of care into outpatient settings versus the much higher costs associated with inpatient (i.e., care inside the hospital) services… MOBs tend to produce low single -digit yet highly visible/stable rent growth – an attractive asset class during periods of uncertainty (aka, risk -off). During 2Q23, the company experienced strong leasing volume which was in part a function of the larger footprint created by the merger. Although same store growth is being hampered by elevated expenses (guidance down 50bps versus previous), we view the stability of the story as remaining very much intact.”

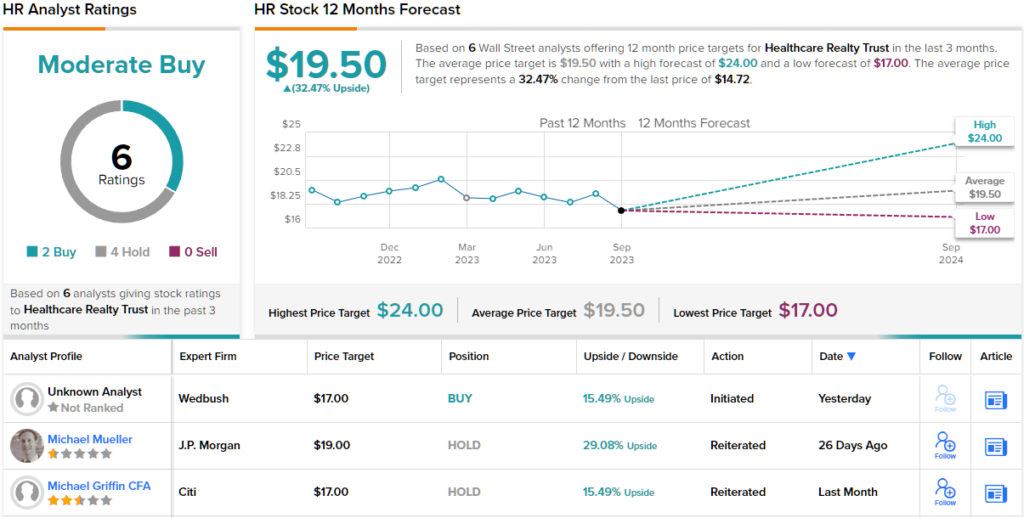

Anderson goes on to give HR shares an Outperform (i.e. Buy) rating, and his price target of $17 implies the stock will gain ~15% on the one-year time frame. Add in the dividend, and the potential return exceeds 23% for the year ahead.

Overall, HR gets a Moderate Buy consensus rating from the Street, based on 6 recent analyst reviews that include 2 Buys and 4 Holds. The shares are trading for $14.72 and their $19.50 average price target suggest a solid 12-month gain of ~32%. (See HR stock forecast)

Apartment Income REIT (AIRC)

Next on our list is Apartment Income REIT, another specialist REIT. As the name suggests, this company focuses on owning and managing apartments and multi-family apartment developments. The company operates in 8 core metropolitan areas and owns 73 communities in 10 states, plus DC, comprising a total of 25,739 apartment homes on its properties. AIRC can boast of a 62% tenant retention rate, which is high for the high-turnover apartment segment.

Like HR above, this company can rely on the advantages of scale. In addition to its substantial real estate holdings, it boasts a market cap of $4.45 billion and $2.3 billion in available liquid assets. The company has also developed a qualitative edge by focusing on the needs of the residents in its properties, selecting a high-quality tenant base that is satisfied with the apartment homes. It’s a solid foundation for ‘best-in-class property management.’

This business model has also led to consistently high revenues. AIRC has seen its top line exceed $200 million in each of the last four quarters. In the most recent reported quarter, 2Q23, the company had total revenues of $214.6 million, up almost 17% year-over-year and $2.8 million above expectations. The company’s FFO of 62 cents per share was up 3% from the previous year and beat the forecast by 2 cents per share.

These results support AIRC’s dividend payment, which was declared in July at 45 cents per share, paid out at the end of August. The dividend has an annualized rate of $1.80 per common share and a solid yield of 6%.

Tenant retention and a sound business model have brought this REIT to Anderson’s attention, and he writes of it for Wedbush: “During 2Q23, AIRC reported strong tenant retention of 62% which helps reduce downtime while saving on expenses. The AIRC platform is structured to allow top line NOI to matriculate smoothly to bottom line FFO, absent the noise of short -term dilutive forces from development activities. The company identifies the ‘Air Edge’ as its ability to apply an improved operating model onto previously acquired assets, thereby enhancing the growth profile beyond the initial point of the investment. For example, 2021 acquisitions have since produced 30% NOI growth and 420bps of margin expansion. All in, AIRC is a solid/safe multifamily story with an improving leverage profile.”

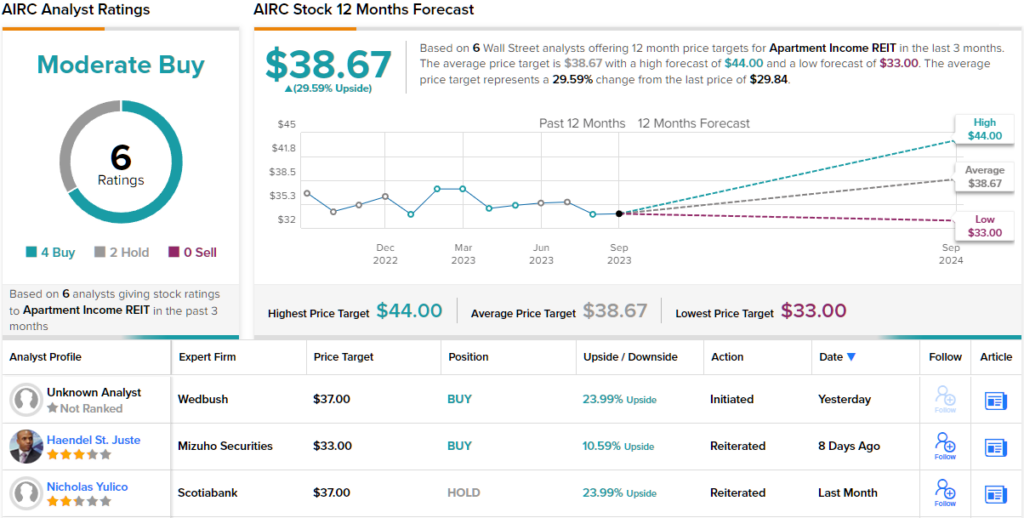

These comments back up his Outperform (i.e. Buy) rating on the stock, while his $37 price target points toward a one-year share gain of 24%. Based on the current dividend yield and the expected price appreciation, the stock has 30% potential total return profile.

Overall, there are 6 recent analyst reviews on record for AIRC, breaking down 4 to 2 in favor of Buys over Holds for a Moderate Buy consensus rating. The stock is currently trading for $29.84 and has an average target price of $38.67; this combination implies ~30% upside potential going out to the one-year horizon. (See AIRC stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.