Are the headwinds piling up? The Middle East war has appeared on the verge of expanding into a larger conflict, and an uptick in US inflation has put a ‘hold’ on expectations for a Fed rate cut this summer. This could be part of the normal cycling of the economy – except that there are some $52 billion worth of outstanding long positions on the S&P 500, and according to Citigroup’s Chris Montagu, 88% of those positions are currently in a loss.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

“Should the market turn negative, the move could be faster and larger due to the large, long positions already in the red… Remaining long positions are already marginally in loss and this positioning setup could amplify any negative market reaction,” Montagu opined.

For the savvy investor, this sounds like a setup for dividend stocks. No matter how the market turns, the high-yield div stocks provide a stable revenue stream on a reliable schedule.

Using the TipRanks database, we’ve looked up some high-yield dividend payers that the Street’s analysts are recommending as the dividend stocks to buy. These are shares that bring solid yields to the table, up to almost 16%. Let’s take a closer look.

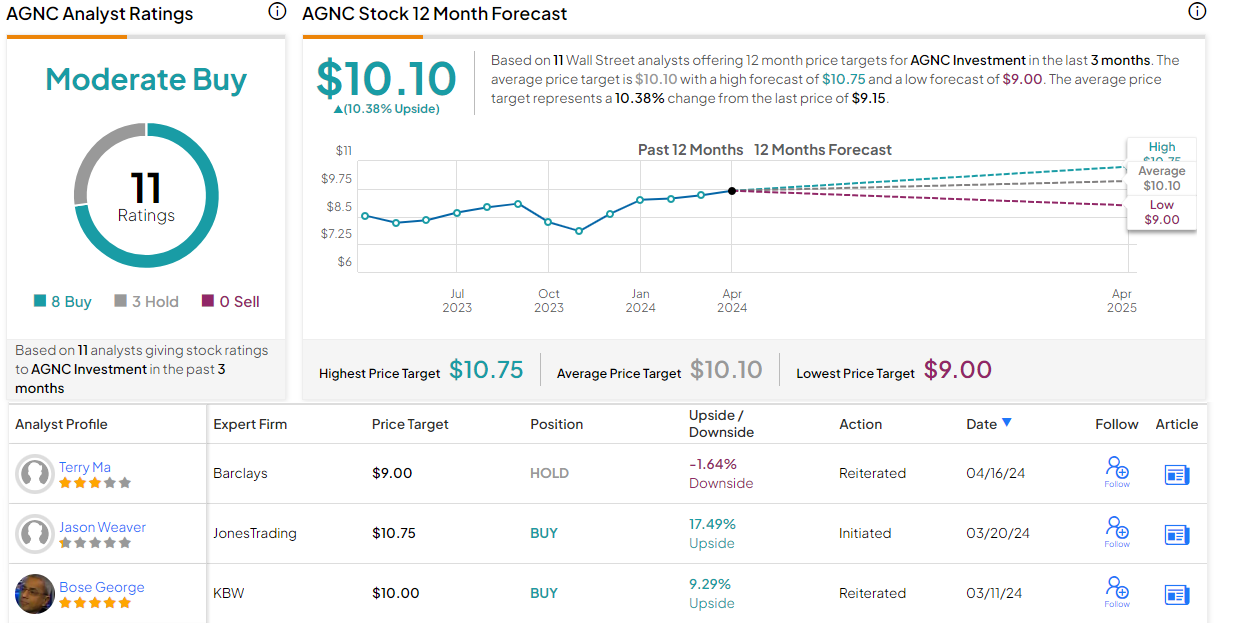

AGNC Investment (AGNC)

The first stock on our list is an internally managed mortgage REIT, or real estate investment trust. These companies bring capital investments to bear on the real estate industry, putting money into a variety of real-property assets, including mortgage loans and mortgage-backed securities (MBSs). Tax regulations typically require REITs to return a high proportion of their profits and earnings directly to investors, and the companies usually use dividends as the vehicle for that, making these stocks popular with dividend investors.

AGNC has built up a portfolio with a strong focus on mortgage-backed securities. As of December 31, 2023, the company’s investment portfolio was valued at $60.2 billion. This total included $53.8 billion in Agency MBS investments, $5.4 billion in net TBA mortgage positions, and $1.1 billion in credit risk transfer, or CRT. Drilling down a little further, we find that 95% of the company’s portfolio value comes from 30-year fixed-rate mortgages, long viewed as one of the most stable financial instruments.

In its last reported quarter, 4Q23, AGNC had a tangible net book value of $8.70 per common share. That figure was up 62 cents per common share from the previous quarter, an increase of 7.7%. At the bottom line, the company reported a “net spread and dollar roll” income per common share of 60 cents, a modest penny better than had been expected.

As for the company’s dividend, AGNC pays out its dividend monthly, at a rate of 12 cents per common share. This payment, when annualized, amounts to $1.44, and gives a juicy yield of ~15.74%. While most dividends are paid out quarterly, some investors prefer a monthly payment, as it provides more flexibility in using the income stream to meet current needs.

For analyst Jason Weaver, covering AGNC from Jones Trading, this stock represents a solid opportunity for investors. He writes of the company, “As a nearly pure-play levered agency RMBS strategy, AGNC’s prospects appear bright for expanding ROE generation capacity and/or book value appreciation near-term alongside expected moderation/easing of monetary policy… Given our view that leveraged agency MBS represents the best risk/ reward characteristics among mREIT strategies at present, along with AGNC’s history, scale, and consistency in strategy, not to mention greater liquidity, we expect this part of the mREIT universe will see the greater upside potential near-term as compared to others warranting a premium valuation.”

Looking ahead at the stock’s prospects, Weaver rates AGNC as a Buy, with a $10.75 price target pointing toward a 17.5% one-year share appreciation. Taken together with the current dividend yield, this implies a one-year return as high as 33%. (To watch Weaver’s track record, click here)

Overall, AGNC shares receive a Moderate Buy consensus rating from the Street, based on 11 recent analyst reviews, with a breakdown of 8 Buys to 3 Holds. The shares are priced at $9.15 and the average target price of $10.10, suggests a gain for the coming year of 10%. (See AGNC stock forecast)

Gladstone Commercial (GOOD)

For the second stock on our list, we’ll stick with REITs and look at Gladstone Commercial. As the company’s name suggests, Gladstone is focused on commercial real estate properties; specifically, the company invests its capital in ‘single tenant and anchored multi-tenant net leased industrial and office properties.’ Currently, the company has properties in the Midwest, the Southeast, and the Southwest, excluding California and Nevada – although Nevada is a target market. The fast-growing states of Florida and Texas are strongly represented in Gladstone’s overall portfolio.

That portfolio currently includes 135 office and industrial properties, located in 27 states. The company’s properties are leased out to 110 tenants, and Gladstone claims a current occupancy rate of 96.8%. The company boasts that its occupancy rate, a key metric for a REIT, has remained consistently above 95% since the firm’s 2003 IPO. The stability and high occupancy rates of Gladstone’s portfolio are important considerations for investors, as these features provide consistency to operations and income.

On the financial side, Gladstone brought in $35.9 million in total operating revenue for 4Q23, down 1.5% from the previous year and missing the consensus expectation of $36.8 million. This revenue total supported a core FFO – funds from operations – for the quarter of 36 cents per share. This was 1 cent better than had been expected and was up 2 cents quarter-over-quarter.

The company’s FFO was more than enough to support the total dividends paid in Q4, which came to 30 cents per common share. The dividend is paid out monthly, like AGNC above; the monthly payout is 10 cents per common share, and the company has recently declared its dividends for April, May, and June. The annualized payment, at $1.20 per share, gives a solid yield of 9.12%.

This stock has caught the eye of Alliance Global Partners analyst Gaurav Mehta, who is upbeat based on the company’s portfolio – specifically, the portfolio’s stable performance and amenability to expansion. Mehta writes, “GOOD is an externally managed REIT that primarily owns industrial and office real estate. Our Buy rating is based on a growing exposure to industrial real estate, stable operating performance with mark to market rent upside for industrial portfolio, opportunity to grow and improve portfolio through asset recycling, and availability of multiple sources of capital to fund growth… Going forward, we expect the common dividend to remain steady.”

That Buy rating is accompanied by a $15.50 price target that suggests a one-year upside potential of 18%. That upside, and the forward dividend yield, imply a total one-year return of 27%. (To watch Mehta’s track record, click here)

There are only 2 recent analyst reviews on file for Gladstone, but they both agree that this is a stock to buy, making the consensus view a Moderate Buy. The shares have a trading price of $13.15 and an average target price of $14.75, indicating potential for a 12% upside on the one-year timeframe. (See Gladstone stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.