Now that we’ve had time to digest the April jobs numbers, some strategists are getting worried about the economy’s mid-term outlook. The jobs report showed 175,000 new jobs added in the month – but that was the lowest gain in the past six months, and was accompanied by an uptick in unemployment, from 3.8% to 3.9%. Along with these topline numbers, the report showed declines in job openings and hires.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

For Roukaya Ibrahim, watching the US economy from BCA, this job report may indicate a shift toward a recession by the end of this year or early in 2025.

“I think that there’s still a runway for the soft landing narrative to continue over the coming months. But eventually, the unemployment rate is going to take higher and that’s going to lead to concerns about a recession,” Ibrahim noted.

The strategist goes on to predict that, in the event of a recession, the S&P 500 could drop to 3,600, or a 31% decline from current levels.

That may be a gloomy outlook, and it suggests a defensive stance for investors – which will naturally turn our attention to dividend stocks. These shares are known for providing real protection to an investment portfolio during a downturn, through a reliable income stream via dividend payments.

Against this backdrop, some Wall Street analysts have given the thumbs-up to two dividend stocks yielding more than 12%. Opening up the TipRanks database, we examined the details behind these two to find out what else makes them compelling buys.

Kimbell Royalty Partners (KRP)

For the first stock on our list, we’ll head to Fort Worth, Texas, where Kimbell Royalty Partners has its headquarters. This company has chosen the right place to set up shop – Texas, in recent decades, has become a major player in the world energy industry, and Kimbell is in the mineral rights business. The company buys land titles and associated mineral rights in rich hydrocarbon basins across the US, and earns royalties on the oil and gas production that takes place on its holdings. The company currently holds approximately 17 million gross acres in 28 states, with its largest single footprint in the famous Permian Basin in the Texas-New Mexico boundary region.

Kimbell’s holdings host active oil and gas extraction activities. As of March 31 this year, the end of Q1, Kimbell’s major properties had 8.2 DUCs, or drilled but uncompleted wells. The company’s total acreage had 98 active rigs, which represented more than a 16% market share of all active land rigs in the lower 48 states.

Royalties on oil, natural gas, and natural gas liquid production from Kimbell’s acreage form the base of the company’s revenue stream, and Kimbell realized a top line of $82.2 million in 1Q24. This figure was up 22% year-over-year and beat the forecast by $1.1 million. The revenue was based on a record quarterly run-rate daily production of 24,678 Boe, or barrels of oil equivalent, per day.

Of particular interest to dividend investors, Kimbell finished Q1 with $48.9 million in cash available for distribution, up 59% year-over-year. The company declared its Q1 dividend at 49 cents per common share, for payment on May 20. This dividend represents a payout of 75% of the cash available for distribution. Its annualized rate of $1.96 per common share gives a forward yield of 12.2%, a high return by any measure and far above the current 3.5% rate of inflation.

For Truist analyst Neal Dingmann, an analyst ranked in the top 1% of Street stock pros and an expert on the energy sector, several key factors inform the bull case. “We forecast Kimbell to continue to generate production and FCF growth with numerous line-of-site wells ensuring ample upside,” said the 5-star analyst. “The solid production profile along with what appears to be continued strong prices resulted in the company boosting its distribution by 14% during the most recent period. We anticipate the company continuing to add strategic assets such as the private deal late last year given KRP’s relationships/skillset and the continued fragmented minerals market.”

These comments support Dingmann’s Buy rating on the shares, while his $21 price target implies a one-year upside potential of 31%. Add the forward dividend yield, and that’s a possible return of 43%. (To watch Dingmann’s track record, click here)

That bullish outlook is no outlier, as Kimbell’s Strong Buy consensus rating is unanimous, based on 5 positive analyst reviews in recent weeks. The stock is selling for $16.01, and its $20.75 average price target suggests that the shares will gain 29.5% over the coming year. (See KRP stock forecast)

TXO Energy Partners (TXO)

The second stock on our list is TXO Energy Partners, a limited master partnership firm operating in the Southwest. The company owns productive hydrocarbon acreage positions in two of the region’s best energy basins – the Permian, of Southwest Texas and New Mexico, and the San Juan, straddling the New Mexico-Colorado state line. These basins are known for their profitable oil and gas plays, and TXO’s land holdings in both bring solid benefits to the company and its shareholders.

TXO’s management takes great care in its land acquisitions, focusing on building a profile based on predictable production. The company achieves this by basing its properties on proven oil and gas production, choosing locations that have decades-long production histories. This gives TXO a set of holdings with clearly understood geology and reservoir characteristics, reducing the risk when compared to unconventional resource plays. TXO’s assets have long-lived reserves and low production decline rates, along with high hydrocarbon recovery rates relative to the costs of completing drilling activities.

Getting down to brass tacks, this means that TXO has solid prospects for generating revenues and dividends from its property holdings. That said, in its last SEC filing, the company reported a 1Q24 top line of $67.44 million, a figure that fell by 57.4% compared to the year-ago period, although it beat the estimates by $2.2 million. The company followed this up with a distribution declaration – that is, a dividend – of 65 cents per common share. This represented a 7-cent increase from the previous quarter. The newly raised dividend annualizes to $2.60 per common share and gives a forward yield of 12.6%.

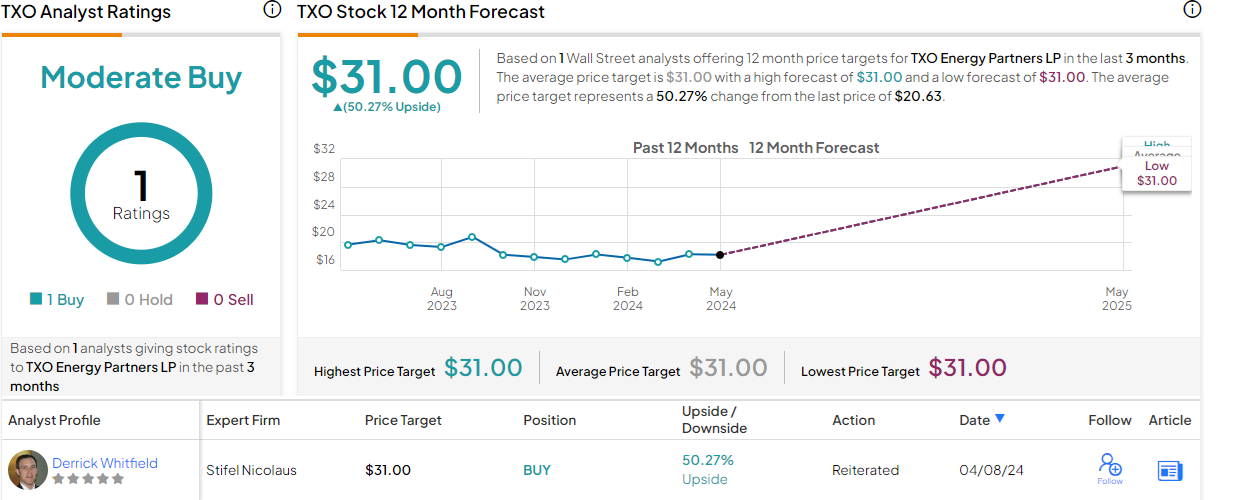

This stock has caught the eye of Stifel analyst Derrick Whitfield, who remains bullish on the shares, writing, “In short, we believe TXO offers investors a highly experienced management team, exposure to low decline, low cost production, a shareholder-friendly distribution framework, and an attractive valuation relative to peers. Based on our estimates, TXO can return 100% of its enterprise value by 2030, offering significant value now and potential upside in the future. Net-net, TXO offers advantaged dividend yield and operational control relative to its Minerals peers, in our view.” (To watch Whitfield’s track record, click here)

The Stifel take is the only analyst review currently on file for TXO and includes a Buy rating with a $31 price target that points toward a 50% gain on the one-year horizon. With the dividend yield, the total return can reach nearly 63%. (See TXO stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.