The headwinds are piling up on our economic horizon, just a few blurs of cloud right now, at the edge of the horizon – and we just don’t know what’s coming next. The headwinds include factors we all know about: persistent inflation, the Fed’s higher interest rates and tighter monetary policy, the tighter business and consumer credit environment, and the fast-rising government debt which at $33.57 trillion already measures 103% of the total GDP. We’ve been reading about these headwinds for several years now; what we don’t know is if, or when, they will coalesce into a storm.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

In the words of Jamie Dimon, the CEO of JPMorgan, “This may be the most dangerous time the world has seen in decades. While we hope for the best, we prepare the Firm for a broad range of outcomes so we can consistently deliver for clients no matter the environment.”

The bottom line is that investors need to take defensive postures with their portfolio additions. And that will naturally lead investors toward high-yield dividend stocks. These income-generating equities offer some degree of protection against both inflation and share depreciation by providing a steady income stream.

Against this backdrop, some top-rated analysts have given the thumbs-up to two dividend stocks yielding up to 11%. Opening up the TipRanks database, we examined the details behind these two to find out what else makes them compelling buys.

Blackstone Secured Lending (BXSL)

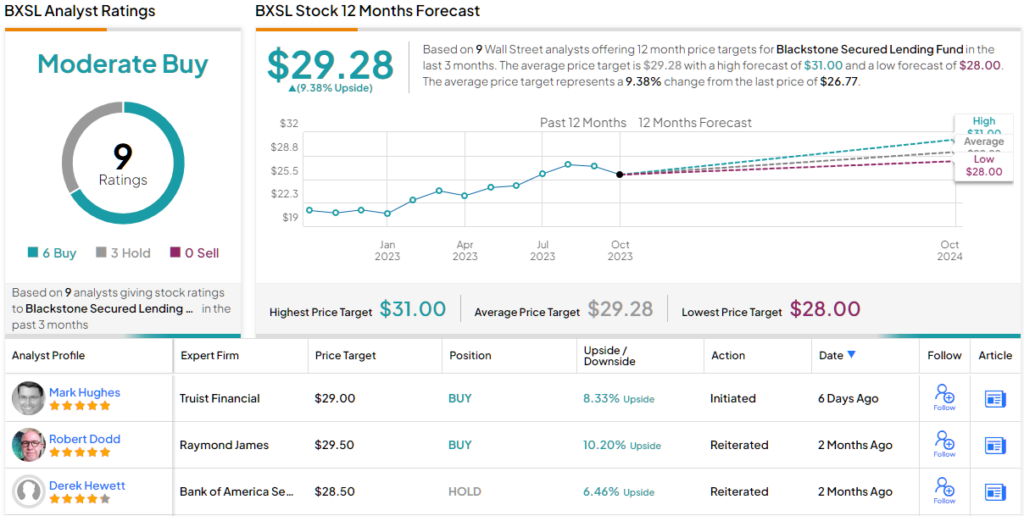

First up is Blackstone Secured Lending, a business development company, or BDC, operating under the larger cover of the Blackstone asset management firm. BXSL operates in the financial services sector, providing capital and credit services to private companies in the US market and across a wide range of sectors including veterinary care, the insurance industry, and cable communications distributors. The top sectors represented in BXSL’s portfolio are software and healthcare.

By the numbers, BXSL’s portfolio holds $9.3 billion in investments, at fair value. These are composed mainly of first lien senior secured loans, 98.4% of the total, and 98.7% of the total is made in floating rate instruments. BXSL has current investments in 180 companies, as of the end of 2Q23.

That was the last reported quarter, and in it, BXSL realized some $290 million in total investment income. This was up 55% year-over-year and beat the forecast by $14.5 million. At the bottom line, BXSL reported a net investment income of $1.06 per share, a result that was 3 cents per share ahead of the estimates. The NII exceeded the company’s regular dividend payment – marking the 17th quarter in a row that BXSL has achieved full coverage of the common share dividend.

BXSL has recently increased its common share regular dividend by 10% to 77 cents, which is scheduled to be paid out this coming October 26. At an annualized rate of $3.08, this dividend offers a robust yield of 11.5%, surpassing the average dividend yield of S&P-listed companies by more than 5x.

Truist analyst Mark Hughes has been impressed by BXSL’s high quality portfolio and its ability to maintain its dividend. The 5-star analyst writes of the stock, “The high quality of Blackstone Secured Lending’s portfolio is underscored by its low proportion of PIK income and high dividend coverage. This positions the company to both grow net asset value (NAV) on a consistent basis and to maintain a stable and attractive dividend yield; historically this has been the formula for BDCs to trade at a premium to NAV… Blackstone Secured Lending shares are compelling on a price-to-NAV basis, we believe, particularly when evaluated in the context of the company’s return on equity and the quality of its investment portfolio…”

Looking ahead, Hughes rates BXSL shares a Buy, and his price target, now set at $29, implies the stock will gain 8.3% in the year ahead. The total return will approach ~20% when the dividend is added to the upside. (To watch Hughes’ track record, click here)

Overall, the 9 recent analyst reviews on this stock include 6 Buys over 3 Holds, for a Moderate Buy consensus rating. (See BXSL stock forecast)

Equitrans Midstream (ETRN)

Next up on our ‘dividend list’ is Equitrans, a midstream company in the oil and gas sector. Midstream firms hold a vital link in the energy chain, moving hydrocarbon products from production regions and wellheads to the refineries, terminal points, and storage farms where retailers can pick it up for sale to the end users. Equitrans focuses its operations in the Appalachian region, specifically the area where Pennsylvania, Ohio, and West Virginia come together. This is one of America’s richest natural gas production regions and forms the core of this company’s extensive midstream network.

Equitrans’ transport assets mainly move natural gas and natural gas products out of the Appalachian Basin; the company describes its network as holding a strategic position capable of ‘debottlenecking’ the Basin. In particular, the company’s Mountain Valley Pipeline (MVP) and MVP Southgate projects promise the growth needed to improve the key link between natural gas sources and the major US demand markets.

At bottom, this means the company is routinely capable of generating profits and cash. Yet, in its last financial report, for Q2, the company’s total revenue came to $318.5 million, down 3% from the prior-year quarter and missing the forecast by almost $7.9 million. But – the company’s bottom line was sound, at 9 cents per share by non-GAAP measures, a result that beat the forecast by 4 cents per share.

This company has a dividend history going back to 2019, and the dividend has been held stable since 2020. That current stable payment is 15 cents per common share, or 60 cents annually, and the dividend yield is 6.3%.

Writing on this stock from Goldman Sachs, industry expert John Mackay likes Equitrans’ extensive footprint and notes that its assets are attractive to investors and M&A firms alike.

“Given ETRN’s strategic gathering and transmission footprint in the Appalachian Basin, relative EV size, and cash flow clarity from an MVP resolution, we see ETRN as a potential M&A target. ETRN’s assets are highly strategic in our view in the core of the SW Marcellus and Utica with interconnections into all major interstate pipelines in the region – and are supported by long term MVCs with IG counterparties… With an EV size of ~$[12]b, we believe the relative size appears manageable for larger midstream players,” Mackay opined.

Going forward, these comments back up the Goldman Sachs analyst’s Buy rating, which comes with an $11.50 price target, suggesting a gain of almost 21% on the one-year horizon. That return can reach 27% with the dividend added in. (To watch Mackay’s track record, click here)

Overall, Equitrans boasts a Strong Buy rating from the analyst consensus, and it is unanimous – based on 3 recent positive share reviews. (See Equitrans stock forecast)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.