The market is being buffeted by conflicting headwinds, making the pundits’ job harder. While inflation appears to be moderating, with the annualized rate down to 5% in March – the lowest since the summer of 2021 – the job market remains surprisingly robust. Last month, the BLS reported 253,000 new jobs, exceeding the predicted 180K, and an unemployment rate of just 3.4% compared to a forecast of 3.6%.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

The robust job numbers present a challenge for the Federal Reserve, which is tasked with managing inflation. In an effort to curb inflation, the central bank has raised interest rates, which are currently hovering between 5% and 5.25%. Although the latest interest rate hike, implemented earlier this month, was anticipated to be the last one for the near future, there are concerns that the Fed may prioritize tightening the job market to combat inflation, even if it means taking the risk of triggering a recession or another banking crisis.

For stock investors, the situation presents a natural move: a shift into defensive equities. The classic defensive play is dividend stocks, especially the high-yield dividend stocks. With their reliable passive income streams, and inflation-beating yields, these stocks present investors with resources to weather a storm.

Wall Street’s top analysts would agree – they have been picking out top dividend stocks for investors to buy, and focusing on div shares that will give yields of at least 9% going forward. Let’s take a closer look.

Kimbell Royalty Partners (KRP)

We’ll start with Kimbell Royalty Partners, a mineral rights company based in Texas with land holdings in multiple ‘areas of interest’ across North America. Kimbell’s holdings include more than 16 million gross acres, in all of the major onshore hydrocarbon production basins of the continental US, including the Permian and Eagle Ford of Texas, the Bakken of North Dakota-Montana, and the Haynesville of Louisiana.

The company derives its income from production royalties on hydrocarbon extraction from its acreage, and it also owns royalty interests in more than 124,000 gross wells on its lands. That total includes more than 48,000 wells just in the Permian Basin, the famous Texas formation that, in recent decades, has made the Lone Star State a player in the world oil industry.

Kimbell takes care to keep its mineral rights holdings up to date, through regular acquisition activity. The most recent such move, announced in April of this year, was for a $143.1 million mineral and royalty purchase in the Midland Basin in Texas. The purchase includes mineral and royalty rights on 60,000 gross acres of the Northern Midland Basin, and is expected to add $43.3 million in cash flow over the next 12 months.

The company’s properties already produced a strong profit, even before that acquisition. In the recently released financial results for 1Q23, Kimbell announced total revenues of $66.9 million, nearly double the $33.7 million from the year-ago quarter. This supported a GAAP EPS of 36 cents, beating the forecast by 19 cents.

Along with the quarterly results, Kimbell also announced its Q1 dividend distribution, set at 35 cents per common share. This was fully covered by the GAAP EPS, and represented 75% of the cash available for distribution. The 35 cent dividend annualizes to $1.40 per share and gives a yield of 9%.

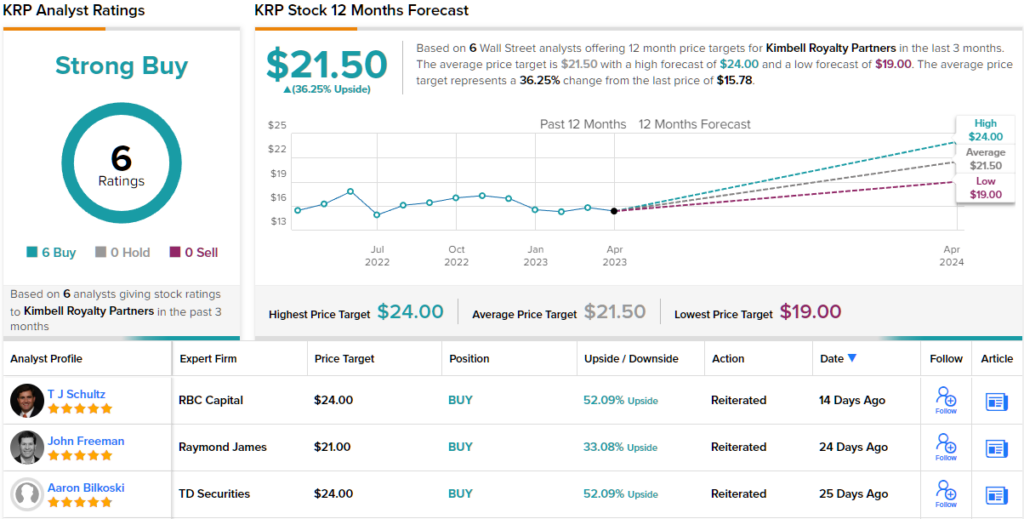

Covering this stock for RBC Capital, 5-star analyst TJ Schultz takes an upbeat view, based in part on Kimbell’s ability to drive growth through acquisition – and its potential for increasing the dividend yield.

“The solid EBITDA print (on better than expected realized natural gas prices) should be supportive near term. KRP has executed on Permian growth transactions recently, which helps to better balance its oil/gas mix as the production base grows (~54% natural gas post deals). At the current RBC price deck, we think KRP offers the potential for >10% forward yield (on a 75% payout ratio), and we view the relative valuation discount vs closest royalty peers as constructive,” Schultz wrote.

Looking ahead, Schultz rates KRP stock an Outperform (i.e. Buy), and his $24 price target implies a one-year gain of 52% for the stock. Based on the current dividend yield and the expected price appreciation, the stock has 61% potential total return profile. (To watch Schultz’s track record, click here)

Overall, KRP gets a Strong Buy rating from the analyst consensus, based on 6 unanimously positive recent reviews. The average price target is $21.50, suggesting a 36% share appreciation from the current trading price of $15.78, heading out to the one-year time frame. (See KRP stock forecast)

Camping World Holdings (CWH)

The next dividend stock on our list is Camping World Holdings, a company that has long held a successful position in the outdoor leisure and recreation niche. The company is primarily a dealer in recreational vehicles, offering multiple lines of towed and self-powered RVs, both new and used, along with the ancillary gear that RVers need. Apart from campers, CWH is also involved in water and marine leisure, and sells boats and other watercraft, as well as tow trailers and other equipment.

CWH operates through its subsidiaries, and is currently the largest retailer of RVs and related outdoor and camping products working in the US market. The company’s Camping World and Good Sam brands have been in business since 1966, and the company has taken care to get to know its customers and what they want.

Knowing the customer is a boon for any business, and CWH has used its knowledge to beat the revenue and earnings forecasts for the first quarter of this year. While both the top and bottom lines were down year-over-year, both came in ahead of expectations. The top line number, $1.49 billion in total revenue, was $10 million more than the Street had been looking for, while the bottom line non-GAAP diluted EPS of 14 cents profit was 17 cents better than the expected 3-cent loss.

The company attributed its sound results to record sales in used vehicles, which rose 10.4% y/y to reach $444.7 million in the quarter. Used vehicle unit sales grew 13.3% and hit 12,432 units, also a company record. The increase in used vehicle sales reflects constraints on customers in a tightening economic environment, but also continued strong demand.

In a move that shows the company’s confidence, CWH announced earlier this month that it intends to open its first location in Montana, through the acquisition of Billing-based I-90 RV. The move will increase CWH’s presence in the northern Plains; details of the intended transaction have not yet been released. The move follows six similar announcements in recent months, announcing acquisition in the states of Arkansas, California, Michigan, Oregon, and Utah.

Turning to the dividend, we find that CWH last paid out its distribution on March, for 1Q23. The common share dividend, at 62.5 cents, annualizes to $2.50 and gives a high yield of 10%. That’s double the last annualized inflation numbers.

All of this caught the eye of Baird analyst Craig Kennison, who is impressed by CWH’s ability to shift with the market trends and needs.

“CWH reported upside to EBITDA expectations fueled by growth in the used RV market. We like the pivot to the used market, which offers more affordable options for consumers and a larger addressable market for Camping World – all while leveraging unique sourcing tools CWH has developed. Separately, management signaled an aggressive dealer consolidation phase, building on several deals already in 2023. Investor sentiment has yet to turn positive on dealers, but we see value for patient investors to the extent CWH continues to pay the dividend (10%),” Kennison opined.

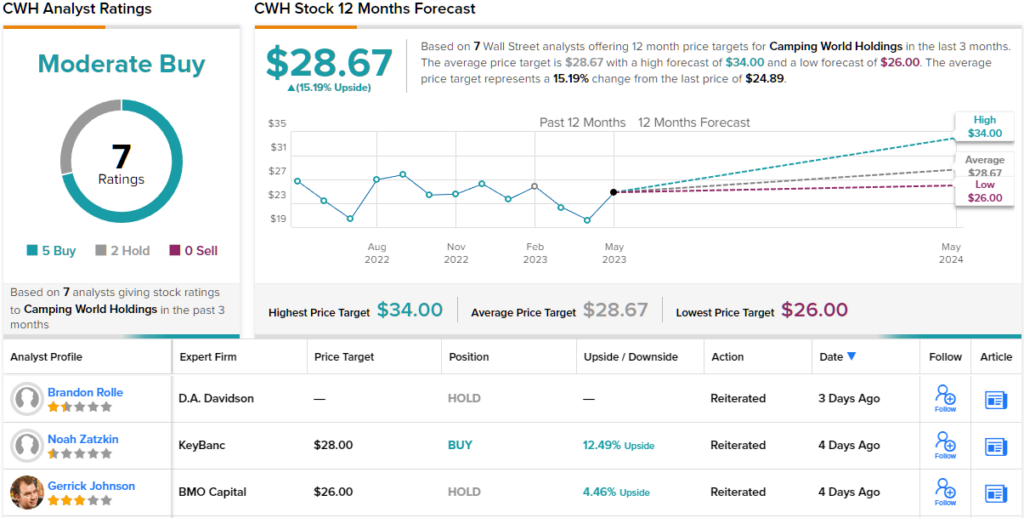

To this end, the 5-star analyst gives CWH stock an Outperform (i.e. Buy) rating, along with a $28 price target that implies an upside of 12.5% for the coming year. (To watch Kennison’s track record, click here)

Overall, the shares have a Moderate Buy consensus rating, based on 7 analyst reviews that include 5 Buys and 2 Holds. The average price target of $28.67 suggests a one-year gain of 15% from the current share price of $24.84. (See CWH stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.